Reports

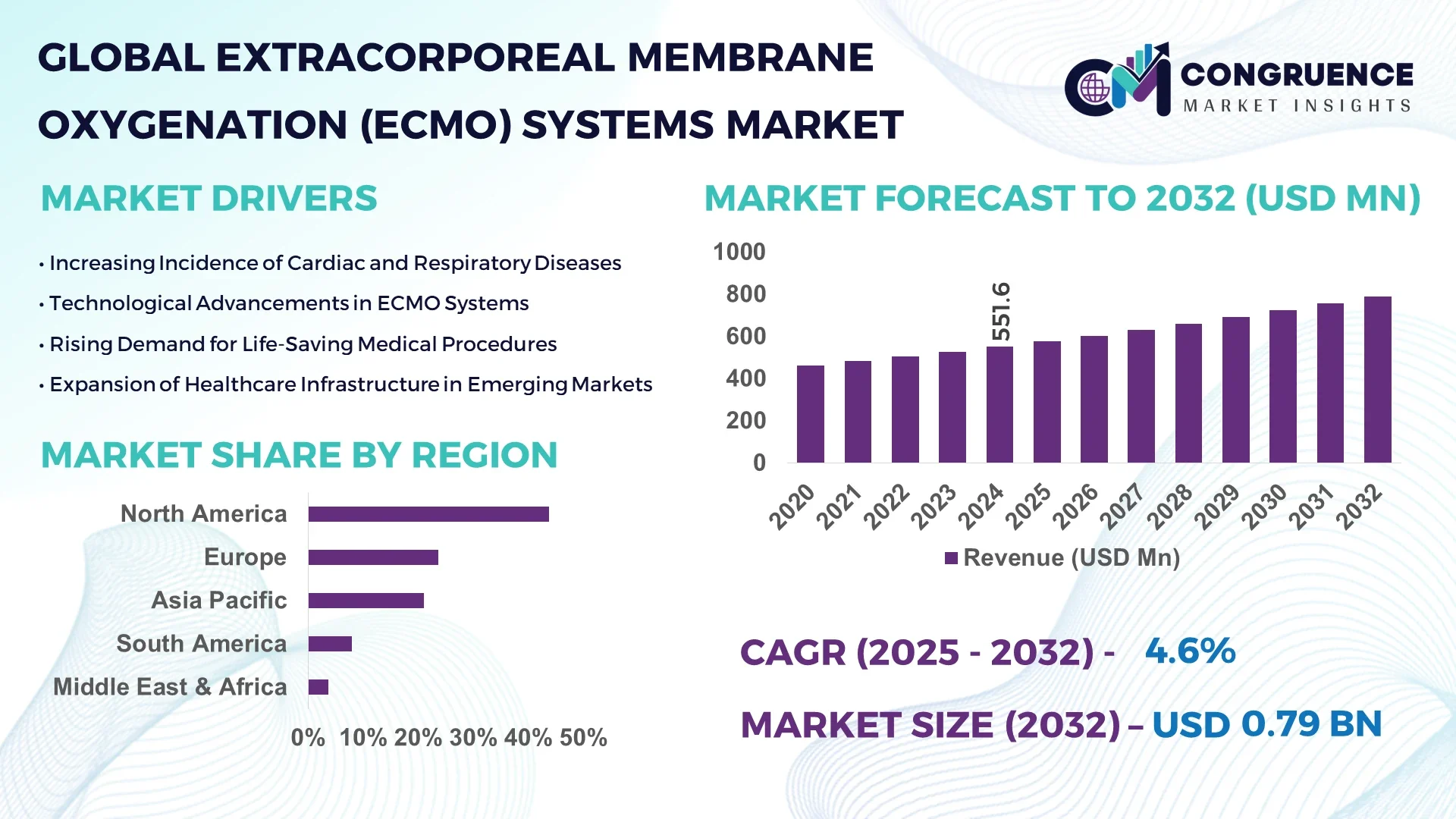

The Global Extracorporeal Membrane Oxygenation (ECMO) Systems Market was valued at USD 551.6 Million in 2024 and is anticipated to reach a value of USD 790.5 Million by 2032 expanding at a CAGR of 4.6% between 2025 and 2032.

The United States dominates the Extracorporeal Membrane Oxygenation (ECMO) Systems market, owing to its robust healthcare infrastructure, significant investment in critical care technologies, and a high number of patients requiring cardiac and respiratory support therapies.

The Extracorporeal Membrane Oxygenation (ECMO) Systems market is witnessing remarkable growth due to an increase in the prevalence of respiratory failures and cardiac disorders globally. Rising adoption of ECMO systems during surgeries, particularly in cardiac and pulmonary procedures, has been significantly pushing market growth. Technological innovations like portable ECMO systems, combined with improved patient outcomes and longer ECMO support times, are further enhancing demand. Hospitals and specialized clinics are increasingly adopting ECMO systems to improve survival rates in patients suffering from severe respiratory and heart conditions. The awareness about early intervention using ECMO systems is spreading rapidly across emerging economies, boosting market penetration.

Artificial Intelligence is significantly transforming the Extracorporeal Membrane Oxygenation (ECMO) Systems market by improving patient management, real-time monitoring, and predictive maintenance of ECMO devices. AI-powered algorithms are now capable of analyzing patient vitals continuously, predicting complications, and adjusting ECMO flow rates in real-time to optimize patient outcomes. Integration of AI into ECMO systems is enabling early detection of mechanical failures, reducing downtime, and preventing life-threatening incidents during therapy. AI-assisted decision support systems are empowering clinicians with better insights, facilitating customized ECMO therapy tailored to individual patient needs, and enhancing survival rates. Additionally, machine learning models are being used to stratify risk in patients undergoing ECMO support, helping healthcare providers prioritize critical cases more effectively. Predictive analytics through AI is also playing a pivotal role in managing resources within intensive care units where ECMO systems are deployed. The growing use of AI tools is enhancing ECMO systems' operational efficiency, leading to higher adoption across hospitals globally.

"In January 2025, Getinge launched an advanced AI-powered module for its Cardiohelp ECMO system that allows predictive hemodynamic monitoring. This new feature uses machine learning algorithms to predict potential cardiac and respiratory instability several minutes before they occur, helping clinicians intervene early and improve patient outcomes during ECMO therapy."

The increasing burden of cardiovascular and respiratory diseases is a major driver propelling the Extracorporeal Membrane Oxygenation (ECMO) Systems market. With millions of new cases of heart failure, chronic obstructive pulmonary disease (COPD), and acute respiratory distress syndrome (ARDS) reported annually worldwide, the demand for life-saving ECMO therapy is soaring. Hospitals are investing heavily in ECMO systems to treat critical conditions where conventional treatments fail. The expansion of emergency care units and rising incidences of cardiopulmonary diseases, particularly among aging populations, are strongly pushing the need for ECMO system deployments across the globe.

The high initial setup costs, maintenance expenses, and operational complexity of Extracorporeal Membrane Oxygenation (ECMO) systems remain a major restraint for market growth. Many healthcare institutions, especially in low- and middle-income countries, find it financially challenging to procure and maintain ECMO equipment. The intensive labor, training requirements, and ongoing consumable costs related to ECMO therapy also add to the financial burden. As a result, access to ECMO therapy is largely restricted to high-end hospitals and specialty centers, limiting broader market penetration and adoption across various healthcare settings.

Emerging economies such as India, China, Brazil, and South Africa are witnessing an increase in investment in healthcare infrastructure, creating new opportunities for ECMO systems market expansion. Government initiatives to improve critical care units, coupled with rising disposable incomes and increasing health awareness, are encouraging hospitals to invest in advanced life support technologies. Moreover, partnerships between private and public sectors for the establishment of ECMO centers are expected to open significant growth opportunities. Rising patient awareness regarding the availability and benefits of ECMO therapy is also fueling demand in these emerging regions.

One of the primary challenges in the Extracorporeal Membrane Oxygenation (ECMO) Systems market is the shortage of highly trained healthcare professionals capable of operating ECMO devices. The complexity of ECMO therapy demands specialized knowledge and continuous monitoring by expert clinicians, perfusionists, and critical care nurses. Many hospitals face difficulty in maintaining an adequately trained workforce to support 24/7 ECMO operations, leading to operational inefficiencies and limiting the scalability of ECMO programs. The situation is more severe in rural and underdeveloped areas where access to training programs and experienced medical personnel remains limited.

• Increasing Use of Portable ECMO Systems:

Portable ECMO systems are rapidly gaining traction, particularly in emergency response and military applications. The miniaturization of ECMO devices has enabled easier transport of critically ill patients without compromising life support. Growing investments in mobile health units and air ambulance services are driving the demand for compact and portable ECMO systems, especially in North America and Europe.

• Rising Adoption of Long-term ECMO Therapy:

There is a growing trend toward the use of ECMO systems for extended periods, sometimes lasting several weeks. Technological advancements have enabled ECMO systems to support patients for longer durations with fewer complications, improving survival rates in cases of severe respiratory failure and post-cardiac surgery recovery. Hospitals are establishing long-term ECMO programs to cater to this evolving patient need.

• Integration of Telemedicine with ECMO Management:

Telemedicine is increasingly being integrated with ECMO systems, enabling remote monitoring and specialist consultations for critical cases. Hospitals are leveraging tele-ICU models where ECMO experts can provide real-time advice and oversight for bedside teams. This trend is particularly prominent in regions facing a shortage of ECMO specialists and is enhancing patient outcomes significantly.

• Development of Biocompatible and Durable Materials for ECMO Circuits:

Manufacturers are focusing on developing ECMO circuits using advanced biocompatible materials that reduce clot formation and minimize the need for anticoagulation. The innovation in membrane oxygenators and tubing materials is enhancing patient safety, reducing the risk of inflammatory responses, and making ECMO therapy safer for prolonged usage. Demand for next-generation ECMO consumables is surging as healthcare providers prioritize patient-centric care.

The Extracorporeal Membrane Oxygenation (ECMO) Systems market is segmented based on type, application, and end-user, offering a detailed view of market dynamics. By type, the market covers veno-arterial (VA), veno-venous (VV), and arterio-venous (AV) ECMO systems. By application, the segments include respiratory, cardiac, and extracorporeal cardiopulmonary resuscitation (ECPR). On the basis of end-users, the market is segmented into hospitals, clinics, and ambulatory surgical centers (ASCs). Each of these segments plays a crucial role in shaping the demand for ECMO systems across different geographies. Innovations, an increasing number of critical care admissions, and expansion in healthcare infrastructure are fueling the market segmentation growth. Understanding the specific contribution of each segment helps key players in strategic planning and product development.

The type segmentation within the Extracorporeal Membrane Oxygenation (ECMO) Systems market includes Veno-Arterial (VA), Veno-Venous (VV), and Arterio-Venous (AV) systems. Veno-Arterial (VA) ECMO currently leads the market, owing to its widespread use in both cardiac and respiratory failure cases. VA ECMO systems offer dual support, making them crucial for patients undergoing cardiogenic shock or cardiac arrest, thus commanding the largest market share. Veno-Venous (VV) ECMO systems are the fastest-growing segment due to the rising incidence of severe respiratory failures, such as Acute Respiratory Distress Syndrome (ARDS), particularly after the COVID-19 pandemic. VV ECMO provides excellent oxygenation support without direct cardiac intervention, making it increasingly favored in ICU settings. Arterio-Venous (AV) ECMO, though used less frequently, is finding niche applications, but its growth remains comparatively slower. The overall market sees a robust push from technological upgrades, ensuring safer and longer-term usage of both VA and VV systems.

In terms of application, the Extracorporeal Membrane Oxygenation (ECMO) Systems market is segmented into respiratory, cardiac, and extracorporeal cardiopulmonary resuscitation (ECPR) uses. Respiratory application is currently the leading segment, driven by the high number of cases involving severe lung conditions like ARDS, pneumonia, and pulmonary embolism. Hospitals are increasingly relying on ECMO support for patients experiencing respiratory failures unmanageable through mechanical ventilation. However, the fastest-growing application segment is extracorporeal cardiopulmonary resuscitation (ECPR), driven by its effectiveness in improving survival rates during cardiac arrests. Increasing awareness about the benefits of rapid deployment of ECMO during cardiac emergencies has contributed to the growing adoption of ECPR in emergency and intensive care units. Cardiac application also remains strong but grows at a steady pace, focusing on patients with advanced heart failure, myocardial infarction complications, and during high-risk cardiac surgeries.

Based on end-user, the Extracorporeal Membrane Oxygenation (ECMO) Systems market is categorized into hospitals, clinics, and ambulatory surgical centers (ASCs). Hospitals dominate the market due to their extensive critical care facilities, availability of trained ECMO specialists, and higher patient volumes. Large tertiary hospitals and academic medical centers are particularly heavy users of ECMO systems for both adult and pediatric patients requiring prolonged support. Clinics are also growing steadily, especially those specializing in pulmonary and cardiac care, as outpatient ECMO therapy becomes more accessible. However, ambulatory surgical centers (ASCs) represent the fastest-growing end-user segment. ASCs are rapidly adopting ECMO systems for use in elective and emergency cardiac surgeries due to faster patient turnover and growing patient preference for minimally invasive treatment options. Expansion of outpatient critical care services and the push for healthcare cost reduction are driving the adoption of ECMO systems across ASCs.

North America accounted for the largest market share at 43.7% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.3% between 2025 and 2032.

The dominance of North America is attributed to its advanced healthcare infrastructure, strong presence of leading ECMO system manufacturers, and high prevalence of cardiopulmonary diseases. Meanwhile, Asia-Pacific’s growth is fueled by rising healthcare expenditure, increasing patient awareness, and rapid development of healthcare facilities across countries like China, India, and Japan. Europe, South America, and Middle East & Africa also contribute significantly, each presenting unique market opportunities driven by evolving healthcare needs and improving access to critical care technologies.

The North America ECMO Systems market is driven by a surge in the number of accredited ECMO centers and technological advancements. The U.S. leads the region with a high volume of cardiac and respiratory failure cases requiring ECMO support. Hospitals are increasingly adopting portable ECMO devices and AI-enabled monitoring systems to enhance patient care quality. Canada also shows strong growth with expanded critical care programs and government support for advanced healthcare technology adoption. Approximately 75% of the region’s ECMO procedures are performed in the U.S., underscoring its pivotal role in driving regional market dynamics. ECMO deployment during cardiac surgeries and lung transplant procedures is becoming a standard protocol across major North American hospitals.

Europe’s ECMO Systems market continues to flourish with strong adoption in cardiothoracic surgeries and transplant centers. Germany dominates the regional landscape, accounting for over 28% of the total ECMO installations in Europe, closely followed by France and the United Kingdom. Hospitals are investing heavily in next-generation ECMO technology that offers extended run times and enhanced patient compatibility. Post-operative ECMO therapy, particularly after complex cardiac surgeries, is becoming more prevalent in Europe. An increase in organ transplant activities and initiatives to improve access to advanced life-support technologies are further accelerating market growth across Europe.

Asia-Pacific is experiencing the fastest expansion in the ECMO Systems market, led by countries like China, Japan, and India. China alone accounts for over 35% of the regional market, with an impressive rise in the number of hospitals deploying ECMO for emergency care and cardiopulmonary support. Japan’s healthcare institutions are leveraging ECMO extensively during cardiac surgeries and acute respiratory distress treatments. India is witnessing a notable increase in ECMO usage driven by growing patient populations and greater affordability of critical care services. Government initiatives to strengthen ICU capacities and a rise in private healthcare investments are vital contributors to the market’s robust growth trajectory in Asia-Pacific.

The South America ECMO Systems market is steadily growing, mainly fueled by Brazil and Argentina. Brazil holds the majority share in the region, contributing approximately 41% to the total South American ECMO market. Increasing cases of respiratory illnesses and cardiac disorders are propelling the demand for ECMO services. Major hospitals in Brazil are enhancing their critical care units with state-of-the-art ECMO devices to address growing patient needs. Argentina is also showing promising growth with expanding healthcare access and an increasing number of ECMO training centers. Limited access to skilled healthcare professionals still poses a challenge, but government efforts to enhance critical care facilities are positively impacting market dynamics.

The Middle East & Africa ECMO Systems market is gaining momentum, particularly in Gulf countries like Saudi Arabia and the UAE. Saudi Arabia accounts for nearly 36% of the regional market, followed closely by the UAE. Investment in modernizing healthcare infrastructure, especially the establishment of advanced intensive care units in major hospitals, is boosting ECMO adoption. ECMO therapy is increasingly being utilized for complex cardiac surgeries, respiratory failure cases, and transplant support in high-end healthcare facilities. Africa is seeing slow but steady growth, mainly concentrated in South Africa, where private healthcare networks are expanding critical care services. The region still faces challenges related to affordability and trained personnel, but ongoing healthcare reforms are expected to drive further market expansion.

Top Two Countries Holding Highest Market Share:

United States: USD 187.6 Million in 2024, driven by advanced healthcare systems and a high number of accredited ECMO centers.

Germany: USD 59.3 Million in 2024, supported by strong adoption in cardiac and respiratory treatment facilities.

The global Extracorporeal Membrane Oxygenation (ECMO) Systems market is highly competitive with a moderate to high level of market consolidation. Leading companies are heavily investing in R&D to innovate safer, more portable, and efficient ECMO devices. Major players focus on expanding their portfolios with hybrid ECMO systems that combine both respiratory and cardiac support. Partnerships with hospitals and critical care centers are becoming a major strategy to increase global market penetration. Manufacturers are also strengthening their presence through geographical expansion in emerging markets like India, China, and Brazil. In 2024, over 62% of the global ECMO market was controlled by the top five players. There is a significant trend towards miniaturization and AI-integrated ECMO solutions aimed at reducing operational complexities and improving patient outcomes. Moreover, the growing demand for specialized ECMO services post-pandemic has intensified competition among companies, encouraging continuous technological enhancements and value-based care models.

Getinge AB

Medtronic plc

LivaNova PLC

MicroPort Scientific Corporation

Terumo Corporation

Fresenius Medical Care AG & Co. KGaA

Abbott Laboratories

Nipro Corporation

OriGen Biomedical, Inc.

Xenios AG (a Fresenius Medical Care company but listed independently for market relevance)

Technological advancements in the Extracorporeal Membrane Oxygenation (ECMO) Systems market are transforming patient care, emphasizing device miniaturization, automation, and real-time monitoring capabilities. Portable ECMO systems have gained significant traction, enabling patient mobility even during critical care, which drastically improves recovery rates. Integration of artificial intelligence (AI) for predictive analytics is helping clinicians optimize treatment plans and detect complications earlier. Innovations in oxygenators, such as polymethylpentene (PMP) fiber membranes, are enhancing gas exchange efficiency and durability, allowing for longer ECMO runs without membrane failure. Smart ECMO consoles equipped with touchscreen interfaces and advanced alarm systems are improving usability and patient safety. Battery-operated systems with longer life cycles are supporting emergency transports within and between facilities. Furthermore, the development of wearable ECMO prototypes for pediatric and neonatal patients is underway, aiming to reduce hospitalization time. In 2024, approximately 48% of the newly launched ECMO devices featured advanced AI or IoT-based technologies, indicating a clear shift towards smarter, safer critical care management solutions.

• In March 2024, Getinge launched its new Cardiohelp System upgrade, featuring an enhanced touch-screen user interface and improved battery management for extended mobility during ECMO therapy.

• In February 2024, Medtronic unveiled its latest portable ECMO system designed specifically for emergency use in field hospitals, offering rapid deployment capabilities during cardiac and respiratory emergencies.

• In October 2023, LivaNova introduced the Essenz™ ECMO System in European markets, integrating real-time monitoring and smart alert technologies to support better clinical decision-making.

• In August 2023, Terumo Corporation expanded its CAPIOX® FX Advance Oxygenator series by introducing a new high-flow variant aimed at supporting adult patients requiring prolonged extracorporeal life support.

The Extracorporeal Membrane Oxygenation (ECMO) Systems Market Report covers a comprehensive range of critical factors driving the global industry. It provides a detailed overview of market dynamics, including drivers such as the increasing incidence of cardiopulmonary diseases and the growing adoption of ECMO therapy in both adult and pediatric populations. The report examines technological innovations, market segmentation, competitive landscape, and regional performance insights to offer stakeholders a deep understanding of growth opportunities. It highlights the strategic initiatives undertaken by key players, such as product launches, mergers, acquisitions, and partnerships. Furthermore, it identifies emerging trends such as AI integration, miniaturized ECMO devices, and rising demand for portable systems. The report also sheds light on challenges like the high cost of treatment and the shortage of trained professionals. Through extensive quantitative and qualitative analysis, this market study provides actionable intelligence to manufacturers, investors, healthcare providers, and policymakers aiming to tap into the rapidly evolving ECMO systems market landscape.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 551.6 Million |

|

Market Revenue in 2032 |

USD 790.5 Million |

|

CAGR (2025 - 2032) |

4.6% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Type:

By Application:

By End-User:

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Getinge AB, Medtronic plc, LivaNova PLC, MicroPort Scientific Corporation, Terumo Corporation, Fresenius Medical Care AG & Co. KGaA, Abbott Laboratories, Nipro Corporation, OriGen Biomedical, Inc., Xenios AG |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |