Reports

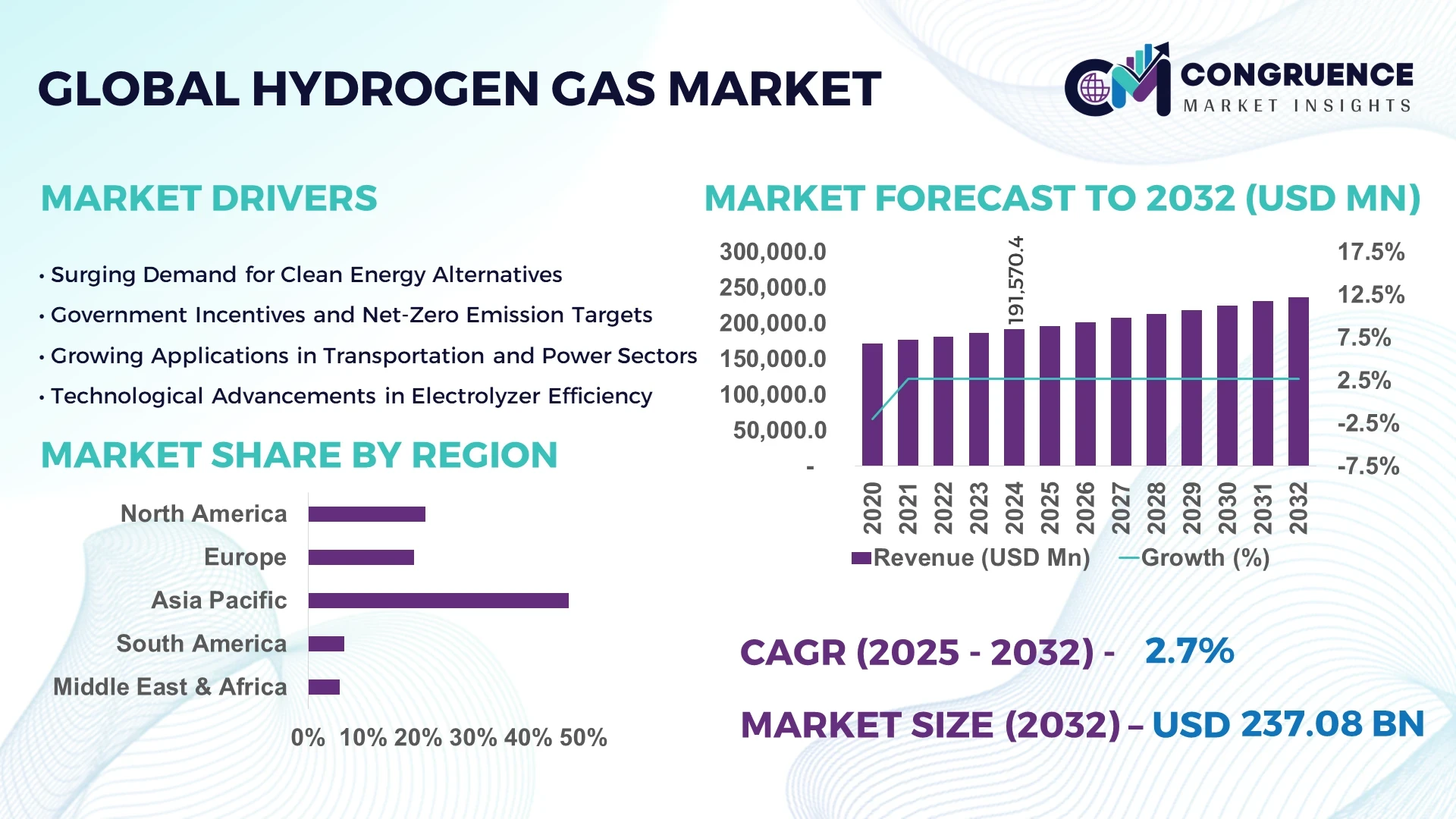

The Global Hydrogen Gas Market was valued at USD 191,570.42 Million in 2024 and is anticipated to reach a value of USD 237,078.41 Million by 2032 expanding at a CAGR of 2.7% between 2025 and 2032.

In the United States, the hydrogen gas market is seeing accelerated momentum due to government-backed energy transition policies and rapid industrial decarbonization strategies. The U.S. Department of Energy has launched the Hydrogen Energy Earthshot initiative aiming to reduce the cost of clean hydrogen by 80% to $1 per 1 kilogram in one decade. The U.S. is emerging as a hub for hydrogen gas production, driven by public-private partnerships and the establishment of hydrogen hubs in Texas, California, and the Midwest. Hydrogen gas is increasingly used in oil refining, ammonia production, and heavy transport applications across the U.S. manufacturing, energy, and automotive sectors. In particular, the U.S. market is benefitting from robust investment in electrolyzer technology and renewable hydrogen projects, significantly boosting domestic hydrogen gas production and usage.

Artificial Intelligence is significantly transforming the hydrogen gas market by optimizing production, enhancing operational efficiency, and minimizing risk. AI in the hydrogen gas sector is used extensively in predictive maintenance, process simulation, and supply-demand forecasting. In hydrogen production plants, AI algorithms monitor real-time variables such as pressure, temperature, and feedstock composition to automatically adjust parameters for maximum hydrogen yield. This application of AI has improved hydrogen plant efficiency by up to 15% in trial runs, according to independent research institutions.

AI also enables anomaly detection in hydrogen gas pipelines and storage tanks, drastically reducing the chances of leakages and accidents. Using machine learning models, energy companies can predict equipment failures weeks before they occur, helping to cut maintenance costs by 20% or more. Moreover, AI-powered logistics tools are optimizing the distribution of hydrogen gas, ensuring timely delivery and minimizing spoilage or inefficiencies in supply chains.

In hydrogen fuel cell development, AI plays a role in material discovery and performance prediction, allowing companies to accelerate R&D processes. Companies are leveraging AI to analyze large datasets from field tests and simulations, helping shorten the design cycle for hydrogen fuel systems by 30%. Overall, the hydrogen gas market is witnessing AI-driven innovation that reduces costs, improves safety, and enhances scalability across various industrial applications.

"In 2024, a major AI development in the hydrogen gas market involved the use of machine learning algorithms to optimize the operation of hydrogen electrolyzers. A partnership between Siemens Energy and a leading AI firm resulted in AI-driven advancements that increased the efficiency of hydrogen production by 15%, enabling cost reductions and enhanced scalability."

The hydrogen gas market is influenced by multiple dynamics, including technological advancements, regulatory policies, energy transition goals, industrial demand, and sustainability initiatives. Market drivers such as increasing hydrogen applications in transportation and clean energy generation are propelling demand. Simultaneously, restraints such as high production costs and infrastructure limitations are hampering rapid adoption. However, opportunities exist in green hydrogen, while challenges persist in achieving global standardization and safety regulation compliance.

Rising demand for hydrogen in clean energy applications

Hydrogen gas is increasingly being used as a clean energy source across power generation and transportation sectors. In 2023, over 680 large-scale hydrogen projects were announced globally, reflecting a growing commitment to decarbonization. In transportation, hydrogen fuel cell vehicle (FCV) registrations grew by 30% year-over-year, showcasing consumer shift toward zero-emission vehicles. In the steel sector, hydrogen gas is being used as an alternative to coke for direct reduced iron (DRI) production, reducing carbon emissions by up to 90%. The European Union’s Fit for 55 initiative targets 50% hydrogen use in industrial energy needs by 2030, reinforcing strong global demand.

High cost of hydrogen production and distribution

The cost of producing low-carbon hydrogen gas—especially green hydrogen—remains significantly higher than conventional fossil-based hydrogen. As of 2024, green hydrogen production costs range from $4 to $6 per kilogram, compared to $1 to $2 per kilogram for grey hydrogen. The lack of hydrogen refueling infrastructure also limits deployment of fuel cell electric vehicles (FCEVs). Pipeline retrofitting to transport hydrogen gas requires major capital investment, and only 4% of current global gas pipelines can support hydrogen blending. Additionally, hydrogen storage requires high-pressure systems and cryogenic tanks, adding logistical complexities and increasing operating expenses for stakeholders.

Expansion of green hydrogen and renewable integration

The global shift toward renewable energy sources presents enormous opportunities for hydrogen gas, particularly green hydrogen. More than 50 countries have released national hydrogen strategies, with targets to produce over 300 million tons of hydrogen annually by 2050. Renewable-rich countries are leveraging solar and wind energy to produce hydrogen through water electrolysis. For example, Australia and Chile are building 10+ GW scale hydrogen plants linked to wind farms. The integration of green hydrogen into power grids can help balance renewable variability, creating decentralized energy systems. The energy storage potential of hydrogen gas, combined with grid flexibility, opens up new use cases and revenue models.

Technical and regulatory complexity in hydrogen infrastructure

Hydrogen gas infrastructure development faces multifaceted challenges. Hydrogen’s low volumetric density makes its storage and transport difficult, requiring specialized tanks and pipelines. Technical issues such as hydrogen embrittlement can degrade metal components, posing safety hazards. Additionally, the absence of standardized safety regulations across countries hinders global hydrogen adoption. Cross-border transport regulations remain inconsistent, causing delays in export projects. In 2024, fewer than 20% of global ports had the capacity to handle hydrogen exports, severely limiting international trade. The lack of skilled labor and hydrogen-specific trainng programs further adds to the operational and regulatory barriers in scaling hydrogen gas infrastructure.

Hydrogen gas market trends indicate a clear pivot toward clean energy and decarbonization. One of the strongest trends is the surge in green hydrogen investments, with over $320 billion announced globally in hydrogen-related projects as of early 2024. Electrolyzer capacity worldwide increased by over 130% in 2023 alone, with PEM (Proton Exchange Membrane) technology gaining the highest adoption rate due to its efficiency in renewable hydrogen production. Another rising trend is the commercialization of hydrogen fuel cell vehicles (FCEVs). Over 72,000 FCEVs are now in operation globally, with Asia-Pacific leading in market penetration.

Decentralized hydrogen production is gaining traction, especially in off-grid and island communities where hydrogen serves as both a fuel and a storage medium. Industrial decarbonization using hydrogen is trending across cement, glass, and steel manufacturing sectors. Countries like Germany, Japan, and South Korea are providing subsidies and tax incentives for companies integrating hydrogen into their processes.

Additionally, digitalization and smart hydrogen plants are emerging, utilizing IoT and AI for real-time optimization and data-driven decision-making. Carbon capture and utilization (CCU) in conjunction with blue hydrogen production is another major trend, with more than 45 pilot projects launched globally in the past year. These trends collectively showcase the evolving nature of the hydrogen gas market, positioning it as a cornerstone of global energy transition and sustainable industrial development.

The hydrogen gas market can be segmented based on type, application, and end-user insights. These categories provide a comprehensive view of the market’s growth, key trends, and regional developments. Understanding the segmentation is crucial to identifying where investment opportunities exist and where consumer demand is shifting. The three major types of hydrogen gas are Green, Grey, and Blue hydrogen, each with different production methods and environmental implications. In terms of applications, hydrogen is used extensively in sectors like transportation, industrial applications, power generation, oil refining, and electronics manufacturing. From an end-user perspective, the automotive, chemical, and steel manufacturing industries represent significant sectors driving the demand for hydrogen gas. Each of these categories plays a vital role in shaping the market’s future, with increasing demand for cleaner energy solutions and advancing technologies.

Green Hydrogen: Green hydrogen is produced using renewable energy sources such as wind, solar, or hydropower through the process of electrolysis, where water is split into hydrogen and oxygen. The main appeal of green hydrogen lies in its zero-emission nature, making it a key component of decarbonizing various industries. As of 2023, global green hydrogen production is estimated to be around 0.1 million tonnes, but with growing investments and technological advancements, this number is expected to see substantial growth in the coming years. Countries like Germany, Australia, and the US are leading green hydrogen initiatives, supported by large-scale government funding and policy incentives. Green hydrogen’s adoption in the transport sector, particularly for heavy-duty vehicles, as well as in industry and power generation, is expected to drive its demand significantly.

Grey Hydrogen: Grey hydrogen is produced from natural gas through a process known as steam methane reforming (SMR), which emits a significant amount of CO2. This type of hydrogen remains dominant in the market due to its cost-effectiveness compared to green hydrogen. However, with growing concerns over its environmental impact, the demand for grey hydrogen is projected to plateau in favor of more sustainable alternatives like green hydrogen. Grey hydrogen accounts for roughly 96% of global hydrogen production today. While it remains a vital hydrogen source for industries such as ammonia production and refining, increasing regulatory pressures and the need for decarbonization are expected to shift the market away from grey hydrogen in the long term.

Blue Hydrogen: Blue hydrogen is also produced through the steam methane reforming process, but with the addition of carbon capture and storage (CCS) technologies to capture CO2 emissions. This type of hydrogen offers a lower-carbon alternative to grey hydrogen and is considered a bridge technology in the transition to cleaner hydrogen sources. By 2025, blue hydrogen production is expected to reach around 10 million tonnes globally, with major production hubs in the US, Canada, and the Middle East. Blue hydrogen is particularly attractive for industries looking for a lower-cost solution to decarbonization, including the steel, refining, and petrochemical sectors. The success of blue hydrogen is highly contingent on the widespread adoption of CCS technologies, as well as regulatory support.

Transportation: The transportation sector is one of the largest consumers of hydrogen, especially for fuel cell electric vehicles (FCEVs) and heavy-duty transportation, including trucks and buses. Hydrogen-powered vehicles offer a range advantage over battery electric vehicles (BEVs) and are particularly beneficial for long-distance, heavy-duty applications. In 2022, the global fleet of hydrogen-powered vehicles surpassed 10,000 units, and it is expected to grow substantially in the coming years. This increase is supported by government subsidies, such as those in Japan and Europe, aimed at reducing carbon emissions in the transport sector. Hydrogen's potential in aviation, where it can be used to power aircraft with zero emissions, is also gaining momentum, with major airlines exploring hydrogen-powered flight prototypes.

Industrial Applications: Hydrogen plays a crucial role in various industrial applications, particularly in the production of ammonia, methanol, and petroleum refining. Hydrogen is a key feedstock in ammonia synthesis, which is essential for fertilizers. The global ammonia production was estimated to be over 200 million tonnes in 2020, with hydrogen being the primary input. In refining, hydrogen is used for desulfurization processes, helping refineries meet stringent environmental regulations. The rise of hydrogen adoption in industries, coupled with increasing efforts to reduce carbon footprints, is expected to accelerate the demand for hydrogen in industrial applications.

Power Generation: Hydrogen is emerging as a promising solution for power generation, particularly for grid stabilization and decarbonizing power plants. It can be used in gas turbines, fuel cells, and other power generation technologies. Hydrogen’s potential to store energy, particularly in the form of green hydrogen, offers an alternative to traditional energy storage methods. Countries like Japan and Germany are investing heavily in hydrogen-based power generation, with pilot projects underway. In 2023, the global hydrogen-based power generation capacity was around 2.5 GW, with projections for rapid growth in the next decade as the energy transition accelerates.

Oil Refining: In oil refining, hydrogen is primarily used for hydrocracking and desulfurization processes. These processes help improve the quality of refined products like gasoline and diesel, ensuring they meet environmental standards. As of 2023, hydrogen consumption in refineries globally was estimated to be approximately 9 million tonnes. The demand for hydrogen in oil refining is expected to grow steadily, particularly as refiners are under pressure to reduce the carbon intensity of their operations and increase the use of cleaner fuels.

Electronics Manufacturing: Hydrogen is used in electronics manufacturing for various purposes, including the production of semiconductors and flat-panel displays. In the semiconductor industry, hydrogen is used as a reducing agent during the production of silicon wafers. The demand for hydrogen in this sector is expected to increase alongside the growing demand for consumer electronics, particularly smartphones, laptops, and electric vehicles. In 2022, the global hydrogen consumption in electronics manufacturing was estimated to be around 0.3 million tonnes, with an upward trend due to the expansion of the electronics sector.

Automotive Industry: The automotive industry is one of the key end-users of hydrogen, particularly in the development of hydrogen fuel cell vehicles (FCVs). Hydrogen offers automotive manufacturers a viable alternative to battery electric vehicles, especially for applications requiring long driving ranges and quick refueling times. Major automakers such as Toyota, Hyundai, and Honda have already launched commercial hydrogen-powered vehicles. The global FCV market is expected to reach 10 million units by 2030. Hydrogen is seen as a crucial component in decarbonizing the automotive sector, especially for heavy-duty vehicles, such as trucks and buses, where batteries are less efficient than hydrogen.

Chemical Industry: Hydrogen is a fundamental feedstock in the chemical industry, particularly for the production of ammonia, methanol, and other chemicals. As of 2023, hydrogen is used in the production of over 150 million tonnes of ammonia annually, which is essential for fertilizer manufacturing. The chemical industry’s reliance on hydrogen is expected to grow as companies strive to meet stricter environmental regulations and reduce their carbon footprint. Green hydrogen’s increasing availability is expected to play a crucial role in this transition, providing the chemical industry with cleaner alternatives for its operations.

Steel Manufacturing: Steel manufacturing is another significant sector driving the demand for hydrogen, especially in the development of direct reduction iron (DRI) processes. Hydrogen-based DRI offers a cleaner alternative to traditional blast furnaces, which are major contributors to CO2 emissions. The hydrogen-based steel production process is gaining traction in countries like Sweden and Germany, with pilot projects underway. The global steel industry’s hydrogen consumption is expected to rise sharply, with the potential to reduce emissions by 70-90% in the coming decades.

Asia-Pacific accounted for the largest market share at 47.3% in 2024; however, North America is expected to register the fastest growth, expanding at a CAGR of 3.4% between 2025 and 2032.

Asia-Pacific leads due to strong industrial demand and national hydrogen strategies from China, Japan, and South Korea. North America is rapidly catching up with hydrogen infrastructure funding, clean energy mandates, and the integration of hydrogen in transportation and power sectors. Europe maintains robust hydrogen innovation, especially in mobility and green hydrogen, while the Middle East & Africa are emerging players, focusing on hydrogen exports using solar-powered electrolyzers.

Federal Funding and Mobility Infrastructure Driving Clean Hydrogen Growth

North America’s hydrogen gas market is booming due to federal funding, tax credits, and infrastructure expansion. The U.S. government allocated over $9.5 billion under the Bipartisan Infrastructure Law for hydrogen hubs. California has deployed more than 50 hydrogen fueling stations, leading nationwide in FCEV adoption. Canada is investing in electrolyzer production, targeting 15% of energy from hydrogen by 2050. Industrial users in oil refining and steel are transitioning from grey to blue hydrogen. The transportation sector is witnessing increased deployment of hydrogen-powered buses, with over 300 in service across major U.S. cities by end-2024.

Green Hydrogen Innovation Anchored by EU Strategy and Cross-Border Infrastructure

Europe is at the forefront of hydrogen innovation. The EU’s Hydrogen Strategy targets 40 GW of renewable hydrogen electrolyzers by 2030. Germany alone has committed over €9 billion to hydrogen technologies. France and the Netherlands are integrating hydrogen into mobility and heating networks. Europe operates over 200 hydrogen refueling stations and is a leader in fuel cell buses. Hydrogen trains (e.g., Alstom Coradia iLint) are running in Germany. Industrial decarbonization in steel and fertilizer plants is pushing hydrogen demand. The European Hydrogen Backbone project aims to connect 28,000 km of dedicated hydrogen pipelines by 2040.

Massive Production Capacity and Green Hydrogen Transition Leading Global Momentum

Asia-Pacific dominates hydrogen production and consumption, led by China, Japan, South Korea, and Australia. China produces over 33 million tons of hydrogen annually, primarily from coal and natural gas, and is transitioning toward green hydrogen. Japan is promoting hydrogen in homes and vehicles, with over 160,000 residential fuel cells installed. South Korea aims to deploy 200,000 FCEVs by 2025. Australia is building mega green hydrogen projects powered by solar and wind. The Asia-Pacific market benefits from robust government support, technological innovation, and massive industrial hydrogen demand across petrochemicals, refining, and electronics sectors.

Green Hydrogen Export Hub Powered by Renewable Energy and Strategic Roadmaps

The Middle East & Africa hydrogen gas market is emerging as a global export powerhouse. Saudi Arabia is constructing the NEOM green hydrogen plant with 4 GW capacity. The UAE is developing hydrogen infrastructure through the ""Hydrogen Leadership Roadmap,"" targeting 25% of hydrogen exports by 2030. South Africa is investing in hydrogen valleys to support platinum-based fuel cells. Egypt and Morocco are building electrolysis-based hydrogen projects with EU collaboration. The region’s abundant solar resources enable low-cost renewable hydrogen production, making it a future hub for green hydrogen exports to Europe and Asia.

The hydrogen gas market is highly competitive, with numerous players across different segments of production, distribution, and technological development. Major players include industrial gas companies, energy producers, and specialized technology providers. The competition in the hydrogen space is increasing as governments around the world push for cleaner energy solutions and a decarbonized economy. Companies are focusing on large-scale hydrogen production, particularly green and blue hydrogen, as well as on the development of hydrogen infrastructure, including transportation and storage solutions. Key players are investing heavily in research and development to improve hydrogen production efficiency, reduce costs, and expand the hydrogen ecosystem. Major companies are also forming strategic partnerships to create hydrogen hubs and commercialize fuel cell technology for sectors like transportation and power generation.

Air Liquide

Linde Group

Siemens Energy

Cummins Inc.

Plug Power

Air Products and Chemicals, Inc.

Shell

ITM Power

Nel ASA

Ballard Power Systems

Hydrogenics Corporation

Mitsubishi Heavy Industries, Ltd.

The hydrogen gas market is witnessing rapid technological advancements aimed at improving production efficiency, reducing costs, and enhancing the scalability of hydrogen solutions. Electrolysis technology is one of the key methods for producing green hydrogen, where water is split into hydrogen and oxygen using renewable electricity. Proton exchange membrane (PEM) electrolyzers and alkaline electrolyzers are leading the charge in this space. Additionally, advancements in steam methane reforming (SMR) with carbon capture and storage (CCS) are enabling the production of blue hydrogen. The development of hydrogen storage solutions, including metal hydride storage and liquid hydrogen systems, is crucial for increasing hydrogen's viability as a transportation fuel. Fuel cell technology continues to advance, with companies improving the efficiency of fuel cells for use in transportation, power generation, and industrial applications. Furthermore, digital technologies such as AI and big data are being integrated into hydrogen production and distribution to optimize processes and enhance grid management, contributing to the broader adoption of hydrogen as a clean energy source.

In March 2024, India's state-owned natural gas company, GAIL Ltd., launched its first green hydrogen project in central India. Utilizing a 10 MW PEM electrolyzer unit imported from Canada, the facility is set to produce 4.3 tons per day (TPD) of green hydrogen by electrolyzing water with renewable energy, marking a significant milestone in India’s clean energy transition.

In May 2024, ITM Power launched the NEPTUNE V, a containerized 5 MW PEM electrolyzer plant priced at £4.35 million. This development underscores ITM Power's commitment to scaling up green hydrogen production capabilities and supporting large-scale industrial applications across Europe.

In June 2024, LAPP introduced the ETHERLINE® FD bioP Cat.5e, its first bio-based Ethernet cable produced in series. This sustainable variant features a bio-based outer sheath composed of 43% renewable raw materials, reducing the carbon footprint by 24% compared to traditional fossil-based TPU sheaths.

In December 2023, SK E&S Co. Ltd announced the addition of South Korea's largest low-carbon hydrogen plant to their global partnership initiatives. This development is part of efforts to foster a domestic hydrogen economy and increase low-carbon hydrogen production.

In June 2024, LAPP introduced the ETHERLINE® FD bioP Cat.5e, its first bio-based Ethernet cable produced in series. This sustainable variant features a bio-based outer sheath composed of 43% renewable raw materials, reducing the carbon footprint by 24% compared to traditional fossil-based TPU sheaths.

The global hydrogen gas market is undergoing a significant transformation, driven by the increasing demand for clean and sustainable energy solutions. Hydrogen gas plays a pivotal role in various industries, including transportation, power generation, and chemical manufacturing. The market encompasses different types of hydrogen production methods, such as gray, blue, and green hydrogen, each with varying environmental impacts. Green hydrogen, produced using renewable energy sources, is gaining prominence due to its zero-emission profile. Governments worldwide are implementing policies and providing incentives to promote hydrogen production and infrastructure development. For instance, the European Union aims to produce 10 million tons and import an additional 10 million tons of hydrogen by 2030. In Asia-Pacific, countries like China and Japan are investing heavily in hydrogen technologies to reduce carbon emissions and enhance energy security. The market also includes various applications, such as fuel cell vehicles, industrial processes, and energy storage systems. With ongoing technological advancements and increasing investments, the hydrogen gas market is expected to play a pivotal role in the global energy transition.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 191,570.42 Million |

|

Market Revenue in 2032 |

USD 237,078.41 Million |

|

CAGR (2025 - 2032) |

2.7% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Linde Group, Air Liquide, Air Products, Air Water, Taiyo Nippon Sanso, Messer Group, Yinde Gas, Meijin Energy, Donghua Energy, Sinopec, Huachang Chemical |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |