Reports

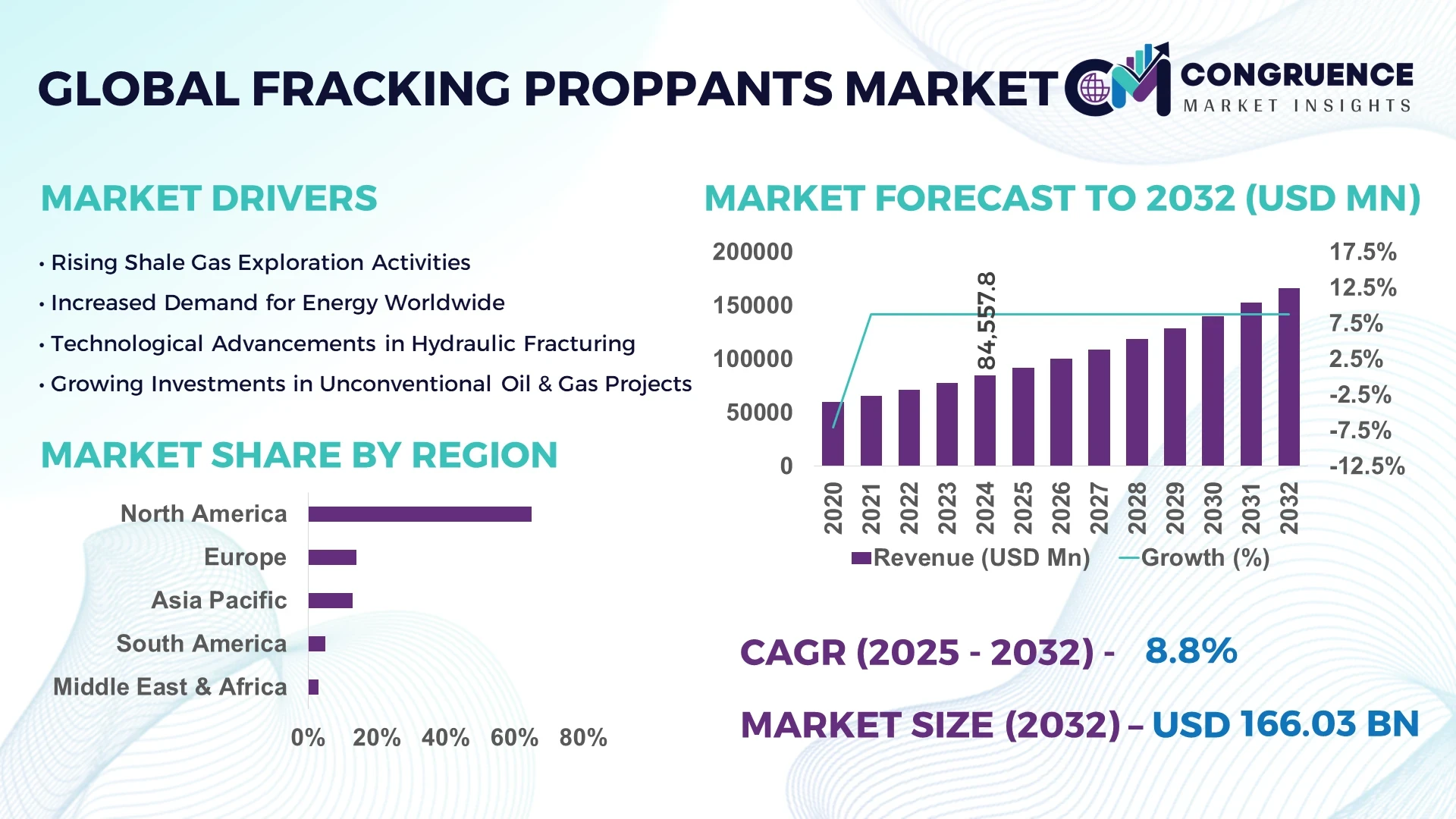

The Global Fracking Proppants Market was valued at USD 84,557.8 Million in 2024 and is anticipated to reach a value of USD 113,954.77 Million by 2032 expanding at a CAGR of 8.8% between 2025 and 2032.

The Fracking Proppants market is gaining global traction due to the rising need for efficient hydrocarbon extraction, especially in unconventional resources such as shale gas and tight oil. Fracking Proppants are extensively used to maintain fractures in hydraulic fracturing operations, thereby enhancing oil and gas production. The North American region, especially the United States, dominates the Fracking Proppants market due to large-scale shale exploration. Asia-Pacific is witnessing robust growth in demand for Fracking Proppants due to increased investments in unconventional energy exploration. Fracking Proppants such as frac sand, resin-coated proppants, and ceramic proppants play a pivotal role in sustaining fracture openings. Increasing demand from developing economies for energy security further accelerates the demand for Fracking Proppants globally. The market is expected to see increasing technological advancements in proppant materials to improve performance and cost-efficiency. The global Fracking Proppants market is being shaped by exploration dynamics, well development rates, and global energy consumption trends.

Artificial Intelligence is revolutionizing the Fracking Proppants market through intelligent automation, predictive analytics, and real-time monitoring in fracturing operations. In hydraulic fracturing, AI is used to analyze vast datasets generated during exploration and production to optimize the selection and deployment of Fracking Proppants. AI-based platforms are capable of predicting fracture propagation and proppant transport behavior with higher accuracy than traditional methods. For example, Halliburton's Voice of the Oilfield AI model has reduced proppant waste by 15% in U.S. shale basins. AI also assists in real-time monitoring of proppant flow, pressure changes, and fracture conductivity, which reduces non-productive time and improves operational efficiency.

In the Fracking Proppants market, machine learning algorithms are deployed to optimize well spacing and proppant intensity. This has enabled operators to achieve up to 20% more hydrocarbon recovery per well in the Permian Basin. AI also contributes to sustainability by minimizing environmental impact through better design of proppant schedules and volumes. AI is being leveraged by companies like Schlumberger and Baker Hughes to reduce silica dust exposure by forecasting and automating sand logistics. The integration of AI in the Fracking Proppants market is expected to increase as producers seek to improve recovery rates, reduce costs, and minimize environmental risks in hydraulic fracturing operations.

"In 2024, Halliburton launched a machine learning platform that uses AI to predict the optimal proppant concentration per stage in unconventional wells. This development enhances decision-making and reduces material waste, leading to improved operational output and better resource allocation across the fracking proppants market."

The Fracking Proppants market dynamics are influenced by evolving energy demands, environmental regulations, and technological advancements. Market forces such as increasing unconventional resource development, global oil prices, and proppant performance innovation significantly impact the supply and demand for Fracking Proppants. The rise in hydraulic fracturing projects globally is boosting the need for high-strength proppants like resin-coated and ceramic proppants. Simultaneously, the cost sensitivity of operators sustains high demand for cost-effective natural frac sand. The Fracking Proppants market is witnessing innovation in proppant materials to improve conductivity, reduce fines generation, and enhance well productivity. Key dynamic elements include environmental policy shifts, investment in green energy, and regional exploration patterns.

Surge in Unconventional Oil and Gas Exploration Activities

The Fracking Proppants market is driven by the growing development of shale gas and tight oil formations, especially in the U.S., China, and Argentina. The United States alone drilled over 14,000 horizontal wells in 2023, 90% of which used hydraulic fracturing techniques requiring Fracking Proppants. China's Ministry of Natural Resources reported a 25% increase in shale gas output in 2023, fueling domestic proppant demand. Fracking Proppants are essential in these unconventional reserves to keep fractures open and maximize hydrocarbon flow. The increase in global energy demand has led to accelerated upstream investments, pushing the growth of the Fracking Proppants market.

Environmental Regulations and Health Concerns

The Fracking Proppants market faces restraints due to stringent environmental and occupational safety regulations. Frac sand mining has raised concerns over air pollution, water usage, and land degradation. The U.S. Occupational Safety and Health Administration (OSHA) has enforced strict limits on crystalline silica exposure, impacting frac sand handling and logistics. Additionally, community resistance to sand mining operations has led to permit delays in Wisconsin and Texas, which account for over 70% of U.S. frac sand production. These environmental and health restrictions increase operating costs and limit expansion, thereby posing a restraint on the growth of the Fracking Proppants market.

Technological Innovation in Proppant Design and Coatings

The Fracking Proppants market holds significant opportunities in the development of advanced proppants with higher thermal stability, conductivity, and strength. Innovations such as ultra-lightweight ceramic proppants, nano-coated resin proppants, and degradable proppants are gaining traction. According to industry data, engineered proppants improve hydrocarbon flow by up to 30% compared to traditional frac sand. Companies investing in customized proppant solutions for specific geologies can tap into high-margin segments of the market. Additionally, biodegradable and environmentally safe proppants are opening new avenues in regions with tight regulatory frameworks, such as the European Union and parts of North America, thus expanding market opportunities.

Volatile Oil Prices Impacting Fracturing Activity

One of the primary challenges in the Fracking Proppants market is the volatility in global oil prices. The fluctuating prices directly affect drilling activity and proppant consumption. For instance, the oil price dip during Q1 2023 led to a 10% reduction in U.S. rig counts, impacting frac sand demand. Uncertainty in oil and gas investments also delays new well development, causing an inconsistent demand cycle for Fracking Proppants. The high capital intensity of proppant production facilities makes them vulnerable to market fluctuations. Furthermore, increased competition among proppant suppliers can compress margins and impact long-term sustainability in the Fracking Proppants market.

The Fracking Proppants market is witnessing several key trends that are reshaping the industry landscape. One major trend is the shift towards in-basin frac sand supply to reduce transportation costs and ensure faster well completion. In-basin sand has grown from 20% of total supply in 2017 to over 70% by 2024 in regions like the Permian Basin. This trend reduces logistics costs by nearly 40% and enhances supply chain efficiency. Another trend is the increased use of high-intensity hydraulic fracturing, which uses more proppants per well. Average proppant usage has increased from 2,000 tons to 5,000 tons per horizontal well in key U.S. shale plays.

The adoption of coated and ceramic proppants is also increasing as operators seek higher conductivity and reduced fines production. Resin-coated proppants account for approximately 15% of the total demand in North America. Additionally, the rise of digital oilfields and real-time analytics in fracturing operations is influencing the way proppants are selected and deployed. Companies are using AI and machine learning to optimize proppant intensity, improve fracture geometry, and predict conductivity outcomes.

Environmental sustainability is emerging as a core focus in the Fracking Proppants market. There's rising demand for low-dust, environmentally-friendly proppants and biodegradable alternatives. Proppant recycling is being explored to reduce environmental footprints and improve operational economics. Lastly, global expansion into regions like Argentina’s Vaca Muerta and China’s Sichuan Basin is creating demand for locally manufactured and tailored proppants. These evolving trends indicate a dynamic future for the Fracking Proppants market with increasing innovation, regional diversification, and environmental considerations.

The fracking proppants market is comprehensively segmented based on type, application, and end-user insights. In terms of type, the fracking proppants market includes sand (frac sand), resin-coated proppants, ceramic proppants, ultra-lightweight proppants, and curable resin proppants. These fracking proppants types vary in performance, strength, conductivity, and cost, catering to specific geological formations and operational needs. Applications of fracking proppants include shale gas extraction, tight gas extraction, coalbed methane extraction, oil extraction, and deepwater offshore drilling. The fracking proppants market also varies based on end-user segments, including oil & gas industry, energy & utilities sector, petrochemical companies, exploration & production companies, and drilling service providers. The detailed segmentation enables precise targeting of proppant solutions in diverse drilling environments, enhancing efficiency in hydraulic fracturing operations across regions.

Sand (Frac Sand): Frac sand is the most widely used proppant in the fracking proppants market due to its low cost and abundant availability. Frac sand usage accounted for over 70% of proppant volume in U.S. hydraulic fracturing operations in 2023. Frac sand proppants offer sufficient strength for shallow to moderately deep wells and are typically composed of high-purity quartz silica. The fracking proppants market demand for frac sand is increasing with the proliferation of “in-basin sand” supply, reducing transport costs. Frac sand’s uniform grain size and roundness enhance permeability in fracked formations. The fracking proppants market continues to grow for frac sand, particularly in the Permian Basin.

Resin-coated Proppants: Resin-coated proppants are used in wells requiring enhanced conductivity and flowback control. These fracking proppants are typically applied over frac sand or ceramic cores with a resin layer to improve crush resistance and reduce proppant flowback. Resin-coated proppants constituted approximately 15% of the fracking proppants market volume in 2023. They are widely used in high-pressure environments where sand alone would crush. The fracking proppants market is adopting resin-coated options to extend well productivity and minimize environmental impacts from proppant migration. They are also favored in regions where regulatory concerns demand safer operations.

Ceramic Proppants: Ceramic proppants dominate the high-performance segment of the fracking proppants market. These proppants are manufactured from bauxite and kaolin and sintered at high temperatures, resulting in superior crush resistance. In 2023, ceramic proppants captured over 80% of demand in ultra-deep shale wells in China and Russia. The fracking proppants market benefits from ceramic proppants where high closure stress environments exist, as they maintain conductivity longer than sand. Their use in complex horizontal and multistage fracking wells is increasing. Although more expensive, ceramic proppants provide higher ROI due to improved hydrocarbon recovery.

Ultra-lightweight Proppants: Ultra-lightweight proppants are engineered to suspend easily in low-viscosity fluids and are designed for slickwater fracking. These proppants are gaining traction in the fracking proppants market for reducing water usage and enabling efficient delivery in complex formations. In 2023, ultra-lightweight proppants were deployed in more than 3,500 U.S. wells, showing rising demand. These proppants help in reducing equipment wear, operational downtime, and surface handling challenges. Their use improves well stimulation while reducing the total weight of transported material. The fracking proppants market is expected to see continued innovation in lightweight solutions.

Curable Resin Proppants: Curable resin proppants are an advanced class of resin-coated proppants used to bond under temperature and pressure during fracking. They are formulated to prevent proppant backflow and reduce sand production at the surface. In 2023, these fracking proppants gained attention for their use in ultra-tight formations in North America. Curable resin proppants maintain fracture integrity and increase hydrocarbon flow rates. The fracking proppants market is utilizing these proppants in sensitive environments where environmental and safety considerations are paramount. They also help reduce the costs associated with production damage and flow assurance issues.

Shale Gas Extraction: Shale gas extraction remains the dominant application in the fracking proppants market. The U.S. alone contributed over 80% of fracking proppants volume for shale gas production in 2023. Fracking proppants enable microfracture creation in tight shale formations, ensuring sustained gas flow. Proppants like ceramic and resin-coated sand are preferred in horizontal shale wells to maintain fracture conductivity. As countries like China and Argentina expand their shale reserves, the fracking proppants market is projected to grow proportionately. Innovations in shale-specific proppant blends are increasing well recovery rates and reducing operational costs across North America and Asia-Pacific.

Tight Gas Extraction: Tight gas reservoirs demand high-strength proppants due to extremely low permeability and high closure stress. The fracking proppants market is evolving with demand for curable resin and ceramic proppants in tight gas plays. In 2023, tight gas extraction accounted for nearly 20% of the proppant consumption in Asia and Eastern Europe. Proppant performance in tight gas fields directly impacts extraction efficiency and economic viability. The fracking proppants market benefits from specialized designs for tight gas stimulation where deeper and hotter wells are common. Technological advancements in real-time monitoring improve proppant placement accuracy in these reservoirs.

Coalbed Methane Extraction: Coalbed methane (CBM) reservoirs use lower-pressure fracking methods and therefore require lightweight and cost-effective proppants. The fracking proppants market for CBM is expanding in regions such as India, Australia, and China. In 2023, over 9,000 CBM wells were stimulated globally using tailored fracking proppants. Frac sand and ultra-lightweight proppants dominate this segment due to their affordability and suitability for low-pressure reservoirs. The fracking proppants market in CBM applications is focused on maximizing gas output while minimizing water usage. Environmentally safe proppants are gaining traction in this segment due to groundwater protection concerns.

Oil Extraction: Fracking proppants are widely used in tight oil formations to boost crude production. With growing tight oil operations in the U.S. Permian Basin and Canada's Montney Formation, the demand for fracking proppants has surged. In 2023, oil extraction consumed over 25 million tons of proppants globally. Ceramic and resin-coated proppants are preferred for high-yield oil wells. The fracking proppants market for oil extraction benefits from multistage hydraulic fracturing, where consistent proppant flow and placement are crucial. Increased drilling activities in Saudi Arabia and Brazil also contribute to fracking proppants demand in oil-focused reservoirs.

Deepwater Offshore Drilling: The fracking proppants market is slowly penetrating deepwater offshore drilling as technology enables hydraulic fracturing in undersea environments. These wells require ultra-high-performance proppants due to extreme depths and pressures. In 2023, pilot projects in the Gulf of Mexico and the North Sea tested ceramic proppants in subsea fracking. Though niche, the segment holds potential for growth as offshore operators seek to extend well productivity. The fracking proppants market in deepwater operations demands innovations in transportable, corrosion-resistant, and lightweight proppants. Challenges related to deployment logistics and environmental compliance influence proppant selection in this segment.

Oil & Gas Industry: The oil & gas industry is the primary end-user of the fracking proppants market. With over 90% of new oil and gas wells in the U.S. using hydraulic fracturing, the demand for proppants is constant. This sector drives innovation and bulk purchases of frac sand, ceramic proppants, and resin-coated materials. In 2023, the oil & gas sector consumed over 95 million tons of fracking proppants globally. The industry’s focus on enhanced oil recovery and unconventional resource development is fueling continued investment in proppant technology and logistics. Sustainability and performance remain top priorities in fracking proppants selection.

Energy & Utilities Sector: The energy & utilities sector relies on stable natural gas supplies for electricity generation and distribution. As this sector diversifies away from coal, it indirectly supports fracking proppants demand through increased shale gas extraction. In 2023, over 35% of utility-scale natural gas generation in North America was powered by shale gas. The fracking proppants market benefits from this energy transition, where efficient and eco-friendly proppant solutions are being promoted. The energy sector's regulatory compliance and environmental focus influence proppant formulation and selection, particularly around water use and emissions control.

Petrochemical Companies: Petrochemical manufacturers depend on stable supplies of natural gas liquids (NGLs), many of which originate from shale gas. The fracking proppants market plays a crucial role in sustaining high-volume NGL extraction. In 2023, petrochemical companies sourced over 40% of their feedstock from fracked gas wells. These firms often invest in upstream operations to ensure raw material security, increasing their role in proppant procurement. The fracking proppants market benefits from collaboration between petrochemical giants and fracking operators to align extraction capabilities with downstream demand trends.

Exploration & Production Companies: Exploration & Production (E&P) companies are at the forefront of fracking operations and are major consumers of fracking proppants. These companies choose proppant types based on geological data, formation pressure, and cost-efficiency. In 2023, E&P firms globally allocated more than 18% of their CAPEX to hydraulic fracturing, directly impacting fracking proppants demand. Their operational scale and well planning strategies influence bulk purchases and inventory of frac sand, ceramic, and resin-coated proppants. E&P firms focus on long-term well productivity and cost reduction through proppant innovation and supply chain optimization.

Drilling Service Providers: Drilling service providers act as intermediaries in the fracking proppants market by managing procurement, storage, and on-site deployment. They provide technical services, such as proppant mixing, hydraulic modeling, and pressure management. In 2023, leading oilfield service providers conducted over 55,000 fracking stages globally. These service providers influence the selection of proppants by integrating performance analytics, well logging data, and reservoir simulation results. Their feedback loops to manufacturers help improve fracking proppant designs and customization. This group’s operational knowledge enhances the fracking proppants market’s ability to innovate and respond to field demands.

The North America region accounted for the largest market share at 45.5% in 2024, however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 9.3% between 2025 and 2032.

The Fracking Proppants Market in North America is being driven by advanced oilfield infrastructure, high drilling rates, and widespread shale gas exploration, particularly in the United States and Canada. The Asia-Pacific region is experiencing accelerated growth in the Fracking Proppants Market due to the increased shale gas exploration initiatives in China, India, and Australia. Europe continues to witness slow but steady growth, while the Middle East & Africa is investing in unconventional oil & gas extraction, further boosting the demand for Fracking Proppants. The global adoption of hydraulic fracturing and horizontal drilling methods is creating significant regional opportunities in the Fracking Proppants Market.

High Demand from Shale Plays Drives North American Proppants Use

In North America, the Fracking Proppants Market is primarily dominated by the demand from extensive shale basins including the Permian, Bakken, Eagle Ford, and Marcellus formations. Over 90% of proppants used in the U.S. are frac sand, driven by its cost efficiency and effective conductivity. The Fracking Proppants Market is also benefiting from high rig counts and drilling activity across Texas and Pennsylvania. The use of resin-coated proppants is rising for high-pressure wells, particularly in deep shale zones. Canada contributes with investments in unconventional plays such as the Montney and Duvernay formations. The proppants supply chain is supported by a robust network of regional mines and logistics infrastructure in North America.

Advanced Technologies Fuel Proppants Demand in European Unconventional Plays

The Fracking Proppants Market in Europe is steadily gaining ground, especially in countries like the United Kingdom, Germany, and Poland, which are exploring domestic shale gas to reduce reliance on imports. In 2024, frac sand constituted over 52% of the total proppants used in Europe. Despite environmental opposition, advancements in fracking technologies and waterless fracturing methods are promoting project approvals. European companies are increasingly using ceramic proppants for wells requiring high crush resistance. Eastern European countries are investing in unconventional oil and gas as part of energy diversification strategies, expanding the Fracking Proppants Market footprint in the region.

Government Support and Shale Gas Push Accelerate Market Growth in Asia-Pacific

The Asia-Pacific Fracking Proppants Market is showing strong growth due to active shale gas developments in China, which accounted for over 60% of regional proppants demand in 2024. The Chinese government's 5-year plans promote increased domestic gas production to reduce coal dependency. India is initiating hydraulic fracturing operations in Assam and Gujarat, driving local demand for frac sand and resin-coated proppants. Australia continues fracking in the Beetaloo Basin, emphasizing high-strength proppants for deep wells. Indonesia and Malaysia are exploring unconventional resources, thus adding momentum to the Fracking Proppants Market across the Asia-Pacific region.

Exploration Activities Bolster Fracking Proppants Demand in MEA

In the Middle East & Africa, the Fracking Proppants Market is emerging rapidly, driven by unconventional resource development in Saudi Arabia, United Arab Emirates, and South Africa. In 2024, the region accounted for approximately 8.7% of global proppants demand, with expectations to grow further due to national strategies to diversify energy sources. Saudi Aramco is investing in hydraulic fracturing to extract tight gas, increasing the use of resin-coated and ceramic proppants. South Africa’s Karoo Basin shows promise for shale development, and proppants are essential to these efforts. Investment from global energy giants is boosting infrastructure and fracking operations, aiding the growth of the Fracking Proppants Market.

The Fracking Proppants Market is highly competitive, with several established and emerging players focusing on cost efficiency, quality, and technological innovation. Major players are increasing their proppant production capacities and expanding geographically to meet rising demand from shale gas, tight gas, and deep oil wells. Market participants are also investing in resin-coating technologies, ultra-lightweight proppants, and logistics optimization to maintain a competitive edge. In 2024, the top five companies accounted for over 40% of the global proppants supply. Mergers, acquisitions, and strategic collaborations remain common across the Fracking Proppants Market, particularly between proppant manufacturers and upstream drilling firms. Players are focusing on sustainability and recycling of proppants, which is creating new product lines and service offerings to support unconventional hydrocarbon extraction.

CARBO Ceramics Inc.

U.S. Silica Holdings, Inc.

Smart Sand Inc.

Hi-Crush Inc.

Hexion Inc.

Saint-Gobain Proppants

Mineração Curimbaba

Fairmount Santrol Holdings Inc.

Badger Mining Corporation

China GengSheng Minerals Inc.

The fracking proppants market is undergoing a technological transformation, driven by innovations in extraction techniques, digitalization, and material engineering. One of the most significant developments is the deployment of high-performance proppants designed to maintain conductivity in ultra-deep and high-temperature wells. Ceramic proppants with enhanced thermal stability are now being used for shale plays that reach temperatures exceeding 300°F. These proppants offer superior crush resistance and help maximize hydrocarbon flow.

Automation is another major driver. Advanced automated proppant loading systems have reduced loading times by 40% and minimized manual errors. Companies like Halliburton and Liberty Energy have integrated digital twin technologies in well planning, allowing real-time proppant tracking and dynamic adjustment during fracturing. The integration of cloud-based platforms and edge analytics is enabling predictive maintenance of proppant handling equipment, decreasing downtime by up to 25%.

Furthermore, environmentally friendly technologies are emerging. Bio-resin-coated proppants and recyclable sand blends are gaining popularity for reducing environmental impact. These sustainable solutions are meeting regulatory compliance and corporate ESG goals. The overall emphasis on intelligent proppant solutions, data-driven well design, and eco-safe operations is redefining the competitive edge in the global fracking proppants market.

• In March 2023, U.S. Silica Holdings increased frac sand output by over 2 million tons annually to support booming shale plays in the Permian Basin, addressing the supply-demand gap and optimizing logistics for regional drilling operations.

• In May 2023, Covia introduced “Self-Suspending Proppants” (SSPs) that eliminate the need for gel-based fluids. This innovation reduces water consumption by 10% and fluid viscosity by 30%, enhancing fracture placement and cost efficiency.

• In October 2023, Hexagon Digital Wave partnered with a leading fracking company to deploy smart proppant flow sensors that improved real-time data capture during hydraulic fracturing. The system enhanced operational control and reduced non-productive time by 15%.

• In January 2024, Smart Sand Inc. launched a fully electric proppant delivery system that cut diesel usage in last-mile logistics by 90%, supporting environmental sustainability and reducing delivery time by 20%.

• In February 2024, CARBO Ceramics introduced an AI-enhanced fracture simulation tool to determine optimal proppant size and distribution. Early tests showed a 12% increase in well productivity across three test fields in Texas.

The scope of the fracking proppants market report encompasses a comprehensive analysis of market trends, growth drivers, technological advancements, and competitive landscape. This report provides insights into key segments such as proppant types—frac sand, resin-coated proppants, ceramic proppants, ultra-lightweight proppants, and curable resin proppants. Applications evaluated include shale gas extraction, tight gas extraction, coalbed methane extraction, oil extraction, and deepwater offshore drilling. The report also investigates demand patterns across end-user sectors like the oil & gas industry, energy & utilities, petrochemical firms, exploration companies, and drilling service providers.

Regionally, the report offers in-depth insights into North America, Europe, Asia-Pacific, and the Middle East & Africa, analyzing factors like production output, resource availability, and drilling intensity. It also includes an overview of recent technological innovations and sustainability efforts transforming the industry. This market analysis provides actionable intelligence for manufacturers, suppliers, logistics operators, and investors seeking to navigate the evolving fracking proppants landscape. The report emphasizes trends such as digitalization, automation, and eco-friendly solutions—enabling stakeholders to align strategies with future market needs. Fracking proppants market growth is further fueled by the increasing depth and complexity of unconventional drilling operations.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 84,557.8 Million |

|

Market Revenue in 2032 |

USD 113,954.77 Million |

|

CAGR (2025 - 2032) |

8.8% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types:

By Application:

By End-User:

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

CARBO Ceramics Inc., U.S. Silica Holdings, Inc., Smart Sand Inc., Hi-Crush Inc., Hexion Inc., Saint-Gobain Proppants, Mineração Curimbaba, Fairmount Santrol Holdings Inc., Badger Mining Corporation, China GengSheng Minerals Inc. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |