Reports

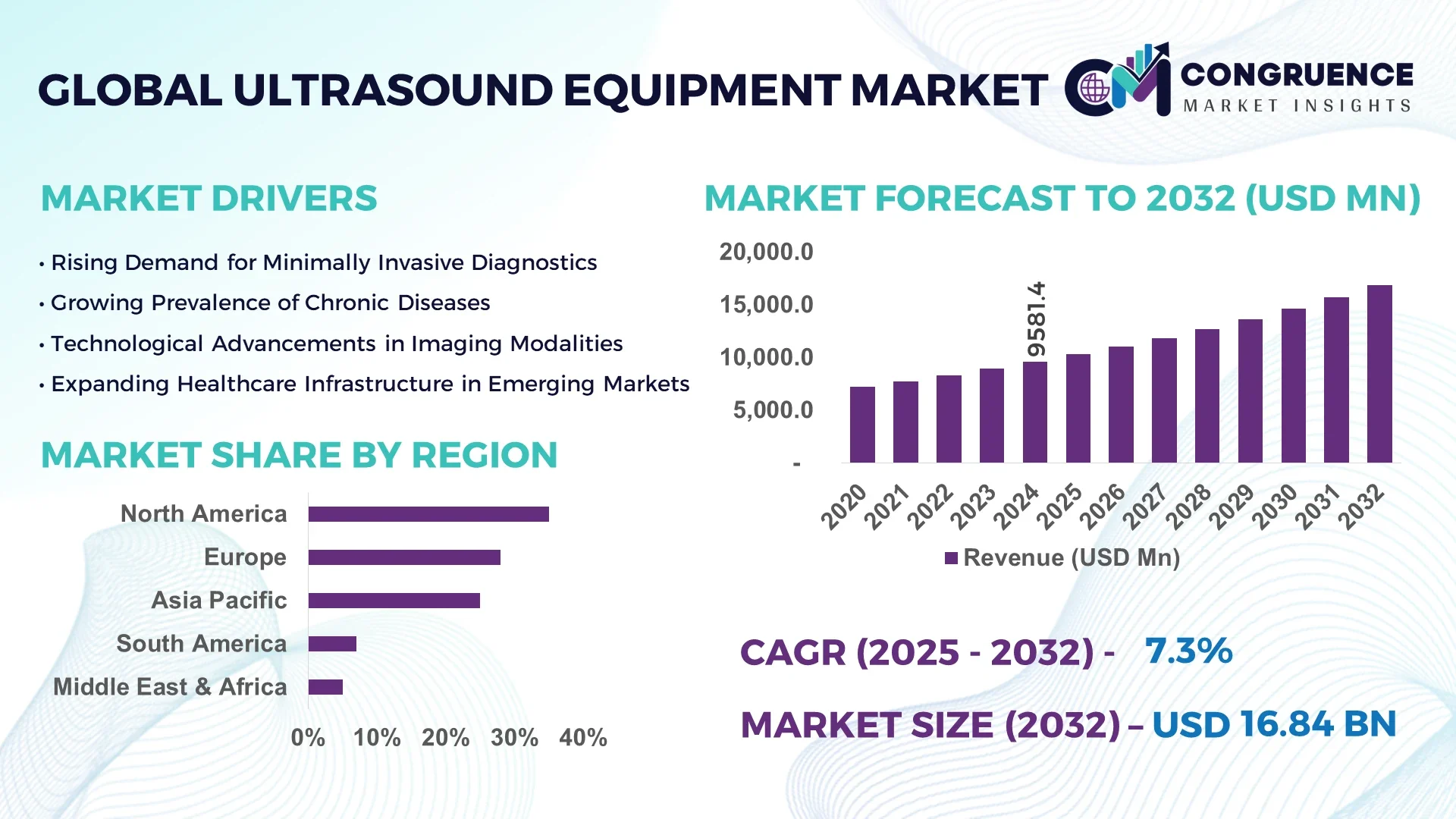

The Global Ultrasound Equipment Market was valued at USD 9,581.4 Million in 2024 and is anticipated to reach a value of USD 16,835.5 Million by 2032, expanding at a CAGR of 7.3% between 2025 and 2032.

The ultrasound equipment market is witnessing significant growth due to the increasing demand for non-invasive diagnostic procedures and the rising prevalence of chronic diseases.Technological advancements, such as the development of portable and handheld ultrasound devices, are enhancing point-of-care diagnostics, making ultrasound more accessible in various healthcare settings.Additionally, the integration of artificial intelligence (AI) in ultrasound imaging is improving diagnostic accuracy and workflow efficiency, further propelling market growth.The growing geriatric population and the increasing focus on early disease detection are also contributing to the expansion of the ultrasound equipment market globally.

Artificial intelligence is revolutionizing the ultrasound equipment market by enhancing image quality, improving diagnostic accuracy, and streamlining workflows.AI algorithms assist in real-time image analysis, enabling quicker and more accurate diagnoses.For instance, AI-powered ultrasound systems can automatically identify anatomical structures and detect abnormalities, reducing the dependency on operator expertise.This is particularly beneficial in regions with a shortage of skilled sonographers.Moreover, AI integration facilitates the development of portable ultrasound devices with advanced capabilities, expanding their use in point-of-care settings.The adoption of AI in ultrasound imaging is also driving the development of tele-ultrasound services, allowing remote consultations and diagnostics, which is crucial in rural and underserved areas.Overall, AI is significantly enhancing the capabilities of ultrasound equipment, making it more efficient, accurate, and accessible.

In July 2024, GE HealthCare launched the Versana Balance, an AI-enabled ultrasound product designed to provide precise diagnostics for obstetrics and gynecology applications.

The global Ultrasound Equipment Market is experiencing rapid expansion due to the growing preference for non-invasive diagnostic solutions. Healthcare providers are increasingly adopting ultrasound devices for real-time, radiation-free imaging, especially in prenatal care, cardiology, and internal medicine. The World Health Organization (WHO) highlights that over 70% of medical decisions involve some form of diagnostic imaging. Ultrasound technology, being safer and more cost-effective than CT or MRI, is becoming a staple in both developed and emerging healthcare settings. The global shift towards early disease detection and preventive care also supports the rising installation of portable and point-of-care ultrasound systems across clinics and rural health centers.

A significant barrier in the Ultrasound Equipment Market is the shortage of trained sonographers and radiologists, particularly in low and middle-income countries. The operation of advanced ultrasound machines requires specific training, and the learning curve is relatively steep, especially with the introduction of AI-powered systems. According to the American Registry for Diagnostic Medical Sonography, there are fewer than 100,000 certified professionals in the U.S., resulting in staffing gaps. Furthermore, training programs can be costly and time-consuming, discouraging healthcare facilities from adopting newer, more complex ultrasound technologies, despite their clinical benefits.

One of the most lucrative opportunities in the Ultrasound Equipment Market is the surge in demand for portable and handheld devices. These compact systems are revolutionizing point-of-care diagnostics by enabling imaging outside of traditional hospital settings—in ambulances, rural clinics, and even home care. Companies like Butterfly Network and Clarius have launched pocket-sized ultrasound scanners that connect to smartphones, increasing access to diagnostics in remote regions. With over 60% of the global population living in areas with limited access to full-scale medical imaging centers, portable devices present a scalable, cost-effective solution to bridge the diagnostic gap.

While AI is enhancing diagnostic accuracy in the Ultrasound Equipment Market, its integration with traditional systems poses significant technical challenges. Ensuring data interoperability across platforms, maintaining regulatory compliance, and managing cybersecurity risks are critical issues faced by manufacturers and healthcare providers. Hospitals using legacy systems often struggle to integrate AI tools into their workflows, leading to inefficiencies. A 2023 survey by Frost & Sullivan revealed that 42% of radiology departments cited system compatibility as the top hurdle to adopting AI-powered ultrasound devices. As a result, bridging the technology gap remains a major challenge for unlocking the full potential of AI in diagnostic imaging.

The ultrasound equipment market is experiencing significant transformations driven by technological advancements and evolving healthcare needs.A notable trend is the increasing adoption of handheld ultrasound devices, which are projected to capture over 50% of the portable ultrasound segment due to their affordability and ease of use . These devices are particularly beneficial in point-of-care settings, enabling quick diagnostics in emergency rooms and remote locations.

Artificial intelligence (AI) integration is another pivotal trend, anticipated to impact over 70% of new product innovations . AI enhances diagnostic accuracy by providing automated image interpretation, thereby reducing the reliance on operator expertise and improving workflow efficiency.This is especially crucial in areas with a shortage of skilled sonographers.

Tele-ultrasound services are also gaining traction, with adoption rates growing by more than 60% . These services enable remote imaging and consultations, expanding access to quality healthcare in underserved regions.Additionally, the demand for contrast-enhanced ultrasound (CEUS) has surged beyond 40%, offering enhanced real-time imaging for accurate diagnosis.

Regionally, North America holds over 35% of the market share, driven by technological innovations and high healthcare expenditure . However, the Asia-Pacific region is experiencing the highest growth, with expansion rates exceeding 50%, attributed to increasing healthcare investments and rapid technological advancements . Europe follows, contributing over 25% of the market, propelled by advancements in 3D/4D imaging technology.

The ultrasound equipment market is segmented by type, application, and end-user, each playing a crucial role in the market's dynamics.

Compact Ultrasound Devices

Compact ultrasound devices are gaining popularity due to their portability, affordability, and flexibility.These systems are essential for point-of-care imaging and diagnostics in various settings, including clinics, hospitals, and emergency rooms.Their battery-operated mode and lightweight design make them ideal for use in remote locations and situations requiring immediate on-site diagnosis.

Table-top Ultrasound Equipment

Table-top ultrasound equipment is experiencing growth, particularly with high-end technology models.These systems offer high-frequency transducers and AI-enabled imaging capabilities, enhancing picture quality and diagnostic precision.They are increasingly used in specialized medical fields such as radiology, obstetrics, and cardiology for complex procedures and high-end imaging.

Radiology

Radiology remains a dominant application area for ultrasound equipment, with the segment holding the largest revenue share of over 22.33% in 2023 . The integration of AI in radiology enhances diagnostic accuracy and efficiency, making ultrasound an indispensable tool for imaging organs and tissues across various medical conditions.

Gynecology

The gynecology segment is anticipated to grow at the fastest rate, driven by increased awareness of maternal and fetal health.Ultrasound devices are extensively used for prenatal screenings, monitoring fetal development, and diagnosing gynecological conditions such as ovarian cysts and uterine fibroids.

Cardiology

In cardiology, ultrasound equipment is vital for assessing heart function and detecting cardiovascular conditions.Echocardiography, a key application, allows for real-time visualization of heart structures and blood flow, aiding in the diagnosis of heart failure, valve disorders, and congenital heart defects.

Point of Care

Point-of-care ultrasound is increasingly important, enabling quick assessments in emergency settings or at the patient’s bedside.The portability and ease of use of compact ultrasound devices make them ideal for immediate diagnostics in critical care situations.

Urology

In urology, ultrasound assists in visualizing the kidneys, bladder, and prostate, aiding in the diagnosis of conditions such as kidney stones, prostate enlargement, and urinary tract infections.Its non-invasive nature makes it a preferred diagnostic tool in urological assessments.

Surgery

Ultrasound equipment is increasingly utilized in surgical procedures to guide minimally invasive operations and ensure precision.Its real-time imaging capabilities assist surgeons in navigating complex anatomical structures during interventions.

Hospitals

Hospitals are the primary end-users of ultrasound equipment, accounting for the largest revenue share of over 40.45% in 2023 . The extensive use of ultrasound devices across various departments, including emergency rooms, outpatient clinics, and specialized diagnostic centers, drives this segment.The adoption of technologically advanced imaging systems and the increasing number of patients with lifestyle-related disorders further boost demand.

Clinics

Clinics also represent a significant end-user segment, relying on ultrasound equipment for routine diagnostic purposes.The growing availability of portable and affordable ultrasound devices enhances their adoption in clinics, enabling efficient patient assessments and monitoring .

North America accounted for the largest market share at 35% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.5% between 2025 and 2032.

North America's dominance is attributed to its advanced healthcare infrastructure, high adoption of innovative technologies, and significant investments in research and development.Conversely, Asia-Pacific's rapid growth is driven by increasing healthcare expenditures, rising awareness of early disease detection, and government initiatives to improve healthcare accessibility.Europe holds a substantial market share, supported by its well-established healthcare systems and continuous technological advancements.The Middle East & Africa region, while currently holding a smaller share, is witnessing steady growth due to improving healthcare facilities and increasing demand for diagnostic imaging.

Technological Advancements Driving Market Growth

In 2024, North America maintained its leading position in the ultrasound equipment market, accounting for 35% of the global share.The region's growth is propelled by the integration of advanced technologies such as AI and 3D/4D imaging in ultrasound devices.The United States, in particular, has seen a surge in the adoption of portable and handheld ultrasound devices, enhancing point-of-care diagnostics.The presence of major market players and continuous investment in research and development contribute to the region's market expansion.Additionally, the increasing prevalence of chronic diseases and the aging population are driving the demand for efficient diagnostic tools.

Rising Demand for Non-Invasive Diagnostic Tools

Europe's ultrasound equipment market was valued at USD 2.66 billion in 2024.The region's market growth is fueled by the rising demand for non-invasive diagnostic tools and the increasing incidence of chronic diseases.Germany leads the European market, driven by its robust healthcare infrastructure and high adoption rates of advanced medical technologies.The emphasis on early disease detection and preventive healthcare measures further boosts the demand for ultrasound equipment.Moreover, the region's focus on technological innovation and the presence of key market players contribute to the market's expansion.

Rapid Growth Driven by Healthcare Investments

Asia-Pacific is emerging as the fastest-growing region in the ultrasound equipment market, with a projected CAGR of 6.5% from 2025 to 2032.The region's market size was USD 2,280.5 million in 2024.China, Japan, and India are the key contributors to this growth, driven by increasing healthcare investments, rising awareness of early disease detection, and government initiatives to improve healthcare accessibility.The adoption of portable and handheld ultrasound devices is gaining traction, particularly in rural and remote areas.Additionally, the growing prevalence of chronic diseases and the aging population are boosting the demand for efficient diagnostic tools.

Steady Growth Amidst Healthcare Improvements

The Middle East & Africa ultrasound equipment market was valued at USD 198.3 million in 2024.The region is witnessing steady growth, driven by improving healthcare infrastructure, increasing demand for diagnostic imaging, and rising awareness of early disease detection.Countries like Saudi Arabia, the United Arab Emirates, and South Africa are leading the market, supported by government initiatives to enhance healthcare services.The adoption of advanced technologies such as 3D/4D imaging and portable ultrasound devices is gaining momentum.Additionally, the growing prevalence of chronic diseases and the aging population are contributing to the market's expansion.

The global ultrasound equipment market is characterized by intense competition among key players striving for technological innovation and market expansion.Leading companies such as GE Healthcare, Siemens Healthineers, and Philips Healthcare dominate the market with their extensive product portfolios and strong global presence.These companies continuously invest in research and development to introduce advanced ultrasound systems with enhanced imaging capabilities and user-friendly interfaces.Emerging players like Mindray and Clarius Mobile Health are gaining traction by offering cost-effective and portable ultrasound solutions, catering to the growing demand in developing regions.The market also witnesses strategic collaborations and partnerships aimed at expanding distribution networks and enhancing product offerings.For instance, in August 2023, GE Healthcare launched the Vscan Air SL, a wireless ultrasound imaging system designed for quick assessments, reflecting the trend towards portable and point-of-care ultrasound devices.Additionally, the integration of artificial intelligence in ultrasound equipment is becoming a key differentiator, enabling automated image analysis and improved diagnostic accuracy.Despite the opportunities, companies face challenges such as stringent regulatory requirements and the need for continuous innovation to maintain a competitive edge in this dynamic market landscape.

GE Healthcare

Siemens Healthineers

Philips Healthcare

Mindray Medical International Limited

Canon Medical Systems Corporation

Samsung Medison

Fujifilm Holdings Corporation

Esaote S.p.A.

Clarius Mobile Health

Hitachi, Ltd.

Technological advancements are significantly shaping the ultrasound equipment market, with innovations enhancing diagnostic capabilities and expanding application areas.The integration of artificial intelligence (AI) in ultrasound systems has revolutionized image acquisition and interpretation, enabling automated measurements and improved diagnostic accuracy.For example, AI-powered tools assist clinicians in detecting anomalies and reducing examination times, thereby increasing efficiency in clinical settings.The development of portable and handheld ultrasound devices has facilitated point-of-care diagnostics, especially in remote and underserved regions.These compact devices offer real-time imaging and are increasingly used in emergency medicine, critical care, and primary care settings.Additionally, the incorporation of 3D and 4D imaging technologies provides detailed visualization of anatomical structures, enhancing prenatal and cardiac assessments.Wireless connectivity and cloud-based data storage solutions are also gaining prominence, allowing seamless integration with hospital information systems and enabling telemedicine applications.Furthermore, advancements in transducer technology have led to the development of high-frequency probes, improving image resolution and expanding the scope of ultrasound in musculoskeletal and vascular imaging.These technological innovations are driving the adoption of ultrasound equipment across various medical specialties, contributing to the market's growth.

In August 2023, GE Healthcare introduced the Vscan Air SL, a wireless ultrasound imaging system designed for rapid cardiac and vascular assessments at the point of care.

In January 2024, Clarius Mobile Health launched the Clarius PAL HD3, a wireless portable whole-body ultrasound scanner in Australia, offering high-definition imaging compatible with iOS and Android devices.

In September 2023, Exo unveiled the AI-powered Iris System, featuring a portable probe with a 150-degree field of view and a depth of 30 centimeters, enhancing liver and fetal imaging capabilities.

In July 2024, a pilot project in Uganda implemented AI-based ScanNav FetalCheck technology, enabling midwives and nurses to perform prenatal scans using portable devices, aiming to reduce stillbirths and complications in rural areas.

In July 2024, GE HealthCare adjusted its revenue growth forecast due to a slowdown in China's healthcare sector, impacted by an anti-corruption campaign affecting sales of imaging machines and other medical equipment.

The Ultrasound Equipment Market Report provides a comprehensive analysis of the global market, encompassing various segments based on type, application, end-user, and geography.It offers insights into market dynamics, including drivers, restraints, opportunities, and challenges influencing market growth.The report examines technological advancements, such as the integration of AI and the development of portable devices, shaping the future of ultrasound diagnostics.It also highlights recent developments and strategic initiatives undertaken by key market players to enhance their market presence.The geographical analysis covers major regions, including North America, Europe, Asia-Pacific, and the Middle East & Africa, providing a detailed understanding of regional market trends and growth prospects.Furthermore, the report includes a competitive landscape section, profiling leading companies and analyzing their product offerings, strategic partnerships, and market strategies.This comprehensive report serves as a valuable resource for stakeholders, including manufacturers, healthcare providers, investors, and policymakers, facilitating informed decision-making and strategic planning in the ultrasound equipment market.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 9,581.4 Million |

|

Market Revenue in 2032 |

USD 16,835.5 Million |

|

CAGR (2025 - 2032) |

7.3% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

GE Healthcare, Siemens Healthineers, Philips Healthcare, Mindray Medical International Limited, Canon Medical Systems Corporation, Samsung Medison, Fujifilm Holdings Corporation, Esaote S.p.A., Clarius Mobile Health |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |