Reports

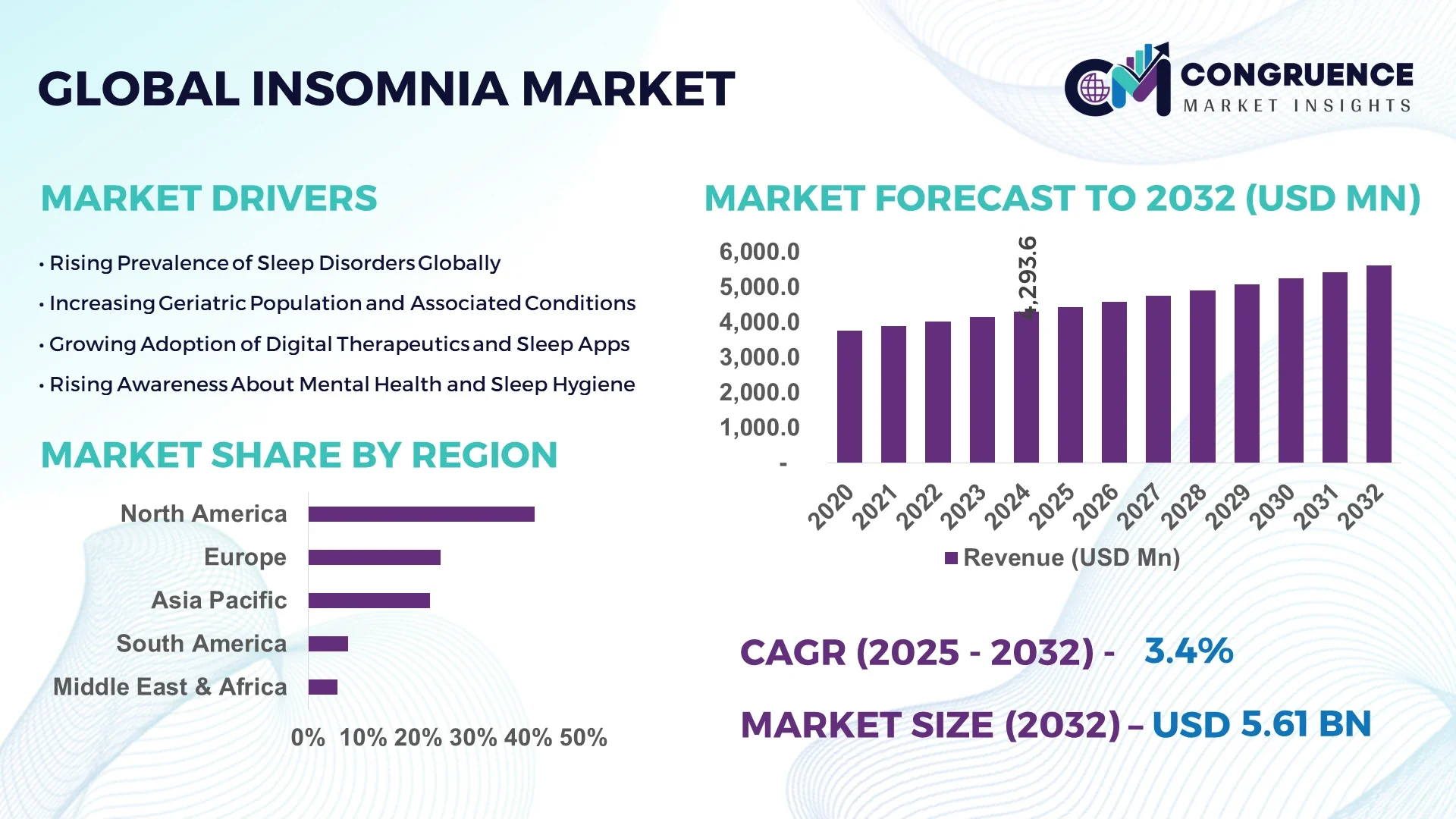

The Global Insomnia Market was valued at USD 4293.58 Million in 2024 and is anticipated to reach a value of USD 5610.27 Million by 2032 expanding at a CAGR of 3.4% between 2025 and 2032.

Insomnia, a prevalent sleep disorder affecting millions globally, is witnessing rising attention due to increasing awareness of mental health, urban stressors, and lifestyle-induced health complications. The global insomnia market is propelled by growing healthcare investments, expansion of digital therapeutic platforms, and escalating demand for over-the-counter (OTC) and prescription-based sleep aids. With the rise in aging populations and work-related stress across regions such as North America, Europe, and Asia-Pacific, the need for efficient insomnia solutions is intensifying. The influx of cognitive behavioral therapy apps, wearable sleep trackers, and innovative prescription medicines is also shaping the competitive landscape. Additionally, governments and health organizations are promoting sleep hygiene awareness, further encouraging market growth. The surge in screen time and shift work schedules is anticipated to keep demand steady for years to come.

Artificial Intelligence (AI) is significantly revolutionizing the insomnia market by enhancing diagnostic accuracy, improving personalized treatment, and boosting patient adherence to therapy. AI-powered mobile applications now deliver tailored cognitive behavioral therapy for insomnia (CBT-I), which has emerged as a preferred first-line treatment over medication due to its long-term benefits and fewer side effects. Companies are integrating AI with wearable devices to monitor sleep patterns in real-time, producing detailed reports to help clinicians fine-tune treatment strategies. Furthermore, AI-driven platforms can detect early signs of insomnia by analyzing speech patterns, behavioral changes, and biometric data. In 2023, more than 40% of digital sleep apps incorporated some form of AI or machine learning algorithms. AI-enabled bots and virtual assistants are now capable of interacting with patients through natural language processing, offering recommendations and tracking sleep diaries effectively. As a result, the global demand for AI-based insomnia therapies is growing, driven by patients' desire for non-invasive, tech-enhanced solutions. AI not only helps in early detection but also empowers users with actionable insights, creating a feedback loop that improves treatment outcomes and minimizes reliance on pharmaceuticals.

"In February 2024, Philips launched an AI-integrated sleep therapy platform called “SmartSleep Analyzer,” which uses machine learning to assess sleep patterns and recommend personalized treatments, enhancing patient engagement and compliance."

One of the significant drivers of the insomnia market is the increasing demand for non-drug-based treatment options, particularly digital therapeutics. Cognitive Behavioral Therapy for Insomnia (CBT-I) has gained widespread acceptance, with the National Institutes of Health recognizing it as a first-line treatment. More than 30% of primary care providers in the U.S. now recommend CBT-I applications before prescribing medication. Moreover, digital therapeutics platforms are expanding rapidly; in 2023, the number of users of insomnia-focused apps grew by over 28%. The convenience, cost-effectiveness, and long-term efficacy of digital treatments are leading patients and providers to favor them over sedative-hypnotics and other pharmacological therapies.

One of the major restraints in the insomnia market is the growing concern about the side effects and dependency risks associated with pharmacological treatments. Benzodiazepines and non-benzodiazepine hypnotics, often prescribed for sleep disorders, have been linked with cognitive impairment, dependency, and increased risk of falls in older adults. Studies show that around 15% of patients using prescription sleep medications report dependency symptoms. Regulatory bodies, such as the FDA, have issued black box warnings on certain sleep medications due to safety concerns. These warnings are influencing physicians and patients to explore alternative treatment options, thereby limiting the growth of pharmaceutical solutions in the insomnia market.

The rise in telehealth adoption presents a substantial opportunity for insomnia treatment providers. Telemedicine platforms now allow patients to receive specialized sleep consultations and therapy sessions from the comfort of their homes. In 2023, telehealth usage for sleep disorders saw a 35% increase in North America alone. This surge is primarily driven by accessibility, convenience, and reduced healthcare costs. Remote CBT-I sessions are especially popular among millennials and working professionals who prefer on-demand support. Additionally, wearable devices integrated with teleconsultation apps are enabling physicians to provide real-time feedback, improving patient adherence and outcomes. The global reach of telemedicine offers untapped growth prospects, particularly in developing markets where sleep specialists are scarce.

Despite increasing incidences of insomnia, a significant portion of the affected population remains undiagnosed due to lack of awareness. Many individuals perceive sleep problems as short-term or unimportant, which delays medical intervention. In fact, over 40% of people with insomnia symptoms do not seek professional help. This underreporting leads to a gap in data collection and treatment availability. Furthermore, primary care physicians may lack the training or tools needed for accurate insomnia diagnosis, often misattributing symptoms to anxiety or depression. This misdiagnosis leads to inappropriate treatment and poor patient outcomes, posing a significant challenge to market growth. Awareness campaigns and better screening protocols are essential to address this issue.

The insomnia market is experiencing several noteworthy trends that are reshaping treatment, diagnosis, and patient engagement. One of the dominant trends is the integration of wearable health devices with mobile health apps that track sleep metrics such as REM cycles, heart rate, and oxygen levels. These tools are gaining popularity, with over 50 million global users in 2023. Another trend is the rise of natural and plant-based sleep aids, driven by consumer preference for chemical-free remedies. Sales of melatonin supplements, for example, rose by 23% in 2023 in North America. Moreover, there's a growing emphasis on personalized medicine, with sleep clinics and app developers offering custom-tailored treatment programs based on genetic, behavioral, and lifestyle data. Subscription-based sleep wellness platforms are also gaining traction, offering CBT-I, meditation guides, and lifestyle coaching as bundled services. Additionally, strategic collaborations between tech companies and healthcare providers are enabling faster commercialization of AI-based insomnia treatments. This evolving landscape signifies a shift from traditional medication-focused solutions to holistic, tech-integrated approaches that promote long-term sleep health.

The global insomnia market is segmented based on type, application, and end-user insights. Each of these segments presents a distinct growth path and specific healthcare needs. By type, insomnia is categorized into primary, secondary, acute, chronic, onset, and maintenance insomnia, each requiring unique therapeutic approaches. By application, the market caters to sleep induction, anxiety and stress management, cognitive behavioral therapy, pain management, and mental health monitoring, highlighting the diverse ways insomnia intersects with physical and psychological health. By end-user, the demand is segmented across adults, geriatric populations, adolescents, healthcare providers, and sleep clinics and centers. The segmentation reveals that while adults are the largest consumers, rising cases in teens and the elderly are boosting specialized treatment needs. These categories also reflect how medical technologies and therapeutic innovations are being tailored to suit different user profiles and clinical situations. With each segment presenting distinct growth drivers and challenges, market participants are optimizing strategies to meet the expanding demand across demographics and therapeutic domains.

Primary Insomnia: Primary insomnia refers to sleep disturbances not directly linked to any other health condition or issue. It accounts for a significant portion of diagnosed cases, especially in urban and working populations. Approximately 25% of people with sleep complaints suffer from primary insomnia, often driven by lifestyle stressors, screen exposure, and irregular work shifts. This type sees high demand for behavioral therapies and non-pharmacological solutions such as CBT-I and mindfulness-based apps. Digital health platforms are expanding services for primary insomnia due to the high prevalence and willingness of patients to adopt self-help tools. Pharmaceutical demand is lower here compared to chronic or secondary types, although OTC sleep aids are frequently used. Primary insomnia continues to be a major target for wellness brands and therapeutic startups looking to offer accessible, tech-integrated sleep management solutions.

Secondary Insomnia: Secondary insomnia results from underlying medical or psychiatric conditions such as depression, chronic pain, or neurological disorders. It represents around 30% to 40% of all insomnia diagnoses. Treatments here often involve addressing the root cause while managing the sleep disorder simultaneously. The market for secondary insomnia includes strong demand for prescription medications, especially sedative-hypnotics and antidepressants. Mental health monitoring apps and connected wearable devices are increasingly used to monitor patients' sleep patterns and correlate them with symptoms of other conditions. Healthcare providers often integrate insomnia management into broader treatment plans, especially for patients with comorbidities like anxiety or cardiovascular disease. The growing burden of lifestyle diseases worldwide is contributing to a surge in secondary insomnia cases, thus driving multi-pronged therapeutic innovations in this segment.

Acute Insomnia: Acute insomnia is short-term, often lasting a few days to weeks, and typically triggered by life stressors such as trauma, job loss, or travel. It affects up to 40% of adults at some point in their lives. While often self-resolving, acute insomnia sees high usage of over-the-counter medications and herbal supplements. The market also sees growth in consumer-directed solutions such as relaxation techniques, mobile CBT-I apps, and sleep environment optimization tools. Acute insomnia is highly prevalent among travelers and students, especially during exams or after major life events. Companies are launching fast-acting sleep aids and digital calming tools to capitalize on this demand. Acute insomnia treatments are particularly popular in the direct-to-consumer segment, reflecting the need for temporary and easily accessible solutions.

Chronic Insomnia: Chronic insomnia, defined as sleep disturbances lasting three months or longer, affects approximately 10% of the global adult population. It has a significant market share due to the long-term and often debilitating impact it has on health. Treatment frequently involves a combination of medication, CBT-I, and lifestyle interventions. Chronic insomnia is closely monitored in clinical settings, with frequent use of polysomnography and wearable diagnostic tools. This type has a high conversion rate into long-term pharmaceutical use, driving demand for prescription sleep aids. Digital therapy platforms offering continuous care and personalized treatment plans are gaining traction. The chronic insomnia segment is a key target for healthcare providers due to its association with increased risk for cardiovascular disease, depression, and reduced productivity.

Onset Insomnia: Onset insomnia is characterized by difficulty falling asleep and is often tied to anxiety, stress, or poor sleep hygiene. This condition is common in adolescents, young adults, and shift workers. Nearly 15% to 20% of people with insomnia report onset-related symptoms. Market solutions include melatonin supplements, sleep hygiene education programs, and mobile applications that help reduce screen time before bed. Wearables and ambient technology such as smart lights and sound machines are often marketed specifically to this group. Onset insomnia management is increasingly integrated with mental health apps, helping users track their mood and sleep latency. Tech-savvy consumers are driving demand for solutions that combine digital relaxation with sleep coaching. This segment is expanding with growing awareness of circadian rhythm disorders and their impact on sleep initiation.

Maintenance Insomnia: Maintenance insomnia is the inability to stay asleep or waking up too early without being able to return to sleep. It is prevalent in older adults and people with chronic health conditions. Approximately 20% of insomnia sufferers experience maintenance-related symptoms. Solutions include both pharmaceutical therapies and wearable monitors that track sleep continuity. New AI-powered platforms offer personalized insights into nocturnal wake patterns, helping individuals and providers address the root cause. Maintenance insomnia is strongly linked to depression and other mood disorders, which often require integrated treatment approaches. The market is seeing an increase in demand for combination therapies, such as sleep-promoting drugs alongside behavioral coaching. Maintenance insomnia continues to be a critical focus for sleep clinics due to its impact on daytime function and long-term health.

Sleep Induction: Sleep induction refers to therapies or treatments that help initiate sleep. This application area dominates the insomnia market, especially for acute and onset insomnia. Products range from sedative medications to natural supplements like melatonin and valerian root. Digital sleep aids such as guided meditation apps, sound therapy, and blue light reduction technologies are widely used. As of 2023, the demand for melatonin supplements grew by over 20% in the U.S. alone. Pharmaceutical companies are continuously launching fast-acting solutions to meet consumer demand for rapid onset sleep. Sleep induction is also the most common reason individuals seek medical consultation for insomnia, making it a critical segment for both pharmaceutical and non-pharmacological solution providers.

Anxiety and Stress Management: Since anxiety and stress are common underlying causes of insomnia, managing these factors is a central application of many insomnia treatment approaches. Approximately 50% of insomnia patients experience clinically significant anxiety. CBT-I platforms, mindfulness apps, and therapy sessions often combine sleep and stress management. In 2023, usage of mental wellness apps with dual sleep-anxiety modules rose by 35%. Pharmaceutical treatments also include dual-action drugs addressing both conditions. This segment is crucial for long-term management of insomnia, especially in young professionals and students. Market growth is further driven by workplace stress, urban lifestyle, and rising cases of burnout and generalized anxiety disorder.

Cognitive Behavioral Therapy: CBT for insomnia (CBT-I) is a gold-standard, non-drug treatment with strong clinical backing. It addresses the psychological triggers and perpetuators of insomnia, such as negative thoughts and sleep-related anxiety. In 2023, digital CBT-I app downloads exceeded 5 million globally, indicating growing acceptance. CBT-I is effective in both acute and chronic insomnia, with outcomes showing sustained sleep improvement without medication. Healthcare systems are increasingly integrating CBT-I into telehealth and insurance programs. Many apps now offer automated CBT modules powered by AI, making the therapy scalable and cost-effective. This application is central to the market shift toward non-pharmacological solutions and long-term sleep wellness.

Pain Management: Chronic pain conditions often result in sleep disturbances, making pain management a key application area for insomnia treatment. Around 60% of chronic pain sufferers report poor sleep quality. This application segment uses a combination of analgesics, sleep-promoting agents, and physical therapies. Market demand is strong in geriatric populations and patients with arthritis, fibromyalgia, or post-surgical pain. Advanced pain management clinics now include sleep assessments as part of their care model. Digital pain trackers and sleep monitors are also being used together to provide holistic patient insights. Pain management as an application continues to grow with the increasing global burden of musculoskeletal disorders.

Mental Health Monitoring: Mental health monitoring in the context of insomnia involves the use of apps, wearables, and clinical tools to track mood, behavior, and sleep quality. This application is particularly useful for patients with comorbid psychiatric conditions such as depression, bipolar disorder, and PTSD. In 2023, more than 30% of mental health apps integrated sleep tracking features. These platforms enable early detection of sleep disruptions, helping healthcare providers adjust therapy before major psychiatric symptoms worsen. Data-driven insights are also helping researchers better understand the interplay between sleep and emotional wellbeing. This segment is growing as awareness increases regarding sleep’s impact on overall mental health.

Adults: Adults make up the largest end-user segment for insomnia treatments, driven by work stress, irregular schedules, and screen overexposure. Around 30% of adults globally experience short-term insomnia. This group relies on a mix of pharmaceuticals, natural supplements, and digital sleep aids. Corporate wellness programs and health insurance plans are increasingly covering sleep therapy for working adults. The growing use of digital wearables and mental health apps also contributes to rising demand. Adults are particularly drawn to CBT-I and on-demand therapeutic platforms, reflecting their preference for flexible and accessible care options. This segment remains a key target for tech-driven and DTC (direct-to-consumer) insomnia products.

Geriatric Population: The elderly population experiences higher insomnia prevalence due to age-related physiological changes, chronic illness, and medication use. Approximately 50% of adults over 65 report some form of sleep disturbance. This group often requires personalized care that includes pharmaceutical treatment, physical therapy, and sleep environment modifications. The market is seeing rising demand for maintenance insomnia solutions, especially long-acting drugs with lower dependency risk. Sleep clinics and elder care centers are integrating sleep assessments into regular geriatric evaluations. This segment is also targeted by smart bed systems and non-invasive monitoring technologies. With an aging global population, demand from this demographic is expected to steadily increase.

Adolescents: Adolescents are increasingly affected by insomnia due to academic pressure, social media usage, and mental health issues. Nearly 15% to 20% of teens report chronic sleep disturbances. Schools, pediatricians, and mental health practitioners are placing more emphasis on early intervention. Teen-focused apps, blue light filtering technologies, and CBT-I programs designed for younger users are seeing growth. Sleep education initiatives are being introduced in schools to raise awareness. The demand for non-drug solutions is particularly high among parents concerned about long-term medication side effects. Adolescents represent a growing, underserved demographic in the insomnia market.

Healthcare Providers: Healthcare providers are both key stakeholders and users of insomnia treatment tools. Sleep medicine specialists, general practitioners, and psychiatrists drive pharmaceutical prescriptions, administer behavioral therapies, and adopt digital diagnostics. The rise of AI-powered platforms and telehealth has enabled providers to scale CBT-I and sleep assessments. In 2023, over 70% of behavioral health practices in North America incorporated digital sleep solutions. Providers also use patient-generated data from wearables and apps to inform diagnosis and monitor outcomes. Continuous training and integration of sleep medicine in primary care practices are expanding the influence of this end-user group.

Sleep Clinics and Centers: Sleep clinics and specialized centers are at the forefront of diagnosing and treating complex insomnia cases. These facilities offer comprehensive services including polysomnography, CBT-I, and medication management. Sleep labs are adopting AI diagnostics and home-based testing kits to improve reach. The number of accredited sleep centers in the U.S. surpassed 2,500 in 2023, reflecting increasing demand. These centers cater to chronic and maintenance insomnia cases, offering multidisciplinary care. Sleep clinics are also critical in data generation and research, partnering with pharmaceutical and digital health companies for clinical trials. Their role in specialized care continues to grow as sleep disorders receive greater attention in public health discussions.

North America accounted for the largest market share at 41.2% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.8% between 2025 and 2032.

The dominance of North America is attributed to high awareness levels, robust healthcare infrastructure, and widespread adoption of digital health tools for insomnia treatment. In contrast, the Asia-Pacific region is experiencing rapid growth due to increasing urbanization, rising mental health concerns, and greater smartphone penetration facilitating digital sleep therapy. Europe held the second-largest share at 28.5% in 2024, fueled by growing geriatric populations and expanding sleep clinics across countries like Germany and the UK. Meanwhile, the Middle East & Africa captured a modest 7.4% share, though the segment is steadily expanding with the improvement of specialized healthcare infrastructure. Regional players are increasingly entering markets with localized CBT-I platforms, wearable devices, and OTC sleep aids, which are boosting accessibility and driving region-specific innovations in insomnia management.

Rising Demand for Prescription Sleep Aids and Digital Therapeutics

In 2024, North America emerged as the leading region in the global insomnia market, capturing a market share of 41.2%. The U.S. leads the regional market due to high insomnia prevalence—affecting over 70 million adults annually—and advanced treatment frameworks. The rising number of FDA-approved medications, including dual orexin receptor antagonists, has boosted prescription-based treatment adoption. Furthermore, the popularity of digital CBT-I platforms such as Somryst and Big Health's Sleepio has soared, especially post-COVID-19. Nearly 60% of users in North America now prefer digital therapies as a first-line treatment. Canada is also experiencing growth with national initiatives addressing sleep disorders in aging populations. Insurance reimbursement for digital behavioral therapies and growing investment in mental health tech companies continue to propel the North American market forward. The integration of AI in sleep monitoring and increased awareness campaigns also contribute to continued innovation in the region.

Expanding Elderly Population Driving Chronic Insomnia Care

Europe held the second-largest market share in 2024, accounting for 28.5% of the global insomnia market. The region’s growth is largely driven by the increasing prevalence of chronic insomnia among the elderly and individuals with mental health comorbidities. In Germany, over 20% of the population aged 65 and older reports chronic sleep disorders. The United Kingdom and France have also expanded their sleep-focused healthcare services, integrating CBT-I into national health systems. Prescription drug usage, particularly Z-drugs and melatonin receptor agonists, remains high in several EU countries. Moreover, rising adoption of sleep diagnostics and polysomnography in countries such as Sweden and Italy is creating demand for accurate sleep tracking tools. Europe is witnessing growing investments in AI-driven mental health apps that include insomnia as a primary feature. Digital therapeutics have gained momentum following regulatory approvals and supportive telemedicine policies across the continent.

Urbanization and Smartphone Penetration Fueling Digital Sleep Solutions

Asia-Pacific is rapidly emerging as the most dynamic region in the insomnia market, with countries such as China, India, Japan, and South Korea witnessing a surge in diagnosed cases. Although the region held 22.9% of the global share in 2024, it is expected to show the fastest growth over the forecast period. In India alone, over 33% of adults in urban areas report symptoms of insomnia, often driven by work stress and screen overuse. Japan remains a mature market with long-standing awareness of sleep disorders, where over 20 million individuals experience some form of insomnia. China is seeing robust growth in app-based CBT-I solutions, with over 10 million downloads of sleep therapy apps recorded in 2023. Smartphone-based monitoring tools and wearable sleep trackers are popular among tech-savvy youth, especially in South Korea. The growing mental health awareness and public health campaigns are helping normalize sleep disorder treatments across Asia-Pacific.

Rising Awareness and Mental Health Integration Support Growth

The Middle East & Africa region accounted for a smaller market share of 7.4% in 2024, but it presents significant potential for growth. Rising awareness around mental health and increasing diagnosis of sleep-related issues are opening up new opportunities in the region. In countries like the UAE and Saudi Arabia, high levels of work-related stress, coupled with late-night screen exposure, contribute to widespread cases of acute insomnia. Local governments are actively integrating mental wellness programs into national healthcare plans, indirectly promoting insomnia screening and treatment. South Africa has also seen an uptick in insomnia cases, particularly in urban centers, where lifestyle disorders are on the rise. While access to sleep specialists remains limited in some areas, digital CBT-I platforms and smartphone applications are bridging the gap. Local healthcare startups are also stepping in with culturally relevant, language-specific insomnia solutions, expanding accessibility in both urban and rural populations.

The global insomnia market is moderately consolidated, with a mix of established pharmaceutical companies and rising digital health firms contributing to its evolution. In 2024, over 35% of total treatment uptake came from prescription drugs, with key players competing in the development of orexin receptor antagonists, GABA modulators, and melatonin-based therapies. The FDA approval of novel agents like daridorexant and lemborexant continues to intensify competition. On the digital front, firms offering CBT-I apps and AI-driven mental health platforms have gained traction. Companies like Pear Therapeutics, Big Health, and Headspace Health are collaborating with insurers to scale access to digital sleep care. Furthermore, wearable tech providers are competing by integrating advanced sleep monitoring features, with brands like Fitbit and Withings launching new sleep tracking capabilities in 2024. Strategic partnerships, product launches, and telehealth integration are core strategies driving competition. Companies are also targeting untapped regions like Asia-Pacific and MEA to expand their customer base and gain a competitive edge.

Idorsia Pharmaceuticals Ltd.

Eisai Co., Ltd.

Merck & Co., Inc.

Pfizer Inc.

Sanofi S.A.

Takeda Pharmaceutical Company Limited

Mylan N.V.

Teva Pharmaceutical Industries Ltd.

Jazz Pharmaceuticals plc

Big Health Ltd.

Pear Therapeutics, Inc.

Headspace Health

Chrono Therapeutics, Inc.

SleepScore Labs

Somryst (A product of Orexo AB)

The insomnia market is undergoing a rapid technological transformation driven by digital therapeutics, artificial intelligence, and wearable innovations. Digital Cognitive Behavioral Therapy for Insomnia (CBT-I) applications are emerging as mainstream alternatives to traditional pharmacological treatments. These digital apps have demonstrated a 70% success rate in improving sleep quality and reducing dependency on sleep medications.

Wearable sleep tracking technology has seen a 35% year-on-year growth, empowering users with real-time sleep data and personalized improvement strategies. Devices like headbands and smartwatches now come integrated with sensors that monitor REM cycles, snoring, and breathing patterns, making them integral to sleep disorder diagnosis and management.

Non-invasive devices such as the Modius Sleep Band have been approved for clinical use, offering innovative approaches to treating chronic insomnia without medication. AI-based platforms are using massive datasets—tracking over 500 million hours of sleep—to deliver hyper-personalized sleep recommendations to users.

These technologies not only improve access to treatment but also reduce therapist shortages, cut waiting times, and enhance clinical decision-making. The convergence of AI, mobile apps, and wearables is redefining the way insomnia is diagnosed and managed, creating a more holistic and tech-driven treatment ecosystem for both patients and providers.

April 2023: A digital therapeutics app for insomnia received regulatory approval in South Korea, aimed at treating sleep disorders by addressing behavioral and cognitive factors using smartphone-based therapy.

November 2023: A wearable device designed to improve sleep quality through neurostimulation received approval from U.S. health authorities, offering a non-invasive alternative for patients with chronic insomnia.

October 2024: An AI-powered sleep platform was launched, utilizing data from hundreds of millions of recorded sleep hours to provide users with personalized sleep assessments and lifestyle recommendations.

July 2024: A new melatonin-based treatment for children suffering from insomnia associated with neurogenetic disorders received positive opinion from a major European medical body.

March 2024: An AI sleep coaching app featuring real-time sound-based sleep tracking was introduced, offering tailored tips and support to help users optimize their sleep patterns.

The insomnia market report offers a broad and in-depth examination of current technologies, market forces, and industry developments. It emphasizes the shift toward digital and non-pharmacological interventions such as CBT-I applications, which are gaining preference due to higher safety profiles and a 70% reported success rate in managing chronic sleep disturbances.

The increasing penetration of wearable sleep monitors is also transforming the market. These devices, which have seen a 35% rise in consumer adoption, allow for continuous monitoring of sleep cycles and biometrics, enabling proactive intervention before sleep issues become chronic. Technologies offering non-invasive treatment methods are becoming more mainstream, particularly for individuals seeking alternatives to sleep-inducing drugs.

The report covers regional trends and outlines the high concentration of advanced sleep technologies in North America, while identifying the Asia-Pacific region as a growing hub for mobile-based and AI-integrated sleep solutions. Moreover, it highlights the challenges of traditional insomnia treatments, such as reliance on sedative medications, and evaluates how innovation is reshaping diagnosis and care delivery.

This comprehensive analysis is crucial for stakeholders aiming to capitalize on emerging trends, improve patient outcomes, and meet the growing demand for innovative sleep disorder solutions in a technology-forward landscape.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 4,293.58 Million |

|

Market Revenue in 2032 |

USD 5,610.27 Million |

|

CAGR (2025 - 2032) |

3.4% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Idorsia Pharmaceuticals Ltd., Eisai Co., Ltd., Merck & Co., Inc., Pfizer Inc., Sanofi S.A., Takeda Pharmaceutical Company Limited, Mylan N.V., Teva Pharmaceutical Industries Ltd., Jazz Pharmaceuticals plc, Big Health Ltd., Pear Therapeutics, Inc., Headspace Health, Chrono Therapeutics, Inc., SleepScore Labs, Somryst (A product of Orexo AB), Technology Insights for th |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |