Reports

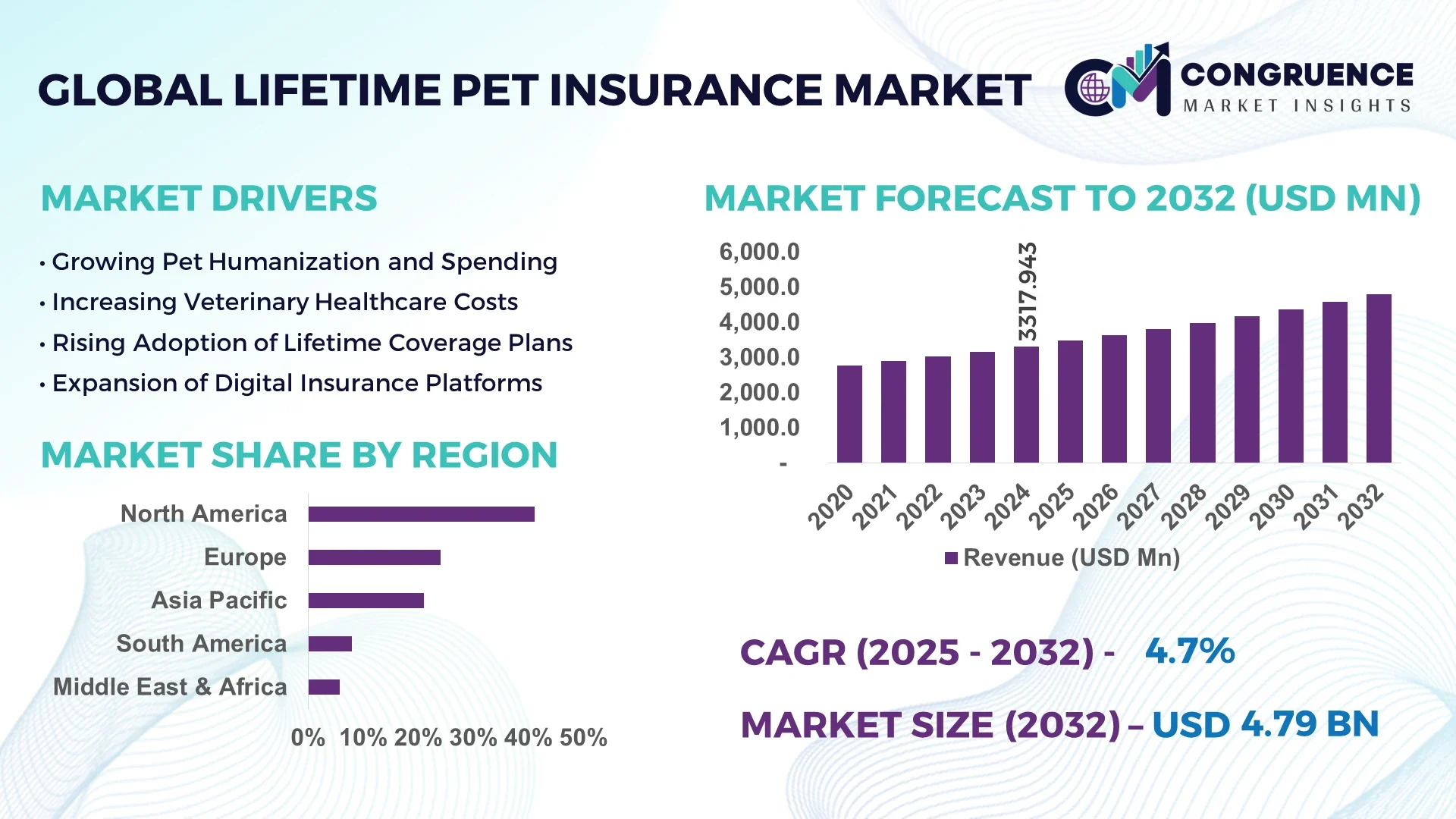

The Global Lifetime Pet Insurance Market was valued at USD 3317.943 Million in 2024 and is anticipated to reach a value of USD 4791.178 Million by 2032 expanding at a CAGR of 4.7% between 2025 and 2032.

The Lifetime Pet Insurance Market is experiencing significant growth due to the rising awareness around pet health and the growing trend of pet humanization. As more pet owners view their pets as family members, the demand for comprehensive lifetime coverage policies continues to rise. These policies are designed to cover chronic illnesses, hereditary conditions, and long-term treatments, offering peace of mind for pet parents. Global players are expanding their offerings with digital platforms that simplify policy comparison, claims management, and customer service. The market is thriving across North America and Europe, with Asia-Pacific emerging as a high-potential region. The rising adoption of cats and dogs, along with veterinary cost inflation, is further boosting the demand for lifetime pet insurance solutions. The global Lifetime Pet Insurance Market is evolving rapidly as insurers innovate coverage options to meet diverse customer needs while maintaining profitability.

Artificial Intelligence is revolutionizing the Lifetime Pet Insurance Market by streamlining operations, improving customer experience, and enabling dynamic risk assessment. AI-driven tools are transforming how insurers assess claims, detect fraud, and provide personalized policy recommendations. AI algorithms can analyze veterinary records, genetic predispositions, and pet health history to determine suitable policy pricing and claim predictions. Chatbots and AI virtual assistants are reducing response times, enhancing customer satisfaction, and minimizing operational costs. Insurtech companies are leveraging machine learning for real-time underwriting decisions, significantly cutting down policy approval time. AI is also helping in predictive modeling to forecast long-term care costs, enhancing accuracy in premium calculations. Companies deploying AI-based analytics platforms are achieving better retention rates and delivering superior claim experiences. With telehealth for pets becoming more mainstream, AI integration in diagnostics is enabling pet insurance providers to offer value-added services. AI is now at the heart of strategic expansion in the Lifetime Pet Insurance Market.

"In March 2024, UK-based pet insurance provider ManyPets partnered with Akur8 to enhance its AI-driven pricing models. This collaboration allows for faster, more accurate underwriting while improving transparency in premium calculations for lifetime pet insurance policies."

The Lifetime Pet Insurance Market is shaped by a complex interplay of evolving consumer preferences, technological innovations, and shifting veterinary care costs. Pet ownership has increased significantly in the past decade, with nearly 66% of households in the U.S. alone having at least one pet. This shift has driven higher expectations for quality pet healthcare, propelling the demand for lifetime insurance products. Technological advancements, especially AI and cloud-based platforms, are improving operational efficiencies and helping insurers provide tailored solutions. On the other hand, rising veterinary treatment costs are pushing customers to seek more comprehensive and long-term insurance options. Key players are investing in digital customer acquisition and mobile apps, streamlining the policy issuance and claims process. Insurers are now focusing on creating value-added services such as wellness programs and telehealth consultations, further intensifying competition in this rapidly growing market.

Increasing Pet Humanization

The growing humanization of pets is a major driver in the Lifetime Pet Insurance Market. Pet parents now demand high-quality healthcare services for their animals, akin to what they expect for themselves. Studies indicate that more than 70% of pet owners in developed countries treat pets as family members. This trend is pushing the need for long-term insurance policies that cover chronic and hereditary illnesses, behavioral therapies, and even dental treatments. Lifetime coverage plans address these concerns by providing comprehensive solutions that extend across the pet’s lifespan. The demand for such policies has notably surged in urban regions, where disposable income and veterinary care access are higher.

High Cost of Premiums

Despite increasing demand, the high cost of premiums remains a significant restraint in the Lifetime Pet Insurance Market. Lifetime policies tend to be more expensive than annual or accident-only policies due to their extensive coverage. For many pet owners, especially in low- and middle-income regions, the monthly or yearly premiums can be a financial burden. Moreover, insurance providers often raise premiums as the pet ages or when claims are made, discouraging renewals. Some policies also include exclusions for pre-existing conditions, leading to dissatisfaction and lower policy adoption. These cost barriers hinder wider market penetration and may slow down growth in price-sensitive regions.

Expansion into Emerging Markets

Emerging markets offer significant growth opportunities for the Lifetime Pet Insurance Market. Countries in Asia-Pacific, Latin America, and the Middle East are experiencing a sharp rise in pet adoption rates due to increasing disposable incomes and changing lifestyles. Veterinary infrastructure is improving, and awareness of pet health is growing. Insurance companies are entering these markets through digital-first approaches, targeting tech-savvy millennial pet owners. The increasing penetration of smartphones and the internet is making it easier for insurers to market and sell lifetime policies. Localization of services and tailored plans based on regional pet care habits further enhance the opportunity for market players to establish a strong footprint.

Limited Awareness in Developing Regions

One of the major challenges faced by the Lifetime Pet Insurance Market is the limited awareness in developing economies. In regions like Africa, South Asia, and parts of Latin America, pet insurance is still a relatively new concept. A majority of pet owners rely on out-of-pocket expenses for pet treatments, unaware of the long-term benefits of insurance coverage. Lack of educational initiatives and poor access to reliable insurance providers further limits market expansion. Additionally, cultural attitudes toward pets and economic priorities in these regions often do not favor long-term financial commitments for animal care. This lack of awareness and education remains a critical barrier to global market expansion.

The Lifetime Pet Insurance Market is witnessing several transformative trends that are reshaping the industry. One key trend is the rise of digital-first insurers offering lifetime pet insurance entirely through mobile platforms. These digital models are making it easier for consumers to access and manage insurance policies. Another emerging trend is the bundling of pet insurance with wellness and preventive care packages. Many insurers now include annual check-ups, vaccinations, and behavioral consultations in their plans. The use of blockchain for policy verification and secure claim processing is also gaining traction. Additionally, the rise in multi-pet households is driving demand for customizable lifetime insurance plans with multi-pet discounts. Personalized insurance packages based on breed, age, and lifestyle are becoming mainstream, increasing customer satisfaction. Behavioral coverage, dental health, and alternative therapies such as acupuncture and physiotherapy are being incorporated into standard lifetime coverage. Sustainability and ESG-aligned policies are also being developed, with insurers focusing on ethical treatment and environmentally conscious services.

The Lifetime Pet Insurance Market is segmented based on policy type, application, and end-user insights, each contributing uniquely to the market’s expansion. The diversity in policy structures allows pet owners to choose coverage according to their pet's specific needs and budget. On the application front, dogs and cats remain dominant, though there’s rising demand for coverage for exotic pets and service animals. Moreover, individual pet owners form the largest end-user group, with veterinary clinics emerging as influential stakeholders offering bundled insurance and wellness plans. Understanding these segmentation dynamics is crucial for stakeholders aiming to penetrate or expand within this competitive landscape.

Accident-Only Lifetime Coverage: Accident-only lifetime coverage continues to hold significant traction in cost-sensitive markets. These policies cover only injuries resulting from accidents, excluding illnesses or long-term diseases. They are often preferred by pet owners with younger, healthy animals at lower risk for chronic conditions. According to pet insurance claim data, accident-related treatments constitute approximately 30% of annual claims globally. These policies are particularly popular in emerging markets where veterinary awareness is still growing. Though limited in scope, they offer affordable entry points for pet insurance, especially for first-time policyholders seeking basic protection against unforeseen events.

Time-Limited Lifetime Coverage: Time-limited lifetime policies provide coverage for a specific period, typically 12 months per condition, even if the condition recurs. These are budget-friendly alternatives to comprehensive plans but have limitations once the time or monetary cap is reached. This type of plan is favored by cost-conscious pet owners who still want protection against major illnesses or accidents. Industry surveys indicate that nearly 22% of new policies in Europe fall under this category, primarily due to their affordability. Insurers often bundle these with optional wellness plans, making them attractive to mid-income pet owners looking for short-term, renewable protection.

Maximum Benefit Lifetime Coverage: Maximum benefit policies offer a capped amount per condition, without a time restriction. Once the financial cap is met for a specific illness or injury, coverage ceases for that condition. This type strikes a balance between affordability and long-term value, particularly for chronic but manageable conditions. Reports indicate this model appeals to pet owners of breeds predisposed to hereditary conditions such as bulldogs or Persian cats. Nearly 27% of lifetime policyholders in North America opt for this plan structure due to its flexibility. It allows continuous treatment of recurring issues, provided the monetary limit hasn’t been exhausted.

Comprehensive Lifetime Coverage: Comprehensive lifetime coverage plans are the most inclusive, covering both accidents and illnesses for the pet’s entire life, often including recurring conditions, alternative therapies, dental care, and behavioral consultations. These plans are in high demand in regions with advanced veterinary infrastructure, such as North America and Western Europe. Research shows that policyholders with comprehensive plans file 2.7x more claims annually, suggesting frequent vet visits. This coverage type holds the largest market share globally due to rising consumer preference for full-spectrum pet care. High premiums are balanced by extensive coverage, making this plan a premium choice for committed pet parents.

Customizable Lifetime Plans: Customizable lifetime plans are gaining popularity, especially among millennial and Gen Z pet owners. These policies allow policyholders to tailor deductibles, benefit caps, and specific inclusions based on breed, age, and lifestyle. Digital platforms have made it easier for consumers to build policies from scratch. According to recent data, customizable plans saw a 38% year-on-year increase in subscriptions in 2024, driven by growing demand for personalized insurance solutions. These plans often integrate wellness programs and telehealth services, appealing to tech-savvy consumers seeking flexibility and transparency. The shift toward personalization is reshaping how insurers structure and market their products.

Dogs: Dogs account for the majority of lifetime pet insurance applications, with approximately 68% of all policies worldwide covering canines. Due to their active lifestyle and breed-specific health issues, dogs are more likely to incur higher veterinary costs over their lifetimes. Large dog breeds, in particular, are more prone to joint disorders, heart conditions, and hereditary diseases, making them ideal candidates for lifetime insurance plans. Insurers frequently tailor their offerings around dog-specific needs, and wellness packages often include routine vaccinations, dental cleanings, and orthopedic screenings. This segment continues to dominate due to the high global dog ownership rate and increasing vet care standards.

Cats: Cats represent the second-largest segment, accounting for nearly 25% of lifetime pet insurance policies globally. While generally considered low-maintenance pets, cats are prone to chronic conditions like kidney disease, diabetes, and thyroid problems, especially in their senior years. Lifetime insurance plans for cats typically emphasize long-term care, prescription diets, and diagnostic testing. The demand for cat coverage is growing in urban regions, where indoor lifestyles and increasing awareness of feline healthcare have influenced buying behavior. Premiums for cat policies are typically lower than those for dogs, but the claim frequency for chronic illnesses tends to be higher, justifying lifetime coverage.

Exotic Pets: in the Lifetime Pet Insurance Market. As of 2024, exotic pet ownership has surged by 12% globally, driven by unique pet preferences among younger consumers. These animals often require specialized care and non-standard veterinary expertise, making treatment costly. Lifetime insurance policies for exotic pets are often limited in availability and vary by species. However, the demand is strong among committed owners who seek financial protection against high-cost emergencies or disease outbreaks. Insurers are gradually expanding offerings to include more exotic species with flexible coverage.

Service Animals: Service animals, including guide dogs and therapy animals, are increasingly covered under lifetime insurance plans due to their specialized roles and high training investments. These animals often undergo rigorous training and are exposed to high-stress environments, making them susceptible to injuries and certain health conditions. Insurance coverage ensures they receive the best possible care, extending their service life and well-being. Data shows that service animals have a 30% higher policy value than regular pets due to tailored inclusions like injury-specific rehab and mental wellness coverage. Governments and non-profits are also partnering with insurers to subsidize these critical policies.

Individual Pet Owners: Individual pet owners are the largest end-user group, accounting for nearly 80% of all policy subscriptions in the Lifetime Pet Insurance Market. With increasing awareness of pet health and rising vet bills, consumers are more inclined to invest in long-term coverage. Urbanization and the trend of delayed parenthood have led to pets becoming primary companions, boosting the emotional and financial investment in pet care. Online platforms, mobile apps, and easy comparison tools have made policy acquisition more convenient. Consumers prefer personalized lifetime plans that align with pet age, breed, and lifestyle, leading to a sharp rise in digital policy adoption.

Veterinary Clinics: Veterinary clinics are emerging as strategic partners in expanding the reach of lifetime pet insurance. Many clinics now collaborate with insurance providers to offer on-site policy guidance and bundled health packages. These clinics play a critical role in educating pet owners about the benefits of long-term insurance. As per 2024 trends, over 35% of new policies were initiated or recommended by veterinary professionals. Clinics benefit by ensuring better compliance with long-term treatments and follow-ups. Some practices even integrate claim management systems for real-time reimbursements, streamlining the customer experience and driving higher retention for insurance companies.

North America accounted for the largest market share at 41.2% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 8.7% between 2025 and 2032.

The dominance of North America is attributed to high pet ownership rates, advanced veterinary healthcare, and increasing consumer awareness regarding pet wellness. Europe followed closely with a 29.5% share, driven by robust pet welfare regulations and rising insurance adoption in Western Europe. Meanwhile, the Asia-Pacific market is witnessing a surge in pet humanization trends, with growing disposable income and digital penetration making insurance policies more accessible. The Middle East & Africa region, although still nascent, is gradually adopting pet insurance, especially in urban pockets. Each region presents a unique growth landscape, shaped by pet ownership behaviors, insurance literacy, and veterinary infrastructure.

Dominance Fueled by High Pet Ownership and Digital Insurance Platforms

North America continues to dominate the Lifetime Pet Insurance Market, accounting for over 41.2% of the global market share in 2024. The United States leads the region, with more than 66% of households owning pets, and approximately 4.85 million pets currently insured under various lifetime coverage plans. Major providers like Trupanion and Nationwide have significantly expanded their offerings through partnerships with veterinary clinics and digital platforms. The popularity of breed-specific and customizable lifetime plans has grown, with tech-savvy pet parents demanding transparent policy structures and mobile app support. Additionally, the growth of pet wellness subscriptions is encouraging bundling with lifetime insurance. Canada also shows an uptick in coverage, especially in provinces like Ontario and British Columbia, where pet care costs are among the highest nationwide.

Rising Demand in Western Europe and Breed-Specific Coverage Driving Growth

Europe captured around 29.5% of the global market share in 2024, with the United Kingdom, Germany, and France being key contributors. The UK remains the largest market, where over 25% of pets are covered under lifetime insurance policies. Regulatory frameworks supporting animal welfare and healthcare are enhancing insurance uptake. Insurers are focusing on breed-specific policies due to growing demand from owners of high-risk breeds like French Bulldogs and Dachshunds. In Germany, lifetime pet insurance plans are increasingly bundled with veterinary wellness services, while France has seen an expansion in online pet insurance platforms. Scandinavian countries, particularly Sweden and Norway, report high penetration rates driven by advanced veterinary systems and strong awareness. Europe’s well-developed legal and consumer frameworks provide a solid foundation for the sustained growth of lifetime pet insurance products.

Pet Humanization and Digital Insurance Access Powering Growth in Asia-Pacific

The Asia-Pacific region, though currently holding a 17.3% market share in 2024, is showing the fastest growth momentum, fueled by rapid urbanization, increasing disposable incomes, and the rising popularity of pet ownership. Japan and Australia are at the forefront, with Japan witnessing an uptick in senior pet insurance plans due to its aging pet population. In China and India, growing e-commerce and digital insurance platforms are driving accessibility to customizable lifetime policies. According to recent surveys, over 36% of urban pet owners in Tier-1 Chinese cities have considered or already purchased a lifetime insurance policy. In Southeast Asia, pet insurance markets are still emerging but gaining traction among millennial pet owners in Singapore, Malaysia, and Thailand. The growing demand for personalized pet care and digital-first insurance products is reshaping the region’s competitive landscape.

Urban Affluence and Premium Pet Care Fueling Regional Adoption

The Middle East & Africa region accounted for approximately 6.2% of the global market share in 2024, with rising demand seen in urban hubs such as Dubai, Riyadh, and Johannesburg. Pet insurance is still in its early phase across the region, but high-net-worth individuals and expatriates are driving interest in comprehensive lifetime policies. In the UAE, luxury pet wellness centers and mobile veterinary services are increasingly partnering with insurers to offer bundled services. South Africa is witnessing moderate growth, supported by an expanding middle class and increased pet health awareness. Limited insurance infrastructure and low penetration in rural areas remain challenges. However, the surge in pet adoption post-COVID-19 and growing digital awareness are expected to elevate market opportunities. Insurers targeting this region are focusing on high-value, customizable coverage for dogs, cats, and imported exotic pets.

The global Lifetime Pet Insurance Market is moderately consolidated, with key players focusing on product innovation, strategic partnerships, and regional expansion to enhance their market positions. In 2024, top insurance providers such as Trupanion, Petplan, and ManyPets dominated the market with a collective presence in over 20 countries. Trupanion, in particular, holds a strong lead in North America, leveraging AI tools to optimize claims processing and underwriting. Meanwhile, European players are concentrating on expanding digital platforms and breed-specific offerings. Insurtech startups such as Wagmo and Pawlicy Advisor have gained traction by offering customizable policies and app-based policy management tools. Established companies are integrating tele-veterinary services and pet wellness apps to improve customer engagement and policy retention. Furthermore, partnerships between veterinary clinics and insurers have led to bundled offerings that cater to preventive and lifetime healthcare needs. Competitive dynamics are driven by innovation, pricing transparency, and customer service excellence in a market where consumer trust is paramount.

Trupanion

Petplan

ManyPets

Figo Pet Insurance

Embrace Pet Insurance

Healthy Paws Pet Insurance

Agria Pet Insurance

Anicom Holdings Inc.

Bow Wow Meow

Petsecure

The Lifetime Pet Insurance Market is undergoing a significant transformation driven by technological advancements. Artificial Intelligence (AI) is at the forefront, enabling insurers to automate claims processing, assess risk profiles, and detect fraudulent activities. AI-powered chatbots and virtual assistants are enhancing customer service by providing instant responses to policy inquiries and claim statuses. Machine learning algorithms analyze vast datasets to personalize insurance plans based on pet breed, age, and health history, improving customer satisfaction and retention.

Blockchain technology is being explored to ensure transparency and security in policy management. By creating immutable records of policy terms and claims, blockchain reduces disputes and enhances trust between insurers and policyholders. Smart contracts automate claim settlements, ensuring timely payouts and reducing administrative costs.

Telemedicine integration is another technological leap, allowing pet owners to access veterinary consultations remotely. This not only improves access to care but also enables insurers to monitor pet health proactively, adjusting coverage as needed. Wearable devices and mobile apps track pet activity and health metrics, providing data that insurers use to offer dynamic pricing models and wellness incentives.

Cloud computing facilitates scalable and flexible IT infrastructure for insurers, enabling rapid deployment of new services and seamless data management. Data analytics tools process real-time information to forecast trends, optimize pricing strategies, and identify new market opportunities.

In summary, the integration of AI, blockchain, telemedicine, and data analytics is revolutionizing the Lifetime Pet Insurance Market, leading to more efficient operations, personalized services, and enhanced customer experiences.

April 2024: Chubb announced plans to acquire Healthy Paws from Aon, enhancing its position in the growing pet insurance market. This strategic move leverages Healthy Paws' expertise to expand Chubb's offerings and meet increasing demand for comprehensive pet health coverage.

April 2024: MetLife Pet Insurance partnered with the Association of Animal Welfare Advancement (AAWA) to support pet owners in lifelong pet care. They will develop educational content addressing veterinary care challenges and recognize innovative animal welfare organizations through the Golden Beagle Award.

November 2023: Fetch partnered with Best Friends Animal Society to aid in their goal of making America a no-kill nation by 2025. Fetch's contributions support Best Friends' efforts in rehoming shelter pets and advocating for animal welfare, aligning with Fetch's mission beyond insurance coverage.

September 2023: Independence Pet Group (IPG) expanded by acquiring Felix, the only U.S. pet insurance brand exclusively for cats. This strategic acquisition broadens IPG's offerings, focusing on comprehensive pet health solutions tailored to cat owners' needs.

August 2023: Global Risk Partners (GRP) entered the UK pet insurance market by acquiring Petsmedicover, now part of Insync Insurance. This enhances GRP's ability to provide innovative insurance solutions and expand its presence in the competitive UK pet insurance sector.

The Lifetime Pet Insurance Market Report provides a comprehensive analysis of the industry's current landscape and future outlook. It examines market dynamics, including drivers, restraints, opportunities, and challenges influencing growth. The report segments the market by type, application, and end-user, offering detailed insights into each category. It also presents regional analyses, highlighting market trends and developments across North America, Europe, Asia-Pacific, and the Middle East & Africa.

Key players in the market are profiled, detailing their strategies, product offerings, and recent developments. The report emphasizes technological advancements, such as AI, blockchain, and telemedicine, shaping the industry's evolution. It also discusses regulatory frameworks impacting market operations and consumer adoption.

Furthermore, the report explores market trends, including the increasing demand for comprehensive pet health coverage, the rise of customizable insurance plans, and the growing importance of digital platforms in policy management. It provides quantitative data on market size, growth rates, and revenue projections, enabling stakeholders to make informed decisions.

Overall, the Lifetime Pet Insurance Market Report serves as a valuable resource for insurers, investors, policymakers, and other stakeholders seeking to understand the market's trajectory and identify opportunities for growth and innovation.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 3,317.943 Million |

|

Market Revenue in 2032 |

USD 4,791.178 Million |

|

CAGR (2025 - 2032) |

4.7% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Trupanion, Petplan, ManyPets, Figo Pet Insurance, Embrace Pet Insurance, Healthy Paws Pet Insurance, Agria Pet Insurance, Anicom Holdings Inc., Bow Wow Meow, Petsecure |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |