Reports

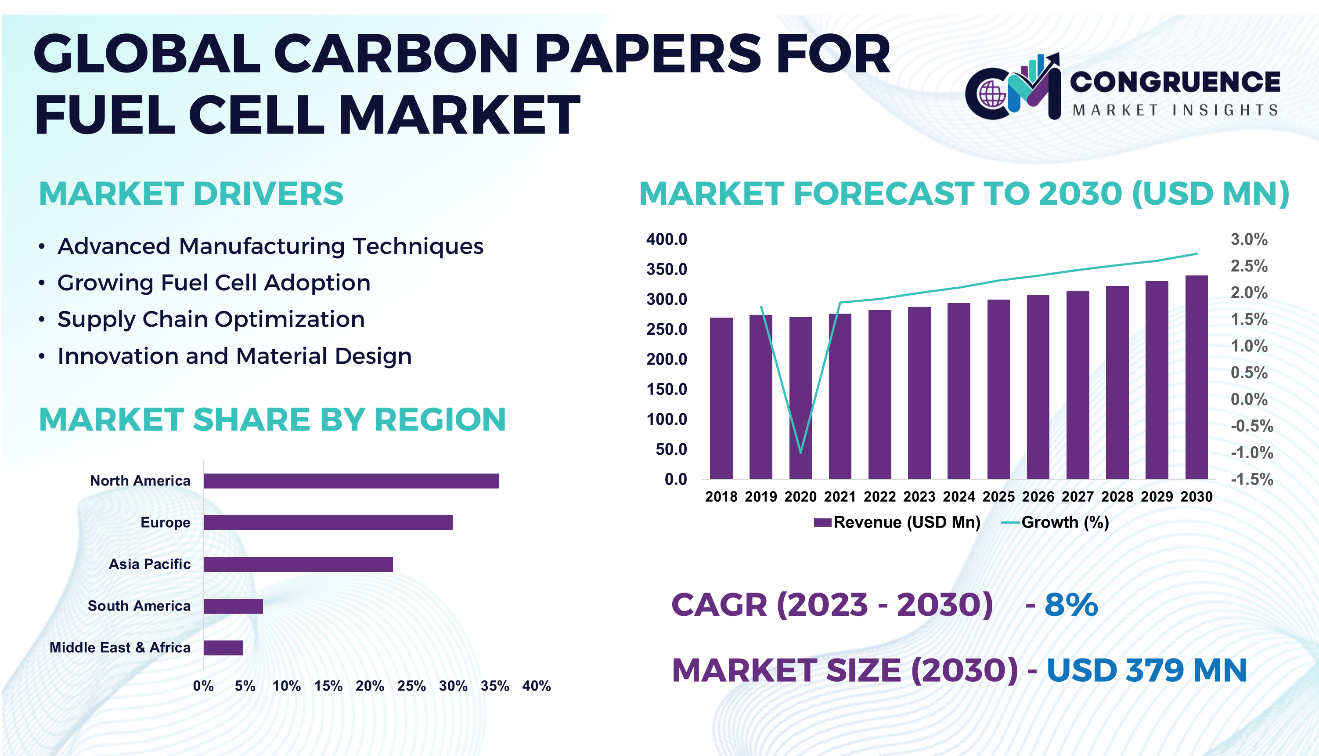

The Global Carbon Papers for Fuel Cell Market was valued at USD 207.70 Million in 2022 and is anticipated to reach a value of USD 379.39 Million by 2030 expanding at a CAGR of 8% between 2023 and 2030.

Fuel cells are becoming more and more popular, which is driving up demand for carbon sheets, which are essential to fuel cell technology. The growing need for clean and sustainable energy sources is propelling the continuous rise of the global market for carbon sheets used in fuel cells. Fuel cells rely on carbon sheets as vital parts to effectively convert chemical energy into electrical energy via electrochemical reactions. The market is being driven by factors such as the increasing focus on environmental sustainability, stricter laws aimed at reducing carbon emissions, and the growing use of fuel cell technology in a variety of applications, such as portable devices, stationary power generation, and automobiles. The need for fuel cells and associated parts like carbon papers is predicted to increase as nations work to switch to low-carbon energy sources. Furthermore, carbon papers' performance and durability are being improved by continuous developments in material science and production techniques, which makes them more appropriate for demanding fuel cell applications. Furthermore, research institutes, businesses, and governments are working together to foster innovation in fuel cell technology, which is propelling the market's expansion. But obstacles like fuel cell technology's high production costs and restricted scalability still need to be addressed before it can be widely used. Notwithstanding these obstacles, the market for carbon sheets for fuel cells is expected to grow in the next years due to the growing emphasis on renewable energy sources and the desire for a more sustainable future.

Carbon Papers for Fuel Cell Market Major Driving Forces

Advanced Manufacturing Techniques: By using advanced manufacturing techniques like additive manufacturing and nanotechnology, carbon papers with improved properties and precise microstructure control can be produced, which improves fuel cell performance.

Growing Adoption of Fuel Cells: The need for carbon papers as essential components of fuel cell stacks is being driven by the growing use of fuel cells in a variety of applications, including stationary power production and mobility.

Supply Chain Optimization: To ensure continuous manufacturing of carbon sheets for fuel cells, producers must source raw materials and manage the supply chain effectively. This has led them to form strategic alliances and broaden their sourcing possibilities.

Innovation and Material Design: By improving the functionality and efficiency of carbon sheets for fuel cells, material design innovation propels market expansion. The creation of strong, lightweight, and highly conductive carbon sheets is made possible by developments in materials science, which satisfy changing market needs for greener and more sustainable energy sources.

Carbon Papers for Fuel Cell Market Key Opportunities

Technological Developments: As material science, nanotechnology, and manufacturing techniques continue to progress, there is potential to improve the efficiency and performance of carbon sheets for fuel cells. This will provide manufacturers a competitive advantage and allow them to create innovative solutions.

Application Diversification: Fuel cell applications have expanded beyond the conventional uses in transportation and stationary power generation to include the aerospace, marine, and portable electronics industries. This has given carbon paper producers new ways to meet the changing demands of the market.

Energy Transition Initiatives: Governments and organizations throughout the world are placing a greater emphasis on decarbonization and renewable energy transition programs, which is driving demand for clean energy solutions like fuel cells and fostering a climate that is favorable for carbon paper makers to profit from.

Carbon Papers for Fuel Cell Market Key Trends

· Increasing focus on reducing carbon emissions drives demand for clean energy solutions like fuel cells, boosting the market for carbon papers.

· Ongoing developments in material science and manufacturing techniques enhance the performance and efficiency of carbon papers for fuel cells.

· Fuel cell applications expand beyond traditional sectors into aerospace, marine, and portable electronics, broadening opportunities for carbon paper manufacturers.

· Growing emphasis on eco-friendly materials and practices propels demand for sustainable carbon papers in fuel cell applications.

Region-wise Market Insights

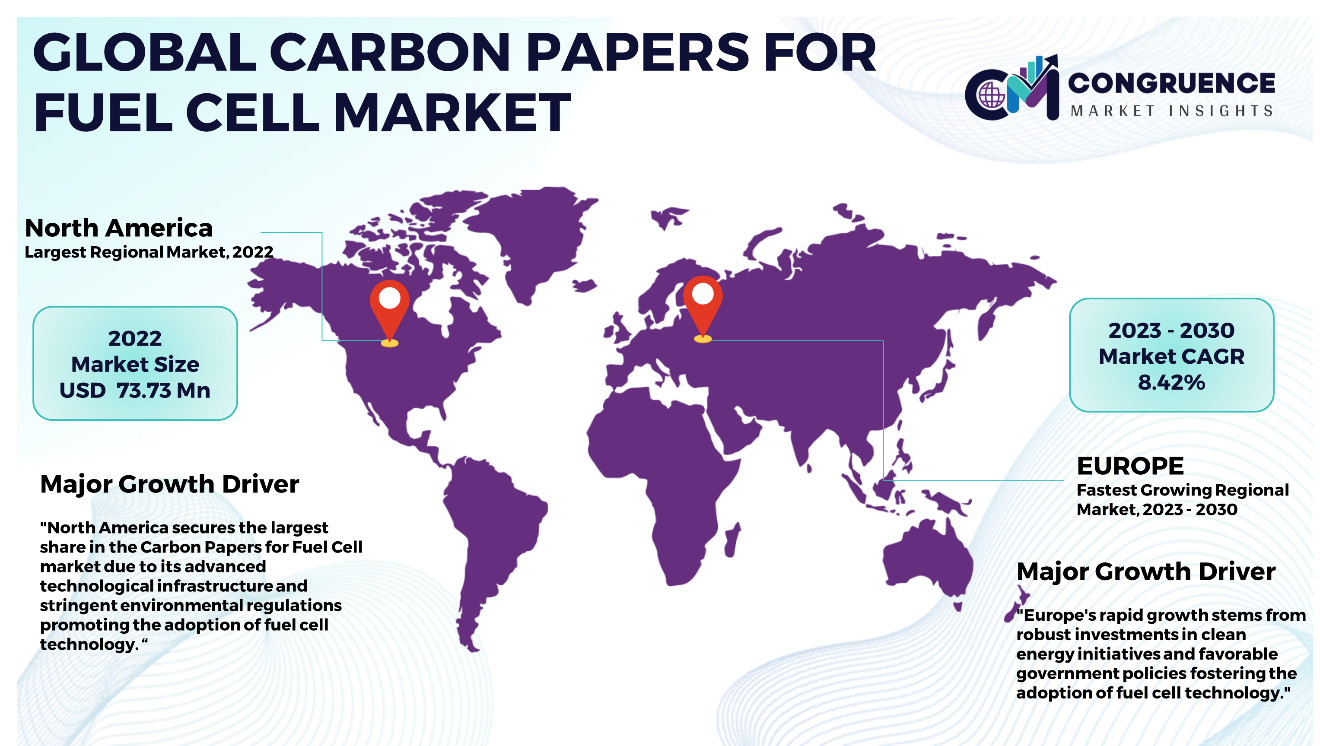

North America accounted for the largest market share at 35.5% in 2022 whereas, Europe is expected to register the fastest growth, expanding at a CAGR of 8.4% between 2023 and 2030.

Fuel cell technology is widely adopted in North America due to a strong legislative framework and advanced technological infrastructure, which has generated a sizable market for carbon sheets. The carbon sheets market for fuel cells is expanding in North America due to a number of factors, such as robust investment in research and development, government incentives for the adoption of renewable energy, and a well-established automotive sector. Growth in the market is encouraged by the region's emphasis on lowering carbon emissions and advancing fuel cell technology, particularly in transportation applications. In addition, collaborations between industry and academia spur innovation and improve the performance and economic feasibility of carbon sheets for fuel cells. In the meantime, strong government incentives and an increasing emphasis on sustainability are driving Europe's rapid growth. Demand is rising throughout the Asia-Pacific area as a result of fast urbanization and industrialization. The Middle East and Latin America exhibit young but promising growth trajectories, propelled by rising investments in clean energy projects. Africa's poor infrastructure presents problems, but it also presents chances for market growth as people become more aware of the advantages of renewable energy. The adoption and growth of fuel cell technology are influenced by the distinct economic, environmental, and regulatory landscapes of each location, which in turn shapes the need for carbon papers. For carbon paper makers to properly customize their strategies and take advantage of the different opportunities available across global marketplaces, they must have a thorough understanding of regional variations.

Market Competition Landscape

Fuel cell manufacturers are competing fiercely for clients in the highly competitive carbon sheet market by offering distinctive solutions. Competitive dynamics are influenced by a number of key factors, including technical innovation, customer service, pricing strategy, and product quality. It is also evident that key factors influencing market positioning include environmental sustainability, regulatory compliance, and reliability history. Fuel cell technology is becoming more and more in demand across a wide range of industries, which is driving up competition and requiring firms to invest heavily in R&D to stay ahead of the curve. To improve their market positions and increase the size of their consumer bases, industry players regularly use mergers, acquisitions, and strategic alliances. Overall, the competitive environment highlights the need it is to always develop and deliberately differentiate yourself in order to prosper in the evolving market for carbon sheets used in fuel cell applications.

Key players in the global Carbon Papers for Fuel Cell market implement various organic and inorganic strategies to strengthen and improve their market positioning. Prominent players in the market include:

· SGL Carbon

· Toray Industries, Inc.

· AvCarb Material Solutions

· Bloom Energy

· Mitsubishi Chemical Corporation

· Duralyst Energy Private Limited

· Cellkraft

· Nuvera Fuel Cells, LLC

· CeTech

· KBC (Yokogawa)

· Ceres

|

Report Attribute/Metric |

Details |

|

Market Revenue in 2022 |

USD 207.70 Million |

|

Market Revenue in 2030 |

USD 379.39 Million |

|

CAGR (2023 – 2030) |

8% |

|

Base Year |

2022 |

|

Forecast Period |

2023 – 2030 |

|

Historical Data |

2018 to 2022 |

|

Forecast Unit |

Value (US$ Mn) |

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Segments Covered |

· By Type (PEMFCs (Proton Exchange Membrane Fuel Cells), SOFCs (Solid Oxide Fuel Cells), MCFCs (Molten Carbonate Fuel Cells), and PAFCs (Phosphoric Acid Fuel Cells)) · By Application (Gas Transportation, Water Management, Power Generation, and Others) · By End Use Industry (Transportation, Power and Utilities, Military and Defense, Telecommunications, and Others) |

|

Geographies Covered |

North America: U.S., Canada and Mexico Europe: Germany, France, U.K., Italy, Spain, and Rest of Europe Asia Pacific: China, India, Japan, South Korea, Southeast Asia, and Rest of Asia Pacific South America: Brazil, Argentina, and Rest of Latin America Middle East & Africa: GCC Countries, South Africa, and Rest of Middle East & Africa |

|

Key Players Analyzed |

SGL Carbon, Toray Industries, Inc., AvCarb Material Solutions, Bloom Energy, Mitsubishi Chemical Corporation, Duralyst Energy Private Limited, Cellkraft, Nuvera Fuel Cells, LLC, CeTech, KBC (Yokogawa), and Ceres |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |