Reports

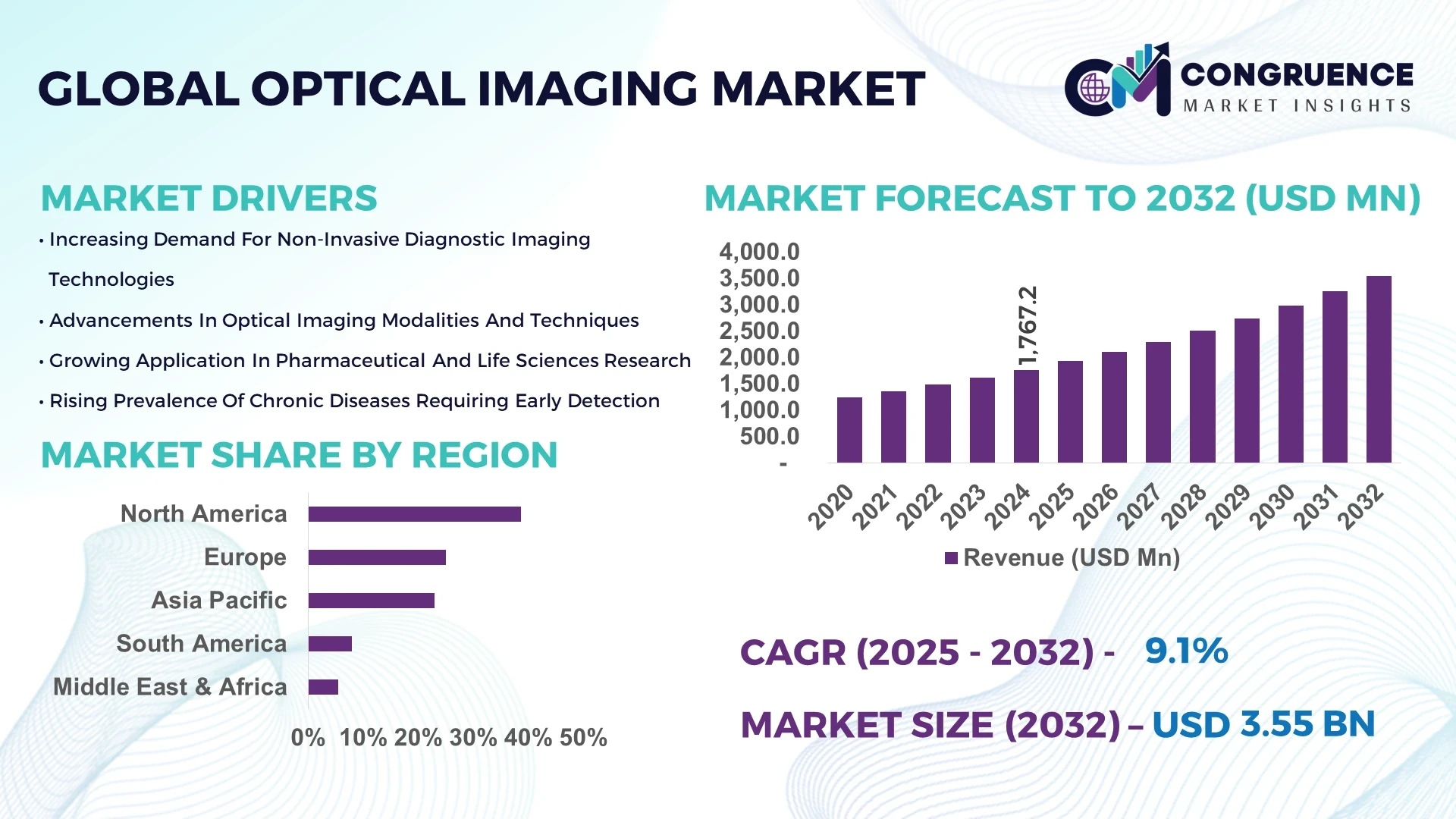

The Global Optical Imaging Market was valued at USD 1767.2 Million in 2024 and is anticipated to reach a value of USD 3547.18 Million by 2032, expanding at a CAGR of 9.1% between 2025 and 2032.

This growth trajectory is fueled by the increasing demand for non-invasive diagnostic procedures, advancements in imaging technologies, and the rising prevalence of chronic diseases.Optical imaging techniques, such as Optical Coherence Tomography (OCT) and Near-Infrared Spectroscopy (NIRS), are gaining traction due to their ability to provide high-resolution images without the need for ionizing radiation.The integration of these technologies into various medical fields, including ophthalmology, oncology, and cardiology, is enhancing diagnostic accuracy and patient outcomes.Moreover, the market is witnessing a surge in research and development activities aimed at improving imaging modalities and expanding their applications beyond traditional boundaries.The adoption of optical imaging is also being propelled by the growing emphasis on early disease detection and personalized medicine, which require precise and detailed imaging solutions.As healthcare systems worldwide continue to prioritize patient-centric approaches, the optical imaging market is poised for significant expansion, offering innovative solutions that cater to the evolving needs of modern medicine.

Artificial Intelligence (AI) is revolutionizing the optical imaging market by enhancing image analysis, improving diagnostic accuracy, and streamlining workflows.AI algorithms can process vast amounts of imaging data rapidly, identifying patterns and anomalies that might be imperceptible to the human eye.This capability is particularly beneficial in fields like oncology and ophthalmology, where early detection of diseases can significantly impact treatment outcomes.For instance, AI-powered tools are being developed to assist in the early detection of cancers by analyzing optical imaging data to identify malignant tissues with high precision.In ophthalmology, AI algorithms are aiding in the diagnosis of conditions such as diabetic retinopathy and age-related macular degeneration by evaluating retinal images.The integration of AI into optical imaging systems also facilitates real-time analysis, enabling clinicians to make informed decisions promptly.Furthermore, AI-driven automation reduces the workload on healthcare professionals by handling routine tasks, allowing them to focus on more complex cases.The continuous advancement of AI technologies is expected to further enhance the capabilities of optical imaging, making it an indispensable tool in modern diagnostics.

"In April 2025, the University of Pittsburgh partnered with Leidos in a $10 million initiative to combat cancer and heart disease using AI-enhanced optical imaging. This collaboration focuses on developing AI tools that improve diagnostic speed and accuracy, particularly benefiting underserved communities."

The dynamics of the optical imaging market are shaped by a combination of technological innovation, healthcare infrastructure development, and the global shift toward non-invasive diagnostics. Increasing demand for high-resolution, real-time imaging tools is promoting the development of portable, compact devices. Simultaneously, government funding for medical imaging innovation and AI integration is enhancing diagnostic accuracy and expanding clinical adoption.

Rising Demand for Non-Invasive Diagnostic Procedures

Optical imaging is gaining popularity due to its non-invasive, radiation-free approach, making it ideal for routine screenings and long-term monitoring. Optical Coherence Tomography (OCT) and Near-Infrared Spectroscopy (NIRS) offer high-resolution visualization of tissues, supporting early detection of diseases. This has accelerated its use in ophthalmology, cardiology, and oncology. Patients increasingly prefer diagnostic tools that reduce discomfort and risks associated with invasive procedures. With the rise of chronic illnesses, optical imaging systems are now vital for preventive diagnostics. As portable imaging technologies evolve, their role in outpatient and home-care settings is expanding rapidly.

High Cost of Advanced Imaging Systems

The high acquisition and maintenance cost of optical imaging systems is a major market restraint. These systems require expensive components such as tunable lasers, advanced detectors, and high-speed data processors. Additionally, operator training and infrastructure upgrades add to capital expenditure. Smaller clinics and hospitals often find it difficult to justify the investment without adequate reimbursement support. In many regions, limited insurance coverage for optical imaging procedures restricts adoption. Cost concerns are particularly acute in emerging markets, where budget constraints hinder technology deployment. As a result, many providers rely on outdated diagnostic tools, limiting overall market growth.

Expansion in Emerging Economies

Emerging markets such as India, China, Brazil, and Indonesia present significant growth opportunities. These regions are witnessing rapid growth in healthcare infrastructure, medical tourism, and investment in diagnostic technology. The increasing burden of lifestyle-related diseases and cancer is fueling demand for early diagnostic tools. Government-backed public health initiatives and expanding private healthcare facilities are enabling faster adoption of optical imaging systems. Training partnerships and collaborations with global players are creating local expertise and service networks. As device manufacturers offer cost-effective and portable imaging solutions, the penetration of optical imaging into remote and underserved regions is steadily improving.

Limited Skilled Professionals

A major challenge in the optical imaging market is the scarcity of trained operators and image analysts. Optical imaging systems require specialized knowledge to operate effectively and to interpret the images accurately. In developing countries and smaller healthcare facilities, this talent pool is significantly limited. Rapid advancements in AI and imaging algorithms further increase the need for continuous upskilling. This lack of expertise results in underutilization of equipment and diagnostic errors. Healthcare institutions struggle to train and retain qualified professionals. Bridging this skills gap through structured training programs and professional certification will be essential to unlock the full potential of this technology.

Several trends are currently shaping the global optical imaging market. First, artificial intelligence integration is significantly improving diagnostic precision and workflow automation. AI is being used to enhance image clarity, reduce noise, and automate the interpretation of high-resolution optical scans. Secondly, the market is witnessing the emergence of portable and handheld imaging systems, making real-time imaging accessible in field diagnostics and rural clinics. Third, hybrid imaging techniques that combine optical imaging with MRI or PET are becoming popular due to their improved functional and structural assessment capabilities. Another notable trend is the application of optical imaging in pharmaceutical research and drug development. Scientists are now using real-time molecular-level imaging to understand disease progression and therapy response. Furthermore, telemedicine adoption is pushing demand for remote diagnostic solutions, with optical imaging becoming central to virtual consultations. Regulatory agencies are also showing increased support by approving more optical imaging devices for clinical use, which accelerates their commercialization. These trends collectively indicate a robust future for the market as technologies evolve and adoption increases globally.

The global optical imaging market is segmented based on product type, application, and end-user insights, each playing a crucial role in shaping market trends. The type segment includes Optical Coherence Tomography (OCT), Fluorescence Imaging, Hyperspectral Imaging, Near-Infrared Spectroscopy (NIRS), and Confocal Microscopy, each offering unique imaging advantages across various clinical and industrial domains. In terms of application, optical imaging is widely adopted in medical diagnostics, life sciences research, pharmaceutical development, industrial inspection, and agriculture & food testing, owing to its non-invasive nature and high spatial resolution. End-user insights reveal the market’s increasing penetration across hospitals and clinics, research & academic institutes, pharmaceutical & biotechnology companies, diagnostic imaging centers, and agricultural enterprises. The growing demand for early diagnosis, rapid screening, and research precision is driving adoption across all segments. Advanced imaging integration in point-of-care systems and clinical research tools is further boosting demand globally, particularly in developed markets and expanding regions such as Asia-Pacific and Latin America.

Optical Coherence Tomography (OCT): OCT dominates the optical imaging market due to its high-resolution cross-sectional imaging capabilities, particularly in ophthalmology. It enables real-time monitoring of the retina, cornea, and optic nerve with micrometer precision. Over 35 million OCT scans are performed annually in the U.S. alone. Its utility is expanding into cardiology for plaque assessment and oncology for tumor margin detection. Technological advancements have led to the development of swept-source and spectral-domain OCT, providing enhanced penetration and faster acquisition rates. Portable OCT devices are also making headway in primary care and mobile diagnostics. OCT’s efficiency in diagnosing diabetic retinopathy and glaucoma drives global demand.

Fluorescence Imaging: Fluorescence imaging is widely used in oncology and intraoperative imaging due to its ability to visualize molecular activity and tissue pathology in real-time. In 2024, over 40% of clinical imaging studies used fluorescence agents for improved visualization. It enables surgeons to identify tumor boundaries and critical anatomical structures with precision. Its use is expanding in sentinel lymph node mapping and angiography. The development of near-infrared fluorescence contrast agents enhances depth and sensitivity. Fluorescence-guided surgery has been adopted in more than 3,000 hospitals worldwide. With applications in drug discovery and cell imaging, fluorescence imaging continues to play a critical diagnostic role.

Hyperspectral Imaging: Hyperspectral imaging integrates spectroscopy and imaging for the identification of materials and biological structures at the molecular level. It is gaining popularity in tissue analysis, wound assessment, and precision agriculture. Each pixel provides spectral information, allowing detection of abnormalities that are invisible in conventional imaging. In healthcare, hyperspectral systems are deployed for monitoring diabetic foot ulcers and burns. In 2024, hyperspectral devices were utilized in over 1,500 research facilities globally. The defense sector is also adopting it for surveillance and target recognition. Its non-contact, label-free approach enhances safety in pharmaceutical inspection and quality assurance across various manufacturing processes.

Near-Infrared Spectroscopy (NIRS): NIRS is gaining momentum in brain imaging, neonatal care, and functional monitoring due to its ability to measure oxygenation and blood flow non-invasively. In 2024, over 8,000 NIRS systems were installed in neuro-research labs and neonatal ICUs worldwide. Its application in mental health, cognitive neuroscience, and rehabilitation is expanding. Portable NIRS devices are used in ambulances and remote health centers. Clinical trials are leveraging NIRS to study drug responses and patient biometrics. Its low cost, ease of use, and safety make it suitable for both research and point-of-care. The integration of wearable NIRS sensors is also driving interest in sports science.

Confocal Microscopy: Confocal microscopy offers high-resolution, 3D imaging of biological tissues and is heavily utilized in dermatology, oncology, and neurology. It enables live-cell imaging, making it essential in real-time cellular studies. In 2024, confocal systems were used in more than 20,000 publications related to cellular and molecular imaging. Its use is also prominent in cosmetic dermatology for skin analysis. Confocal microscopy’s precise optical sectioning helps visualize specific cell layers without the need for physical slicing. It is increasingly adopted in pharmaceutical labs for drug mechanism studies. Innovations in spinning-disk and laser scanning systems have enhanced acquisition speed and resolution significantly.

Medical Diagnostics: Medical diagnostics represent the largest application segment in the optical imaging market. Technologies like OCT, fluorescence imaging, and NIRS are vital in detecting diseases such as cancer, glaucoma, cardiovascular blockages, and neurological disorders. In 2024, over 60% of hospitals used at least one optical imaging tool for diagnostic purposes. The demand for early-stage, radiation-free diagnosis is fueling growth. Real-time imaging helps clinicians make quicker, more accurate decisions. AI-enhanced tools are streamlining the workflow and boosting accuracy. Optical imaging is also used in prenatal and fetal monitoring. This segment continues to evolve with new diagnostic biomarkers and portable system developments.

Life Sciences Research: Optical imaging is a cornerstone in life sciences research, offering precise visualization of biological samples at cellular and sub-cellular levels. Researchers use confocal and fluorescence microscopy for gene expression analysis, protein localization, and cell tracking. In 2024, over 70,000 research papers included optical imaging in methodology sections. Hyperspectral imaging is gaining traction for metabolic and phenotypic studies. Optical imaging is also used in stem cell research, neurobiology, and immunology. Advanced 3D imaging techniques support tissue regeneration and organoid research. With growing investments in academic and clinical labs, this segment is expected to maintain strong momentum.

Pharmaceutical Development: In pharmaceutical development, optical imaging accelerates drug discovery and therapeutic monitoring. It allows in vivo tracking of drug delivery and efficacy in preclinical studies. In 2024, over 500 pharma R&D centers integrated optical imaging systems. Fluorescence imaging and NIRS are key to understanding pharmacokinetics and pharmacodynamics. Imaging biomarkers help determine drug targeting and response mechanisms. Optical imaging enables faster screening of compound libraries and supports personalized medicine development. Real-time visualization of disease progression and treatment response enhances the translational potential of new drugs. Regulatory authorities are also supporting non-invasive imaging for preclinical safety assessments.

Industrial Inspection: Optical imaging is increasingly used in industrial inspection for defect detection, quality control, and materials analysis. Hyperspectral and confocal imaging systems help inspect electronics, semiconductors, and plastics with micron-level accuracy. In 2024, over 12,000 industrial facilities integrated optical imaging tools in their inspection lines. These tools can detect contamination, microfractures, and material inconsistencies. Non-contact, non-destructive evaluation ensures high productivity and minimal waste. Optical imaging also supports automation in manufacturing by enabling real-time process monitoring. In the automotive and aerospace sectors, it is used for coating analysis, thermal inspection, and surface integrity verification.

Agriculture & Food Testing: In agriculture and food testing, optical imaging ensures quality, safety, and yield optimization. Hyperspectral imaging detects ripeness, contamination, and nutrient levels in crops. In 2024, optical imaging was deployed in over 4,000 agro-tech facilities worldwide. Near-infrared spectroscopy helps monitor moisture and fat content in food products. Imaging systems are used in sorting lines to remove defective produce and foreign objects. In precision agriculture, drones equipped with imaging tools map fields and assess crop health. Confocal and fluorescence imaging are also used in plant research to study disease resistance and growth patterns. This application supports sustainable farming and food traceability.

Hospitals and Clinics: Hospitals and clinics are the primary adopters of optical imaging technologies, particularly for diagnostic imaging. OCT and NIRS are commonly used in ophthalmology, cardiology, and neurology departments. In 2024, over 70% of tertiary hospitals globally had installed at least one form of optical imaging system. The growing burden of chronic diseases has prompted early screening programs using non-invasive tools. Real-time surgical imaging and intraoperative guidance are supported by fluorescence imaging systems. Increasing patient preference for non-radiation diagnostic procedures is driving system upgrades across hospital networks. The integration with AI-based software further enhances workflow efficiency and diagnostic accuracy.

Research & Academic Institutes: Research and academic institutes use optical imaging for cellular, molecular, and preclinical studies. Confocal microscopy and hyperspectral imaging are core tools in experimental biology, pharmacology, and bioengineering. In 2024, over 30,000 institutions worldwide had dedicated optical imaging labs. Grants and collaborations with industry players help institutions access advanced imaging platforms. These tools support peer-reviewed publications, patents, and translational research initiatives. Optical imaging is also a critical training component in medical and life sciences curricula. Institutes are increasingly adopting AI-enhanced systems for real-time data interpretation. This segment continues to drive innovation and foundational discoveries across disciplines.

Pharmaceutical & Biotechnology Companies: Pharmaceutical and biotech companies rely on optical imaging for drug discovery, biomarker validation, and therapeutic monitoring. In 2024, more than 1,000 companies deployed advanced imaging platforms in preclinical R&D. Fluorescence and hyperspectral imaging are essential for target identification, screening, and drug interaction studies. NIRS is widely used in real-time physiological monitoring during clinical trials. Imaging data helps reduce time-to-market and ensures regulatory compliance. AI-enabled imaging platforms further automate data processing, enabling faster decision-making. The emphasis on precision medicine and biologics is increasing the role of optical imaging in personalized therapy development and delivery.

Diagnostic Imaging Centers: Diagnostic imaging centers are rapidly adopting optical imaging to expand service offerings and improve diagnosis quality. In 2024, over 15,000 standalone diagnostic centers globally used optical imaging tools. These systems enable detailed tissue imaging with minimal patient discomfort. OCT and fluorescence imaging are used in eye care and oncology screening. Compact, cost-effective devices are ideal for high-throughput patient environments. Optical imaging also enhances virtual diagnostics and tele-imaging capabilities. As these centers compete on turnaround time and accuracy, advanced imaging systems become essential for maintaining service quality and attracting patients seeking high-precision evaluations.

Agricultural Enterprises: Agricultural enterprises are investing in optical imaging to enhance crop health monitoring, food safety, and productivity. Hyperspectral imaging is used for pest detection, soil mapping, and disease analysis. In 2024, more than 2,500 agricultural firms integrated imaging into their precision farming operations. These systems reduce the need for manual inspections and promote efficient resource use. In food processing units, near-infrared spectroscopy helps ensure product consistency and contaminant detection. AI-powered imaging tools analyze yield predictions and climate impact on crop cycles. This adoption supports sustainability and regulatory compliance, especially in export-driven agricultural economies.

North America accounted for the largest market share at 38.6% in 2024, however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 12.1% between 2025 and 2032.

North America's dominance stems from widespread adoption of OCT, fluorescence imaging, and NIRS in clinical diagnostics, especially in the U.S. and Canada. In 2024, over 65% of U.S. hospitals were equipped with optical imaging systems. Europe followed with a 27.8% market share in 2024, driven by research funding and technological advancement in countries like Germany and the UK. Asia-Pacific's rapid growth is attributed to expanding healthcare infrastructure, growing research initiatives, and increased demand for non-invasive diagnostics across China, India, and Japan. The Middle East & Africa region captured a smaller share of 7.3% in 2024 but is gradually witnessing adoption, supported by digital healthcare initiatives and increasing investment in diagnostic imaging technologies. Each region is expected to contribute significantly to market expansion over the forecast period.

Strong Demand from Healthcare Sector Accelerates North America’s Optical Imaging Growth

The North America optical imaging market is being driven by high demand for non-invasive diagnostics, particularly in ophthalmology, cardiology, and oncology. In 2024, over 45% of all optical coherence tomography (OCT) procedures globally were performed in the United States. More than 70% of hospitals across North America are equipped with some form of optical imaging device. The U.S. FDA has approved over 20 fluorescence imaging agents for clinical use. Confocal microscopy and near-infrared spectroscopy (NIRS) are widely utilized in research institutions and diagnostics centers. Moreover, strong government support for medical research, presence of key market players, and increasing adoption of point-of-care imaging systems are accelerating innovation and regional penetration. Canada is also witnessing increased investment in imaging centers, with over 600 facilities utilizing optical platforms by the end of 2024.

Growing R&D and Medical Innovations Fuel Optical Imaging Adoption in Europe

Europe is a strong contender in the global optical imaging market, with countries like Germany, the UK, and France leading advancements in imaging research. In 2024, the region held a 27.8% share of the global market. Over 40% of European research institutions use confocal and hyperspectral imaging for life sciences applications. Germany alone accounted for nearly 6,000 installed optical imaging systems in clinical and research settings. The UK’s National Health Service (NHS) has integrated fluorescence-guided imaging in over 50 surgical hospitals. Significant funding from Horizon Europe and national healthcare programs supports technology upgrades and innovation in diagnostics. The presence of imaging-focused biotech clusters and collaborations between universities and commercial players continues to boost Europe’s technological position in the market.

Rising Healthcare Investments and Research Boost Asia-Pacific Market Expansion

Asia-Pacific is witnessing the fastest growth in the optical imaging market due to a surge in healthcare infrastructure, population health awareness, and government-backed diagnostic programs. In 2024, the region accounted for 21.6% of the global market share. China and India are leading with over 8,000 hospitals adopting optical imaging systems. Japan has integrated optical imaging into more than 60% of its tertiary care institutions. Research institutions across South Korea, Singapore, and Australia are actively using hyperspectral and fluorescence systems for advanced cellular studies. Additionally, favorable regulatory policies and increasing partnerships between local and global manufacturers are accelerating adoption. The demand for portable and affordable optical imaging systems is high in rural and semi-urban areas, driving product innovations tailored to regional needs.

Gradual Technology Integration and Healthcare Modernization in MEA Region

The Middle East & Africa (MEA) region is gradually incorporating optical imaging technologies across its medical and industrial sectors. In 2024, MEA contributed approximately 7.3% to the global market. Countries such as the UAE and Saudi Arabia are leading the charge, with over 500 hospitals adopting OCT and NIRS systems. Several diagnostic centers in the UAE have integrated fluorescence imaging for oncology and vascular assessments. South Africa has shown strong growth in academic research, with leading universities employing confocal microscopy for life sciences. Government initiatives such as Saudi Vision 2030 and rising investments in medical infrastructure are helping the region upgrade its imaging capabilities. Although limited by affordability in rural regions, the introduction of portable and cost-effective systems is improving access to high-quality diagnostics.

The global optical imaging market is highly competitive, with several key players focusing on innovation, product expansion, and strategic collaborations to strengthen their market positions. Major players are investing heavily in R&D to enhance imaging resolution, reduce device size, and enable AI integration. In 2024, over 60% of newly launched devices incorporated AI-driven diagnostics or cloud-enabled platforms. Mergers and acquisitions have also intensified; notable deals included technology firms acquiring niche imaging startups for access to proprietary imaging algorithms. Companies are also expanding geographically, with many U.S. and European manufacturers establishing operations in Asia-Pacific to meet growing demand. Additionally, partnerships between academic institutions and commercial players are driving innovation in imaging biomarkers and therapeutic monitoring. Competition is especially fierce in the OCT and fluorescence imaging segments, which together account for over 55% of total product revenues. Manufacturers are prioritizing FDA and CE approvals to accelerate commercialization cycles and product uptake.

Carl Zeiss Meditec AG

PerkinElmer Inc.

Canon Inc.

Leica Microsystems (Danaher Corporation)

Headwall Photonics Inc.

Topcon Corporation

Bruker Corporation

Hamamatsu Photonics K.K.

Optovue Inc.

Heidelberg Engineering GmbH

Wasatch Photonics Inc.

Cytoviva Inc.

Nidek Co., Ltd.

Thermo Fisher Scientific Inc.

Imalux Corporation

The optical imaging market is undergoing rapid technological evolution driven by advancements in hardware, software, and artificial intelligence. Optical Coherence Tomography (OCT) continues to dominate due to its non-invasive, real-time imaging capabilities. As of 2024, over 75% of ophthalmology clinics globally use advanced OCT systems for retinal diagnostics. Enhanced spectral-domain and swept-source OCT platforms now offer higher resolution and faster scan times. Meanwhile, Fluorescence Imaging is becoming more sophisticated with the integration of quantum dots and novel fluorophores, enabling deeper tissue visualization and real-time intraoperative imaging.

Near-Infrared Spectroscopy (NIRS) is advancing with portable and wearable designs, widely used for monitoring cerebral oxygenation in neonatal and surgical settings. In 2024, over 3,000 hospitals globally adopted compact NIRS devices. Hyperspectral Imaging is gaining ground in cancer diagnostics, with AI-enhanced analysis helping detect metabolic shifts in tissues at the molecular level. In industrial sectors, hyperspectral cameras are used for automated food quality inspection and material sorting.

Confocal Microscopy continues to evolve with live-cell imaging and 3D reconstruction capabilities. Integrated platforms now combine confocal and multiphoton microscopy, offering subcellular detail for research labs. The synergy of AI and cloud computing is accelerating image interpretation, reducing human error, and enabling predictive diagnostics across healthcare and life sciences domains.

• In October 2023, Canon Medical Systems introduced the OCT-A1 system featuring real-time angiography imaging for improved visualization of retinal vessels without dye injection, expanding the scope of non-invasive diagnostics.

• In January 2024, Bruker launched the Ultima Investigator Multiphoton Microscope with advanced resonance scanning capabilities, enhancing deep tissue imaging for neuroscience and cancer biology applications.

• In February 2024, Headwall Photonics announced a partnership with NASA to deploy hyperspectral imaging sensors for space-based agricultural monitoring, showcasing the technology’s versatility beyond healthcare.

• In March 2024, Leica Microsystems unveiled the STELLARIS 8 DIVE system, offering real-time fluorescence lifetime imaging microscopy (FLIM) combined with confocal and multiphoton capabilities for live-cell and tissue imaging.

• In June 2024, Thermo Fisher Scientific integrated deep learning algorithms into its Invitrogen EVOS imaging platform, enabling automated classification of cell types and phenotypes in high-throughput research environments.

The Optical Imaging Market Report covers a comprehensive analysis of industry dynamics, technology landscapes, competitive scenarios, and regional outlooks from 2024 to 2032. The study provides in-depth segmentation by imaging type, application area, and end-user category, delivering insights into growth potential across various verticals including healthcare, life sciences, pharmaceuticals, and agriculture. It includes quantitative evaluations of demand trends for Optical Coherence Tomography (OCT), Near-Infrared Spectroscopy (NIRS), Hyperspectral Imaging, Fluorescence Imaging, and Confocal Microscopy.

This report examines the usage of optical imaging in diagnostics, therapeutic monitoring, surgical guidance, industrial inspection, and agricultural quality control. It assesses market penetration across hospitals, research institutes, pharmaceutical companies, and imaging centers, highlighting investment patterns, technology adoption rates, and infrastructure development. The study also evaluates recent innovations in AI integration, sensor technology, and cloud-based imaging analysis.

Furthermore, the report addresses the strategic initiatives of leading players, product pipelines, collaborations, and global expansion strategies. It highlights key drivers such as rising demand for non-invasive diagnostics, increasing prevalence of chronic diseases, and technological advancements. Challenges including cost barriers and regulatory complexities are also analyzed. The Optical Imaging Market Report serves as a critical resource for stakeholders to navigate emerging opportunities and mitigate investment risks.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 1,767.2 Million |

|

Market Revenue in 2032 |

USD 3,547.18 Million |

|

CAGR (2025 - 2032) |

9.1% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Type:

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Carl Zeiss Meditec AG, PerkinElmer Inc., Canon Inc., Leica Microsystems (Danaher Corporation), Headwall Photonics Inc., Topcon Corporation, Bruker Corporation, Hamamatsu Photonics K.K., Optovue Inc., Heidelberg Engineering GmbH, Wasatch Photonics Inc., Cytoviva Inc., Nidek Co., Ltd., Thermo Fisher Scientific Inc., Imalux Corporation |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |