Reports

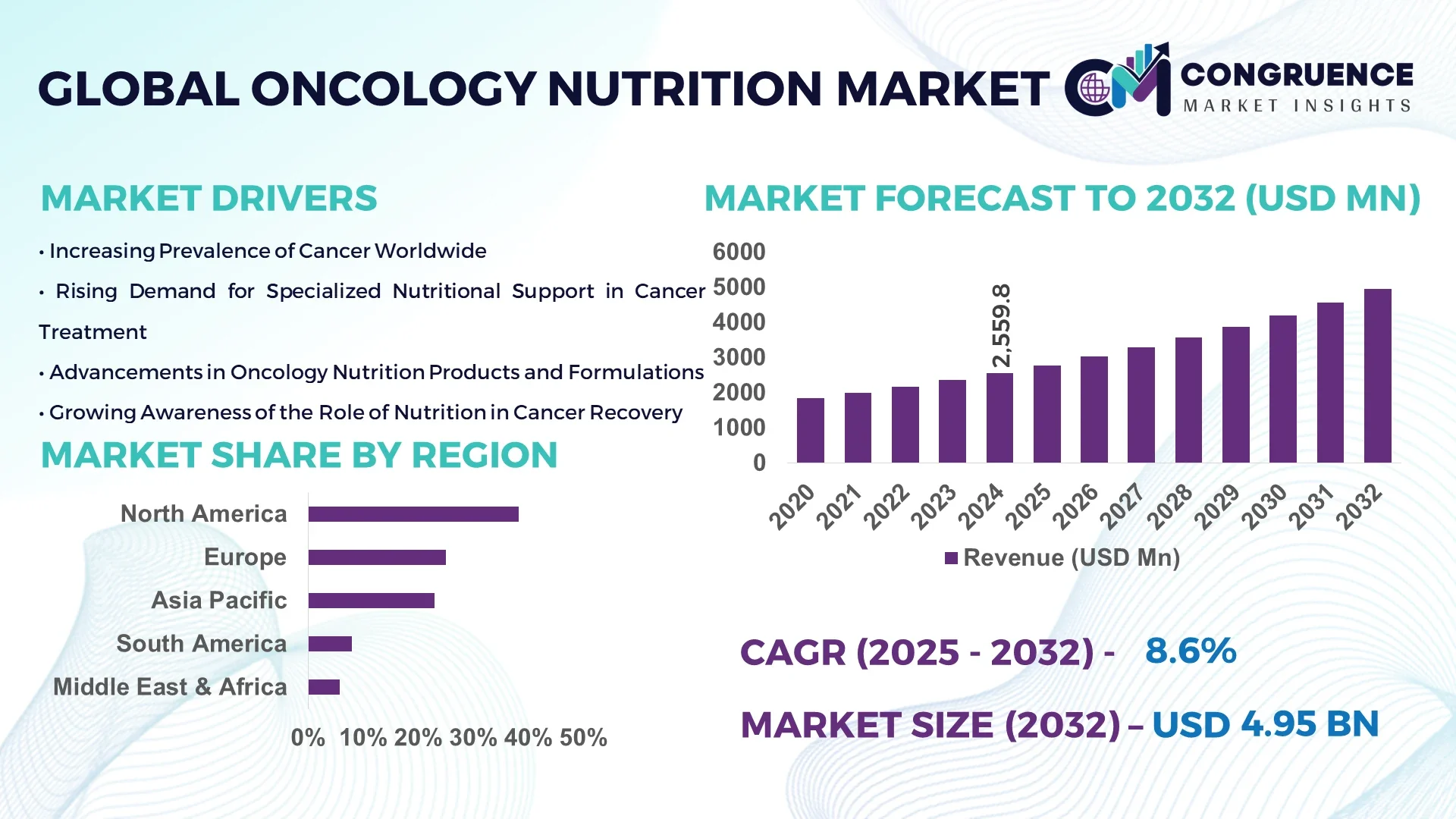

The Global Oncology Nutrition Market was valued at USD 2559.81 Million in 2024 and is anticipated to reach a value of USD 4952.75 Million by 2032, expanding at a CAGR of 8.6% between 2025 and 2032.

The oncology nutrition market is witnessing a sharp increase in demand due to the surging global cancer burden and the growing emphasis on improving cancer patient care through nutritional therapy. Cancer patients undergoing chemotherapy, radiotherapy, or surgery face significant nutritional challenges, which makes oncology-specific nutrition crucial for recovery and treatment outcomes. Specialized formulas tailored for various cancer types, such as gastrointestinal, liver, breast, and lung cancers, are gaining traction. Furthermore, oncology nutrition is increasingly recognized as a complementary treatment approach, helping reduce treatment-related complications and enhancing quality of life. The integration of clinical nutrition into oncology care frameworks across hospitals and clinics is fueling market growth, with a rise in institutional collaborations, clinical trials, and product innovations aimed at optimizing patient health and survival rates.

Artificial Intelligence (AI) is playing a pivotal role in reshaping the oncology nutrition market by enabling precision nutrition solutions tailored to individual patient needs. AI-powered tools and platforms analyze large datasets, including genetic profiles, treatment regimens, metabolic rates, and dietary habits, to formulate customized nutritional strategies that support cancer treatment. Hospitals and research centers are leveraging machine learning algorithms to predict patient responses to certain nutrients and micronutrients, minimizing malnutrition risks. AI assists dietitians and oncologists in identifying optimal feeding plans, ensuring patients receive the correct macro and micronutrient balance throughout treatment cycles. Furthermore, AI-driven mobile apps and wearable technology are empowering remote patient monitoring, enabling real-time diet tracking, symptom logging, and adaptive meal planning. For example, tools like AI-enabled nutrition calculators and digital dietary assistants are enhancing patient adherence and engagement in nutritional programs. The market is also witnessing increased AI integration in clinical trial design and outcome tracking, streamlining product development for oncology-specific nutritional products.

"In January 2024, Nestlé Health Science collaborated with Israeli healthtech firm Nutrino to integrate AI-based nutritional analytics into cancer care pathways, enabling real-time personalization of diet plans for oncology patients through mobile apps and clinical dashboards."

The oncology nutrition market is evolving rapidly due to a complex interplay of driving forces, restraints, opportunities, and challenges. As cancer cases rise globally, the role of targeted nutritional care is gaining recognition among healthcare professionals and patients. Nutritional support has become essential to enhance treatment efficacy, reduce side effects, and improve patient resilience. Market players are developing innovative nutrition formulas and delivery systems aimed at optimizing nutrient absorption and digestion in cancer patients. Despite these promising dynamics, factors such as high costs, regulatory complexities, and patient awareness gaps continue to pose hurdles. However, technological advancements, government initiatives, and partnerships between nutrition companies and oncology centers are unlocking new avenues for expansion.

Rising Demand for Clinical Nutrition Support for Cancer Patients

The increasing incidence of cancer globally—estimated at over 20 million new cases per year—is significantly driving the demand for specialized oncology nutrition. Malnutrition affects up to 80% of cancer patients, leading to complications and higher mortality. Oncology nutrition products like enteral feeds, protein-rich supplements, and omega-3-enriched formulas are witnessing robust demand. Hospitals are integrating nutrition therapy into standard oncology protocols, and awareness campaigns by healthcare organizations are promoting nutritional interventions. The need for better clinical outcomes, shorter hospital stays, and improved tolerance to therapies has made clinical nutrition indispensable in cancer management, thus propelling the market forward.

Limited Access and High Costs of Specialized Nutritional Products

A major restraint in the oncology nutrition market is the high cost of oncology-specific nutritional formulas and supplements, which can limit accessibility, especially in developing economies. Patients in low- and middle-income countries often face difficulty affording enteral nutrition kits, infusion pumps, and high-protein supplements. Additionally, a lack of reimbursement policies in many healthcare systems further compounds the issue. Hospitals in rural and semi-urban areas may not stock advanced oncology nutrition products due to limited demand or logistical constraints. The absence of standard clinical nutrition protocols across many regions also restricts the market's penetration despite growing awareness.

Growth in Personalized Nutrition and Home-Based Care

There is a significant opportunity in personalized oncology nutrition, driven by advances in nutrigenomics, digital health, and home care trends. Increasingly, nutritionists are using genetic testing and metabolic profiling to develop customized meal plans for cancer patients. The rise in home healthcare services also enables patients to receive specialized nutrition at home through telehealth consultations and home delivery of medical nutrition products. Companies are investing in AI-powered dietary platforms that align food intake with cancer treatment schedules, reducing hospital visits. This trend is fostering patient-centric care models, boosting product sales, and opening new avenues for nutritional product innovation and delivery.

Lack of Standardized Oncology Nutrition Guidelines

One of the major challenges in the oncology nutrition market is the absence of universal clinical guidelines for nutritional management across different types and stages of cancer. Although research supports the role of nutrition in improving cancer treatment outcomes, nutrition protocols vary significantly between hospitals, regions, and oncologists. This inconsistency leads to under-prescription or delayed implementation of nutritional therapy. Moreover, oncologists often receive limited training in clinical nutrition, creating reliance on dietitians who may not be involved early in the treatment process. The gap in multidisciplinary collaboration restricts optimal patient care, thereby affecting the adoption of oncology nutrition solutions.

The oncology nutrition market is witnessing a number of significant trends that are reshaping the industry. One of the most prominent trends is the increased demand for plant-based oncology nutrition products, which are preferred for their anti-inflammatory and antioxidant properties. Manufacturers are launching organic, vegan, and allergen-free formulations to cater to this growing consumer preference. Another key trend is the integration of digital health tools, including AI, telehealth, and mobile apps, for remote nutrition monitoring and dietary adjustments. These technologies enable better compliance, real-time feedback, and personalized care. The use of high-protein, immune-boosting formulas enriched with omega-3 fatty acids, glutamine, and probiotics is becoming standard in hospital and home settings. Additionally, multi-nutrient packs for cachexia and muscle wasting in advanced cancer patients are seeing a rise in demand. Strategic collaborations between food science companies and cancer institutes are driving innovation in oncology-specific formulations, delivery methods, and packaging. The trend of early nutritional intervention during treatment planning is also gaining momentum, establishing nutrition as a core pillar of comprehensive cancer therapy.

The oncology nutrition market is segmented based on type, application, and end-user, offering a comprehensive understanding of how nutritional solutions are applied across diverse cancer care environments. By type, the market is categorized into Oral Nutrition Supplements (ONS), Enteral Nutrition, and Parenteral Nutrition, each serving different patient needs and medical conditions. In terms of application, oncology nutrition is utilized across various cancer types, including Head and Neck Cancer, Gastrointestinal Cancer, Lung Cancer, and Breast Cancer, all of which present distinct nutritional challenges. Regarding end-user insights, major demand stems from Hospitals & Clinics, where nutritional protocols are integrated into treatment pathways, and Research & Academic Institutes, which focus on product development and evidence-based clinical validation. This segmentation helps stakeholders identify niche areas of growth, target product development, and tailor distribution strategies across global markets. Each segment offers specific opportunities to improve patient outcomes, enhance treatment efficiency, and strengthen clinical outcomes through tailored nutrition interventions.

Oral Nutrition Supplements (ONS): Oral Nutrition Supplements dominate the oncology nutrition market due to their ease of use, availability, and palatability. These supplements are especially beneficial for outpatients and individuals undergoing chemotherapy or radiation who experience reduced appetite, nausea, or difficulty swallowing. ONS products are available in various flavors and nutrient profiles, enriched with protein, vitamins, and omega-3 fatty acids. According to the Global Cancer Nutrition Survey 2024, over 55% of cancer patients prefer ONS as their primary form of nutritional support. Market leaders are innovating high-protein, low-sugar formulas to meet the evolving dietary requirements. Increasing outpatient cancer treatment protocols and patient preference for non-invasive interventions are further boosting ONS adoption globally.

Enteral Nutrition: Enteral nutrition is used extensively in hospitals for cancer patients who cannot consume sufficient nutrients orally due to dysphagia, gastrointestinal surgeries, or severe mucositis. Administered via feeding tubes (nasogastric or PEG), enteral formulas are designed to deliver high-energy, protein-rich nutrients directly into the digestive tract. In 2024, enteral nutrition accounted for nearly 30% of total oncology nutrition demand due to rising surgical interventions in gastrointestinal and head & neck cancers. These formulations are often enriched with fiber, antioxidants, and immunonutrients to promote healing and reduce inflammation. Technological advancements in pump systems and customizable formulas are expanding the use of enteral nutrition in long-term cancer care.

Parenteral Nutrition: Parenteral nutrition is essential for critically ill cancer patients with non-functioning gastrointestinal systems or severe malabsorption. This type involves the intravenous delivery of essential nutrients, including amino acids, lipids, glucose, electrolytes, and trace elements. Though representing a smaller share of the market, parenteral nutrition is vital in intensive care and palliative oncology settings. The demand is particularly high in post-operative recovery and late-stage cancer management. In 2024, over 1 million oncology patients globally were estimated to require parenteral support, particularly those with pancreatic or gastric cancers. Manufacturers are developing lipid-based emulsions and glutamine-enriched solutions to enhance immunomodulatory effects and minimize infection risk.

Head and Neck Cancer: Patients with head and neck cancers often suffer from severe dysphagia, xerostomia, and mucositis, making oral intake challenging. Nutrition support is critical throughout treatment to prevent weight loss and maintain lean body mass. Over 65% of head and neck cancer patients require enteral feeding support at some stage during treatment. Tube feeding via PEG or nasogastric tubes is commonly used in conjunction with radiotherapy and chemotherapy. Nutritional intervention significantly reduces hospitalization time and enhances therapy tolerance. Specialized high-calorie, high-protein formulas are frequently used in this segment to manage the high metabolic demands of treatment and recovery.

Gastrointestinal Cancer: Gastrointestinal cancers, including colorectal, stomach, liver, and pancreatic cancers, disrupt nutrient absorption and often necessitate enteral or parenteral nutrition. In 2024, gastrointestinal cancers contributed to more than 40% of clinical nutrition interventions in oncology settings. Nutritional support during surgery, chemotherapy, or gastrointestinal resections is crucial to reduce post-operative complications. Formulas fortified with glutamine, medium-chain triglycerides (MCT), and probiotics are preferred to enhance gut health and nutrient absorption. Nutritional strategies in GI cancer management help reduce treatment-related toxicity and significantly improve patient performance status and treatment outcomes.

Lung Cancer: Lung cancer patients frequently face cachexia, loss of appetite, fatigue, and systemic inflammation, making nutrition support essential for sustaining energy levels and improving quality of life. According to the Global Lung Cancer Report 2024, up to 50% of lung cancer patients are malnourished at diagnosis, requiring nutritional intervention. Oral Nutrition Supplements (ONS) enriched with protein and omega-3 fatty acids are commonly prescribed to preserve muscle mass and immune function. Personalized nutrition plans are integrated into palliative care settings to maintain functionality and slow down muscle wasting in late-stage patients.

Breast Cancer: Although breast cancer patients typically maintain oral intake capabilities, many undergo significant metabolic changes, leading to weight gain or loss during chemotherapy. Oncology nutrition for breast cancer focuses on maintaining a balanced body composition, managing treatment-induced fatigue, and preventing malnutrition. Functional foods rich in phytoestrogens, antioxidants, and fiber are increasingly incorporated into dietary plans. Surveys indicate that nearly 45% of breast cancer patients now receive dietary counseling as part of their holistic cancer care approach. Nutritional education and meal planning interventions help reduce the risk of recurrence and improve recovery post-treatment.

Hospitals & Clinics: Hospitals and oncology clinics are the primary end-users of oncology nutrition products, representing over 65% of the total market demand in 2024. Inpatient and outpatient oncology departments frequently administer nutritional support via ONS, enteral, and parenteral methods. Clinical nutrition protocols are becoming a standard of care, particularly in tertiary cancer care centers. Oncology dietitians are integrated into multidisciplinary teams to assess nutritional status, prescribe appropriate formulas, and monitor treatment progress. Hospitals are also investing in advanced feeding equipment and customizable feeding solutions to cater to specific cancer stages and types, thereby increasing product usage across departments.

Research & Academic Institutes: Research and academic institutions play a vital role in driving innovation and clinical validation in oncology nutrition. These institutes conduct clinical trials, nutritional assessments, and patient outcome studies to evaluate the effectiveness of new formulations and delivery methods. In 2024, academic collaborations with food science and biotech firms increased by over 30%, focusing on immunonutrition and gut microbiota-modulating diets. Universities and teaching hospitals are also publishing evidence-based nutrition protocols that influence hospital guidelines globally. Research institutions serve as knowledge hubs that push the boundaries of science-backed oncology nutrition and help bring advanced therapies from lab to clinic.

North America accounted for the largest market share at 38.2% in 2024 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 10.3% between 2025 and 2032.

The dominance of North America is driven by well-established cancer treatment infrastructure, widespread clinical nutrition protocols, and high awareness among oncologists and patients. The United States leads the regional market with strong institutional support for integrating nutritional therapy into standard oncology care. Meanwhile, Asia-Pacific is witnessing rapid expansion due to rising cancer incidence, growing healthcare investments, and increasing awareness regarding oncology nutrition in countries such as China, India, and Japan. Government initiatives for cancer care nutrition programs and international collaborations for clinical trials are also boosting growth. Europe continues to maintain a robust position with increasing demand for evidence-based nutritional products, especially in Germany, France, and the U.K. The Middle East & Africa is gradually emerging with structured cancer care services, driven by GCC nations like the UAE and Saudi Arabia.

Advancements and Institutional Support Fueling Oncology Nutrition in North America

North America remains at the forefront of the oncology nutrition market, primarily due to high cancer prevalence and integration of nutrition into cancer therapy protocols. In 2024, the United States alone accounted for over 70% of North America's oncology nutrition revenue, driven by increased adoption of oral nutritional supplements and enteral nutrition products. The American Society of Clinical Oncology (ASCO) and other medical bodies have issued strong recommendations for proactive nutritional interventions in oncology, enhancing market penetration. Additionally, over 800 oncology centers across the U.S. now include registered dietitians on multidisciplinary teams. Canada is also witnessing increased investment in oncology nutrition research through provincial cancer care programs and academic partnerships, leading to demand for both clinical-grade products and research-driven solutions. The region is also characterized by widespread insurance coverage, favorable reimbursement structures, and a strong presence of key global players.

Clinical Integration and Research Collaboration Driving Growth in Europe

Europe maintains a strong position in the oncology nutrition landscape due to its established healthcare systems and emphasis on patient-centered care. In 2024, Europe held over 29.6% market share, with Germany, the U.K., and France leading demand. Hospitals in Western Europe have embraced comprehensive cancer care frameworks, where clinical nutrition is part of standard treatment regimens. Germany is a key player, with more than 400 cancer care institutions offering routine nutrition assessments during chemotherapy and radiotherapy. France and the Netherlands are advancing nutritional support in palliative care, with specialized formulations tailored to advanced cancer stages. Moreover, the EU-funded research consortiums are contributing to the development of immunonutrition and precision-based formulas for oncology patients. Eastern Europe is gradually increasing its uptake through cross-border collaborations and EU healthcare funding, although gaps still exist in standardized clinical nutrition guidelines across the region.

Rapid Urbanization and Cancer Awareness Boosting Asia-Pacific Market Expansion

Asia-Pacific is emerging as the fastest-growing oncology nutrition market, backed by rising cancer incidence, increasing urbanization, and expanding healthcare infrastructure. In 2024, Asia-Pacific represented 18.9% of the global market, with significant contributions from China, India, Japan, and South Korea. China, with over 4.8 million new cancer cases annually, is scaling up its clinical nutrition services, supported by national policies and public health campaigns. India has launched nutrition-centric oncology support programs across major cancer hospitals, especially for underprivileged patients. Japan continues to lead in research and development, with several academic hospitals trialing novel nutrition protocols. South Korea’s aging population and emphasis on functional nutrition are also driving uptake. Moreover, regional manufacturers are introducing cost-effective enteral and oral nutritional products tailored for local taste preferences, improving accessibility and adherence among cancer patients in rural and semi-urban settings.

Emerging Healthcare Ecosystems Supporting Oncology Nutrition Growth in MEA

The Middle East & Africa (MEA) region is gradually adopting oncology nutrition, driven by improving cancer care infrastructure, increased government focus, and growing awareness among healthcare providers. In 2024, the region contributed 6.1% to the global market, with the highest demand observed in the GCC countries, particularly the UAE and Saudi Arabia. Hospitals in Dubai and Riyadh are incorporating oncology nutritionists as part of cancer care teams, focusing on personalized feeding plans for chemotherapy and radiation patients. Additionally, Saudi Arabia’s Vision 2030 healthcare plan includes initiatives that promote the integration of medical nutrition therapies into public hospitals. Africa, although lagging in infrastructure, is seeing pilot projects by international NGOs to deliver cost-effective nutritional care for cancer patients, especially in Nigeria, Kenya, and South Africa. Market growth remains modest but promising, with private hospitals and academic centers leading awareness and product adoption efforts.

The global oncology nutrition market is characterized by moderate to high competition, with several multinational companies and emerging regional players striving to offer innovative, clinically validated nutrition solutions. Key players are investing heavily in R&D to develop condition-specific oral nutritional supplements, immunonutrition products, and advanced enteral formulas. In 2024, over 130 new oncology nutrition formulations were launched globally, with a focus on high-protein, low-sugar, and plant-based options. Companies are entering into strategic collaborations with cancer care hospitals and research institutes to conduct clinical trials and validate the effectiveness of their products. Mergers and acquisitions are also intensifying; for example, a major nutrition company acquired a medical food brand specializing in cancer-specific products to expand its oncology portfolio. Digital platforms and e-commerce are becoming significant distribution channels, especially for oral supplements. The market is further influenced by regulatory approvals and certifications, which are crucial for commercial success in hospitals and clinical settings.

Nestlé Health Science

Danone S.A.

Abbott Laboratories

Fresenius Kabi

B. Braun Melsungen AG

Hormel Foods Corporation

Meiji Holdings Co., Ltd.

Medtrition, Inc.

Victus, Inc.

Global Health Products, Inc.

The oncology nutrition market is witnessing significant technological advancements aimed at enhancing patient care and treatment outcomes. Artificial Intelligence (AI) and Machine Learning (ML) are increasingly being integrated to develop personalized nutrition plans for cancer patients. These technologies analyze vast datasets, including patient medical histories, treatment regimens, and genetic profiles, to provide tailored nutritional recommendations that support recovery and improve quality of life.

In addition to AI and ML, data analytics plays a crucial role in monitoring patient responses to nutritional interventions. By tracking parameters such as weight changes, nutrient absorption rates, and treatment side effects, healthcare providers can adjust nutritional plans in real-time, ensuring optimal patient outcomes. Furthermore, advancements in enteral and parenteral nutrition delivery systems have led to the development of more efficient and patient-friendly feeding mechanisms, reducing the risk of infections and improving compliance.

The integration of telehealth platforms has also revolutionized oncology nutrition by enabling remote consultations and continuous monitoring. Patients can now receive expert nutritional guidance without the need for frequent hospital visits, thereby reducing healthcare costs and improving access to care, especially in remote areas. These technological innovations collectively contribute to a more holistic and effective approach to cancer treatment, emphasizing the critical role of nutrition in patient recovery.

In January 2024, Danone announced a partnership with Resilience, a digital oncology company, to enhance nutritional care for cancer patients. The collaboration aims to develop a novel nutrition and oncology module integrated with Resilience’s digital oncology platform.

In April 2024, Carilion Clinic, Blue Ridge Cancer Care, and Feeding Southwest Virginia inaugurated the first clinic-based food pantry dedicated to serving cancer patients undergoing treatment. Located within Carilion’s Cancer Center, the facility offers patients access to nutritious food options tailored to their treatment needs.

In September 2023, Filtricine Inc., a U.S.-based biotechnology company, introduced Tality, a medical food based on personalized nutrition designed to inhibit the growth of cancer cells. Tality utilizes specific nutrient formulations to target cancer cells while sparing normal cells, representing a significant advancement in oncology nutrition.

In February 2024, Novartis announced plans to acquire MorphoSys AG, a German biopharmaceutical company, for $2.9 billion. This acquisition underscores Novartis' strategic focus on strengthening its oncology pipeline and expanding its portfolio of innovative cancer treatments.

In July 2022, Nestlé introduced China's first Foods for Special Medical Purpose (FSMP) developed specifically for patients with tumor-related ailments. This product launch followed a comprehensive five-year approval process with Chinese regulatory authorities, marking a significant milestone in oncology nutrition in the region.

The Oncology Nutrition Market Report provides a comprehensive analysis of the current trends, technological advancements, and future prospects within the global oncology nutrition landscape. It encompasses detailed insights into various nutrition types, including oral nutritional supplements, enteral nutrition, and parenteral nutrition, highlighting their applications across different cancer types such as head and neck cancer, gastrointestinal cancer, lung cancer, and breast cancer.

The report delves into the end-user segments, examining the roles of hospitals, clinics, research institutions, and home care settings in the adoption and implementation of oncology nutrition solutions. It also explores the impact of technological innovations, such as AI-driven personalized nutrition plans and advanced delivery systems, on patient outcomes and treatment efficacy.

Furthermore, the report analyzes regional market dynamics, identifying key growth drivers, challenges, and opportunities across North America, Europe, Asia-Pacific, and the Middle East & Africa. By providing a holistic view of the market, the report serves as a valuable resource for stakeholders, including healthcare providers, nutritionists, researchers, and industry players, enabling informed decision-making and strategic planning in the evolving field of oncology nutrition.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 2559.81 Million |

|

Market Revenue in 2032 |

USD 4952.75 Million |

|

CAGR (2025 - 2032) |

8.6% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Nestlé Health Science, Danone S.A., Abbott Laboratories, Fresenius Kabi, B. Braun Melsungen AG, Hormel Foods Corporation, Meiji Holdings Co., Ltd., Medtrition, Inc., Victus, Inc., Global Health Products, Inc. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |