Reports

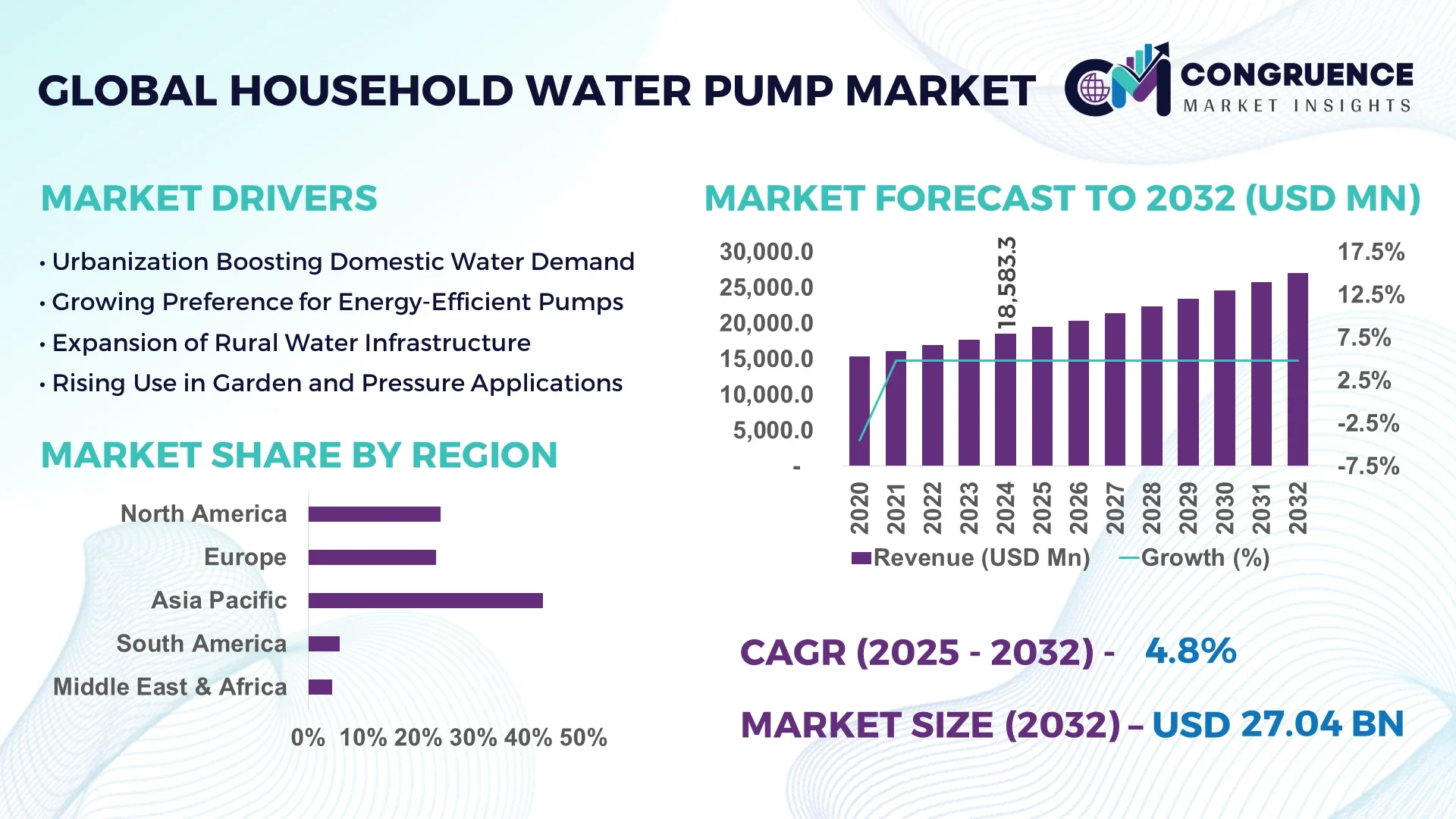

The Global Household Water Pump Market was valued at USD 18,583.3 Million in 2024 and is anticipated to reach a value of USD 27,040.4 Million by 2032 expanding at a CAGR of 4.8% between 2025 and 2032.

The household water pump market in the United States is witnessing robust growth due to increasing demand for reliable residential water supply systems, especially in urban and suburban areas. The U.S. has a high penetration of single-family homes, many of which rely on booster pumps, sump pumps, and pressure pumps for daily operations. Rising awareness around water conservation and energy efficiency, paired with incentives from federal and state governments, is encouraging the adoption of smart water pumps across American households. Smart household water pump systems that provide real-time monitoring, leak detection, and automatic shut-off features are becoming increasingly popular in the U.S., particularly in regions with aging infrastructure or water pressure variability. Additionally, infrastructure modernization and increasing investments in sustainable residential development are fueling the growth of the U.S. household water pump market.

Artificial Intelligence (AI) is transforming the household water pump market by integrating automation, predictive maintenance, and energy efficiency into water pump systems. AI-powered household water pumps can now identify usage patterns, detect anomalies in operation, and even schedule preventive maintenance automatically, reducing the need for human intervention. Smart household water pump systems embedded with AI and IoT (Internet of Things) technologies allow real-time data analytics, optimizing water flow, pressure, and power consumption. For instance, sensors integrated with AI can track energy usage, temperature, pressure fluctuation, and vibration levels to predict equipment failure before it occurs. This dramatically reduces downtime and enhances pump performance across residential properties.

AI is also playing a pivotal role in smart water management by integrating cloud-based platforms that enable remote control and diagnostics of household water pumps via mobile apps or web dashboards. In areas where water scarcity is a concern, AI algorithms help manage water distribution more effectively, ensuring consistent water supply while minimizing wastage. AI-enabled pumps are also aiding utilities and homeowners in managing water bills by delivering consumption data insights. As energy regulations become stricter and users demand more transparency and automation, AI will continue to revolutionize the household water pump market landscape.

"In 2024, Grundfos launched an AI-enabled domestic pump model with predictive diagnostics and automated motor health analytics, reducing maintenance frequency by 25% and downtime by 30%. This development in the household water pump market marks a shift toward AI-powered residential pumping systems aimed at improving operational efficiency and energy conservation."

The household water pump market is influenced by a combination of technological, economic, and environmental factors. Increasing urbanization and residential construction in emerging economies, coupled with the rising need for efficient water supply systems, are key forces propelling market growth. The demand for pressure booster pumps, submersible pumps, and centrifugal pumps in households is surging due to improved living standards and a shift towards smart home solutions. Innovations such as solar-powered water pumps, energy-efficient motors, and intelligent pump controllers are revolutionizing the market landscape. Additionally, growing awareness about water conservation and governmental support for sustainable water infrastructure are encouraging adoption. However, fluctuations in raw material prices and the high cost of smart pump installations may affect market expansion. Regulatory pressures to reduce carbon emissions and water wastage are also reshaping manufacturing standards and pushing companies to develop eco-friendly household water pump solutions.

Rising Urbanization and Growth in Residential Construction

The household water pump market is driven significantly by rapid urbanization and rising residential infrastructure projects across developing and developed countries. According to the United Nations, approximatly 68% of the world population is expected to live in urban areas by 2050. This growth in urban population increases demand for reliable household water pumps for daily residential use. In India alone, the urban housing shortage stood at over 10 million units in 2023, presenting a massive opportunity for water pump manufacturers. The expansion of smart cities and new housing developments further pushes the need for pressure booster and submersible pumps to ensure uninterrupted water supply, even in high-rise buildings. Moreover, rising consumer focus on hygiene and convenience supports market growth.

Increasing Need for Reliable Domestic Water Supply

Despite increasing demand, the household water pump market faces restraints due to high operational and maintenance costs. Traditional water pumps consume a large amount of electricity, accounting for nearly 10%–20% of household energy bills in some regions. Smart water pumps, while more efficient, require significant initial investments and ongoing maintenance costs due to sensor calibration, software updates, and technical support. For instance, advanced AI-enabled water pumps can cost 30%–40% more than conventional models, making them less accessible for low- and middle-income households. In regions with unreliable electricity or infrastructure, the cost of maintaining pumps increases due to voltage fluctuations and wear-and-tear, further limiting adoption in rural markets.

High Installation and Maintenance Costs

The growing global emphasis on sustainability presents a major opportunity for energy-efficient and solar-powered household water pumps. Solar water pumps offer an eco-friendly solution, especially in off-grid or rural areas, and eliminate dependence on erratic electricity supplies. Governments in countries such as India, Kenya, and Nigeria are providing subsidies for solar water pump adoption under rural development programs. According to the International Energy Agency (IEA), solar pump sales in developing countries grew by over 20% annually in the past three years. Additionally, smart water pumps with built-in AI and IoT can reduce energy consumption by up to 30%, which is a strong selling point for eco-conscious consumers. The market is ripe for innovations that combine renewable energy with automation, providing vast growth potential for manufacturers.

Growing Demand for Solar-Powered Pumps

One of the significant challenges in the household water pump market is the increasing pressure to meet environmental compliance standards. Stringent government regulations on energy efficiency, emissions, and water conservation are forcing manufacturers to invest heavily in R&D and adopt cleaner technologies. For example, the U.S. Department of Energy (DOE) mandates efficiency testing and labeling for residential pumps, which adds to manufacturing costs. Complying with global standards such as ISO 9906 or the Energy Star rating system also increases the cost of production and certification. Additionally, navigating differing regulations across countries complicates global distribution and requires region-specific product variations, making scalability and profitability more complex for market players.

The household water pump market is undergoing a significant transformation with several trends shaping its future. One major trend is the adoption of smart pumps equipped with IoT and AI technologies. These smart water pumps provide remote control, automatic scheduling, and diagnostic alerts via mobile applications, making water management more efficient and user-friendly. In 2023, over 40% of new residential pumps sold in developed economies featured smart capabilities. Another key trend is the growing popularity of energy-efficient and variable speed pumps, which adjust motor speed based on demand, reducing power consumption and operational costs. These pumps are gaining traction in urban households focused on sustainable living.

Additionally, solar-powered pumps are becoming increasingly common, especially in rural or semi-urban areas where electricity is unreliable. Compact, low-noise, and portable pump designs are also trending as consumers seek aesthetic and space-saving solutions. The market is witnessing rising demand for corrosion-resistant and long-lifespan materials, which enhance product durability. Moreover, manufacturers are focusing on modular designs and plug-and-play installation systems to simplify setup and maintenance. With digitalization, sustainability, and user convenience as core focus areas, the household water pump market continues to evolve toward intelligent, efficient, and eco-friendly innovations.

The household water pump market is segmented based on type and application, reflecting diverse consumer needs and industrial strategies. In terms of type, leading brands from the U.S., Europe, and Asia dominate specific niches in submersible pumps, centrifugal pumps, and booster pumps. European manufacturers such as GRUNDFOS and WILO are advancing in smart pump technologies, while Chinese companies like Leo Group and Fengqiu focus on mass production and affordability. Based on application, cast iron and stainless steel pumps hold a significant market share due to their durability and corrosion resistance, with increasing demand from residential and agricultural sectors. These segments showcase product diversification in the household water pump market globally.

Centrifugal Pumps: Centrifugal pumps dominate the household water pump market due to their simple design and efficient water handling capacity. These pumps are widely used for shallow water applications and domestic water supply systems. The household water pump market is witnessing strong demand for centrifugal pumps because they provide continuous and uniform water flow for various home utilities. In 2024, centrifugal pumps accounted for over 35% of total household water pump units sold globally. These pumps are highly energy-efficient, require low maintenance, and are available in a wide range of sizes to suit different flow requirements. The increasing adoption of energy-saving centrifugal pumps in urban households is significantly contributing to household water pump market expansion.

Submersible Pumps: Submersible pumps are gaining significant traction in the household water pump market, especially in rural and semi-urban areas where water sources are located deep underground. These pumps operate underwater and are ideal for deep well water extraction. The household water pump market is expanding in this segment due to increased reliance on borewell systems. Submersible pumps minimize noise, offer better efficiency at depth, and reduce priming issues. In 2024, demand for submersible household water pumps grew by 18% globally due to their superior performance in regions with low water tables. Their corrosion resistance and sealed motor construction make them ideal for long-term use in domestic water systems.

Jet Pumps: Jet pumps are commonly used in the household water pump market for shallow and deep well applications. These pumps are ideal for homes where the water level fluctuates seasonally. Jet pumps use a combination of a nozzle and a venturi to create suction, allowing them to draw water from a considerable depth. In the household water pump market, jet pumps are popular due to their affordability, ease of installation, and suitability for intermittent use. In 2024, the jet pump segment held a significant market share in North America, driven by suburban home installations. These pumps are often used in combination with pressure tanks for enhanced functionality in homes.

Booster Pumps: Booster pumps are critical to maintaining adequate water pressure in multi-story buildings and large homes, making them a vital component in the household water pump market. These pumps are especially useful in areas where municipal water supply pressure is insufficient. In the household water pump market, booster pump systems are integrated with pressure control switches and sensors to regulate performance. Demand for booster pumps increased by over 21% in 2024 due to rising high-rise residential construction. These pumps ensure consistent water delivery across all floors and outlets, making them ideal for modern homes and apartments where constant water flow and pressure are essential.

Water Supply & Distribution: Water supply and distribution remain the largest application segment in the household water pump market. Household water pumps are used to draw water from wells, boreholes, tanks, and municipal pipelines for general domestic usage. In 2024, over 45% of installed pumps globally were utilized for water supply and distribution in residential settings. This segment is essential for meeting daily water needs such as drinking, bathing, cooking, and washing. The household water pump market continues to grow in this segment due to increased housing development and water infrastructure modernization. Water distribution systems also benefit from automated control systems to enhance pump performance and efficiency.

Pressure Boosting: Pressure boosting is a vital application in the household water pump market, particularly in high-rise buildings and regions with weak municipal water pressure. Booster household water pumps are deployed to maintain constant water pressure across multiple outlets. In 2024, the pressure boosting segment recorded a strong 20% increase in demand across urban cities worldwide. These systems are increasingly equipped with digital pressure controllers, enhancing energy savings and pump lifespan. The household water pump market is evolving with consumer preferences shifting toward silent and vibration-free booster systems, which are especially popular in densely populated urban environments with multiple bathroom fixtures and large kitchens.

Garden Watering: Garden watering applications are witnessing rising adoption of compact and portable household water pumps, contributing to steady growth in the household water pump market. Homeowners are investing in small-sized surface pumps to automate irrigation tasks and maintain lawns, flower beds, and vegetable gardens. In 2024, garden watering accounted for nearly 12% of the total application share in the global household water pump market. The increasing popularity of DIY gardening and landscaping trends is boosting sales of user-friendly and solar-powered pumps. Additionally, pump manufacturers are offering weatherproof and rust-resistant models designed specifically for outdoor use, further supporting segment expansion in residential and suburban homes.

Residential Homes: Residential homes form the core end-user segment in the household water pump market. Single-family houses depend heavily on water pumps for their day-to-day water supply, pressure boosting, and garden watering needs. In 2024, over 50% of global household water pump installations occurred in independent residential homes. These homes often require pumps that are low-noise, energy-efficient, and capable of handling variable pressure requirements. The household water pump market is focusing on delivering compact and reliable pump solutions for suburban and urban homes alike. Digital controls and smart automation features are gaining popularity among residential homeowners, contributing to market growth.

Apartments & Housing Complexes: Apartments and housing complexes represent a fast-growing end-user segment in the household water pump market due to urban population growth and high-rise development. These buildings require powerful booster and centrifugal pumps capable of distributing water across multiple floors. In 2024, this segment experienced over 15% growth in demand for advanced pressure management solutions. The household water pump market is seeing rising adoption of intelligent pump systems in apartment complexes for centralized control and energy efficiency. Backup pump systems are also increasingly deployed to ensure water availability during peak demand or power outages, making this a strategic growth segment for manufacturers.

Farmhouses & Rural Households: Farmhouses and rural households heavily rely on household water pumps for groundwater extraction and domestic use. Submersible and jet pumps dominate this segment due to deeper water tables and limited municipal water access. The household water pump market is expanding in rural areas thanks to government rural electrification programs and solar water pump subsidies. In 2024, the rural household segment accounted for over 30% of total sales in regions like South Asia and Sub-Saharan Africa. Durability, long runtime, and minimal maintenance are key purchase considerations in this segment. Solar-powered pumps are increasingly adopted in off-grid rural communities, boosting growth.

Small Commercial Establishments: Small commercial establishments, including shops, clinics, and guesthouses, are emerging end-users in the household water pump market. These users require consistent water supply for restrooms, kitchens, and sanitation systems. In 2024, this segment represented 8% of total household pump demand, particularly in mixed-use buildings in developing countries. Pumps used in small commercial spaces emphasize compact design, quiet operation, and automatic pressure regulation. The household water pump market is targeting this segment with hybrid pumps that function in both residential and light commercial environments. Manufacturers are introducing models with built-in filters and overload protection, meeting the specific requirements of commercial users.

Asia-Pacific accounted for the largest market share at 42.6% in 2024; however, the Middle East & Africa region is expected to register the fastest growth, expanding at a CAGR of 6.1% between 2025 and 2032.

The Asia-Pacific region leads the household water pump market due to high demand in India, China, and Southeast Asia, where increasing residential construction and water scarcity issues are driving adoption. Europe followed with 25.4% market share, supported by high-efficiency pump systems in developed countries like Germany and France. North America accounted for 18.9% in 2024, driven by technological integration in residential utilities. Latin America and MEA collectively accounted for over 13.1% share, with infrastructure development and improved water management systems contributing to regional demand. MEA is rapidly advancing due to governmental focus on water infrastructure in countries like Saudi Arabia, UAE, and South Africa.

Technological Advancements Drive Residential Water Efficiency in North America

The North America household water pump market is experiencing steady growth due to advanced water conservation technologies and rising urbanization. The U.S. is a key contributor, with demand for energy-efficient booster and submersible pumps rising in new residential developments. Over 72% of new single-family homes in the U.S. adopted energy-efficient plumbing systems in 2024, fueling water pump integration. Canada also shows increasing adoption in suburban and rural households, particularly in British Columbia and Alberta. Water reuse systems in California and Texas are incorporating automated pumps to improve residential water circulation and storage efficiency, boosting overall market value.

Smart Pump Adoption in Urban Residences Boosts Demand in Europe

In Europe, the household water pump market is expanding due to smart infrastructure investments and a growing emphasis on energy-efficient water management. Germany, France, and the U.K. dominate regional demand, with over 58% of households in Germany using submersible or centrifugal pumps for water pressure regulation and garden irrigation. EU mandates on energy labeling and efficiency have spurred replacement of older pump systems. In 2024, more than 15 million households across the region utilized variable-speed water pumps. Growth in Southern Europe, especially Italy and Spain, is supported by increased demand for residential gardening and solar-powered pumps in off-grid communities.

Population Surge and Urbanization Propel Asia-Pacific Market Growth

Asia-Pacific is the largest and most dynamic market for household water pumps due to population growth, rapid urbanization, and improving water infrastructure. China and India are at the forefront, together accounting for more than 63% of the regional market share. In 2024, over 45 million pumps were sold across India alone, driven by growing household needs in urban and rural settings. Rising disposable income and the adoption of automated water systems have pushed demand for booster and submersible pumps. Southeast Asian nations like Vietnam, Indonesia, and the Philippines are also experiencing accelerated growth in water pump adoption, especially in newly built housing complexes.

Water Scarcity and Infrastructure Projects Boost MEA Pump Demand

The Middle East & Africa household water pump market is witnessing robust growth due to water scarcity challenges, population growth, and large-scale infrastructure projects. In 2024, the UAE, Saudi Arabia, and South Africa led pump installations in new residential zones. Dubai's residential water conservation policy increased sales of pressure-boosting pumps by 32% year-over-year. In Africa, countries like Kenya, Nigeria, and Ghana are expanding rural water supply through subsidized pump distribution. South Africa deployed over 1.4 million pumps in 2024 to meet household and agricultural demands. Government and NGO support for rural electrification and water access projects further accelerate pump market growth.

The household water pump market is highly competitive, marked by the presence of both global and regional manufacturers focusing on innovation, energy efficiency, and automation. In 2024, over 62% of the market was held by the top 15 players, with leading firms expanding their footprint in Asia-Pacific and the Middle East through partnerships and acquisitions. Product differentiation through smart pump technology, IoT integration, and solar-powered variants is a key strategy. Players are also investing in R&D to develop lightweight, durable, and corrosion-resistant pump materials. New entrants from China and India are offering cost-effective solutions, increasing market fragmentation in price-sensitive regions. Moreover, leading manufacturers are establishing regional service hubs to improve after-sales support and customer retention in emerging economies.

Grundfos Holding A/S

Franklin Electric Co., Inc.

Xylem Inc.

Wilo SE

KSB SE & Co. KGaA

Ebara Corporation

Kirloskar Brothers Limited

Zhejiang Doyin Pump Industry Co., Ltd.

Leo Group Co., Ltd.

Dab Pumps S.p.A.

Pedrollo S.p.A.

CRI Pumps Private Limited

Shimge Pump Industry Group Co., Ltd.

Shakti Pumps (India) Ltd.

Calpeda S.p.A.

The household water pump market is witnessing significant technological advancements aimed at enhancing efficiency, sustainability, and user convenience. One notable innovation is the integration of smart pump systems equipped with Internet of Things (IoT) capabilities. These systems allow homeowners to monitor and control water pumps remotely via smartphones or computers, leading to optimized water usage and energy savings.

Variable Frequency Drives (VFDs) are increasingly being incorporated into household water pumps. VFDs adjust the motor speed based on water demand, reducing energy consumption and extending the lifespan of the pump. For instance, VFD-equipped pumps can achieve energy savings of up to 30% compared to traditional fixed-speed pumps.

Solar-powered water pumps are gaining popularity, especially in regions with abundant sunlight. These pumps utilize photovoltaic panels to convert solar energy into electricity, providing an eco-friendly and cost-effective solution for water supply in off-grid areas. In 2024, the adoption of solar-powered household water pumps increased by 18% globally.

In June 2024, LAPP introduced the ETHERLINE® FD bioP Cat.5e, its first bio-based Ethernet cable produced in series. This sustainable variant features a bio-based outer sheath composed of 43% renewable raw materials, reducing the carbon footprint by 24% compared to traditional fossil-based TPU sheaths.

In March 2024, Grundfos launched the SCALA1, a fully integrated, compact, and self-priming water booster pump designed for domestic use. The SCALA1 offers Bluetooth connectivity, allowing users to monitor and control the pump via a mobile app, enhancing convenience and efficiency.

In November 2023, Franklin Electric Co., Inc. unveiled the SubDrive Utility Variable Frequency Drive, designed to provide constant water pressure in residential applications. The drive features advanced protection against voltage fluctuations and dry-run conditions, ensuring reliable operation.

In September 2023, Xylem Inc. introduced the SmartPump series, incorporating IoT technology for real-time monitoring and predictive maintenance. The SmartPump series aims to reduce downtime and maintenance costs for residential water systems.

In July 2023, Wilo SE expanded its product line with the Wilo-Yonos PICO, an energy-efficient circulator pump for residential heating systems. The pump features a user-friendly interface and automatic adjustment capabilities, optimizing performance and energy consumption.

The Household Water Pump Market Report provides a comprehensive analysis of the current market landscape, focusing on technological advancements, regional trends, and key market players. The report examines various types of household water pumps, including centrifugal, submersible, jet, and booster pumps, highlighting their applications in water supply, pressure boosting, and garden watering.

The report delves into the impact of emerging technologies such as IoT integration, solar-powered systems, and variable frequency drives on market dynamics. It also explores the adoption of smart pump systems and the use of advanced materials to enhance pump efficiency and durability.

Regional insights cover North America, Europe, Asia-Pacific, and the Middle East & Africa, analyzing factors driving market growth in each region. The report identifies key trends, such as the increasing demand for energy-efficient and environmentally friendly water pumps, and the growing popularity of smart home technologies.

Furthermore, the report profiles major market players, detailing their product offerings, strategic initiatives, and market positioning. It serves as a valuable resource for stakeholders seeking to understand market trends, identify growth opportunities, and make informed decisions in the household water pump industry.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 18,583.3 Million |

|

Market Revenue in 2032 |

USD 27,040.4 Million |

|

CAGR (2025 - 2032) |

4.8% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Grundfos Holding A/S, Franklin Electric Co., Inc., Xylem Inc., Wilo SE, KSB SE & Co. KGaA, Ebara Corporation, Kirloskar Brothers Limited, Zhejiang Doyin Pump Industry Co., Ltd., Leo Group Co., Ltd., Dab Pumps S.p.A., Pedrollo S.p.A., CRI Pumps Private Limited, Shimge Pump Industry Group Co., Ltd., Shakti Pumps (India) Ltd., Calpeda S.p.A. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |