Reports

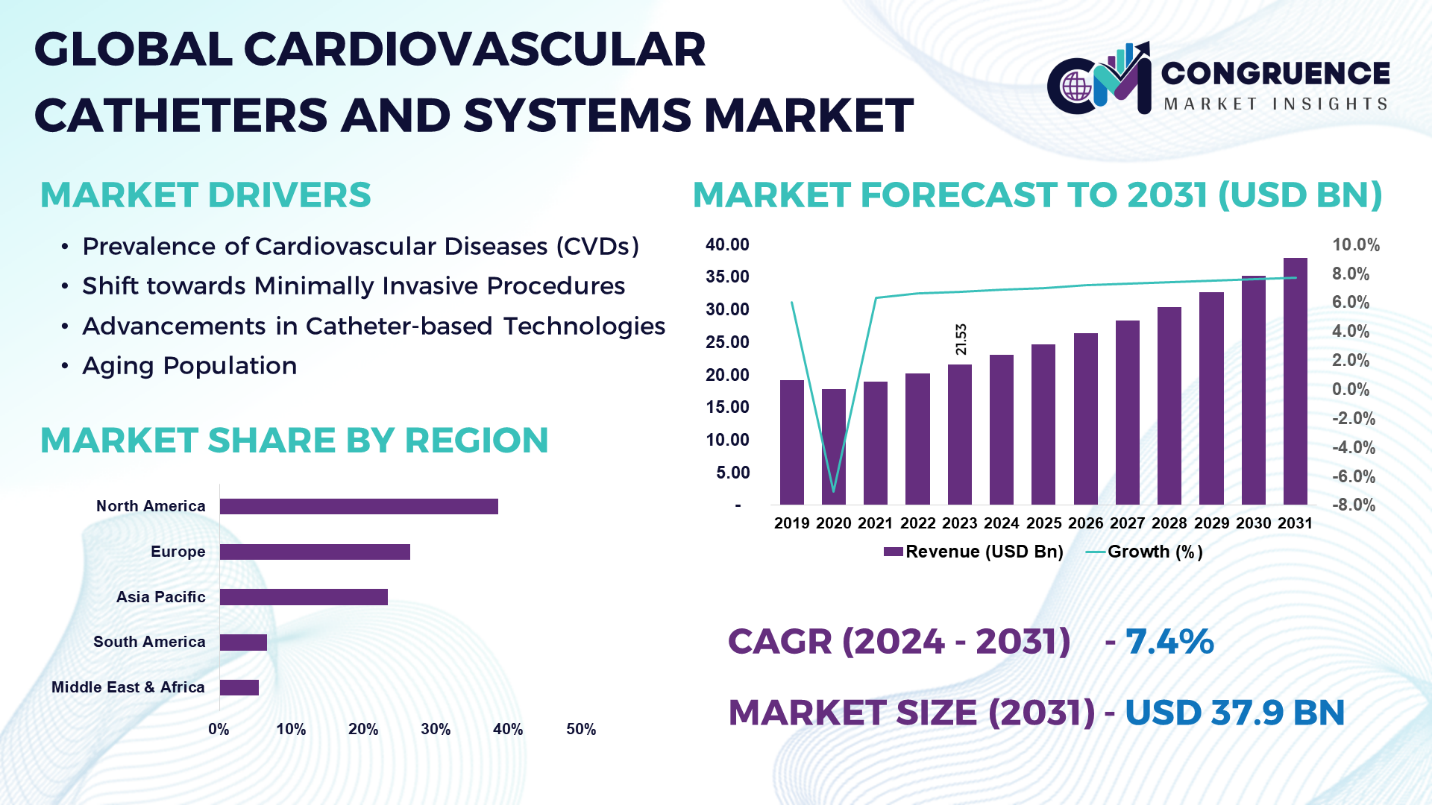

The Global Cardiovascular Catheters and Systems Market was valued at USD 21.53 Billion in 2023 and is anticipated to reach a value of USD 37.90 Billion by 2031 expanding at a CAGR of 7.4% between 2024 and 2031.

The demand for cardiovascular catheters and systems in global market is increasing day by day. This is due to the increasing number of patients suffering from CVDs and also to the implementation of minimally invasive surgery. In the recent past, advancements have been made in catheter-based interventions; thus, attributions such as better material used in catheters, better visualization, and improved navigation tools have expanded both the scope and value of minimally invasive cardiovascular interventional therapies. These include the realization of the need to shift from the cost and length of procedures that are offered as measures towards encouraging the delivery of more comprehensive value-based healthcare, concern towards reducing the hospital length of stay, and the broader concern of reducing the costs of health care, which are some of the key drivers that continue to encourage the use of minimally invasive procedures rather than conventional surgical treatments. This trend is further fueling the cardiovascular catheterization systems and critical care instruments market since patients operated with such instruments require a shorter time to recover, experience fewer post-surgery complications, and have better outcomes.

Cardiovascular Catheters and Systems Market Major Driving Forces

Prevalence of Cardiovascular Diseases (CVDs): The common cardiovascular diseases include coronary artery disease, heart failure, and arrhythmias among others, and an increase in the overall prevalence of these diseases has consequently led to the higher use of cardiovascular catheters and systems.

Shift towards Minimally Invasive Procedures: The tonnage for cardiovascular catheters and systems is advancing due to the increased preference for non-invasive treatments over conventional open surgeries since the cardiovascular catheters and systems cause least invasive procedures, minimal period of recuperation, and can be less expensive when compared to open surgeries.

Advancements in Catheter-based Technologies: Emerging opportunities, including better materials for catheters, superior visualization techniques, better directional aids, are continuously increasing the functionality and efficiency of cardiovascular catheters and systems putting energy in the growth of the market.

Aging Population: Another factor is the increased incidence of cardiovascular diseases due to an ageing population in developed countries and emerging economies. The occurrence of cardiovascular diseases increases, for which cardiovascular catheters and systems for diagnostics, treatment, and management are required.

Cardiovascular Catheters and Systems Market Key Opportunities

Technological Advancements: There is a potential for the for the creation of opportunities as catheter technologies are relatively new and ever-changing, creating room for further advancements in the catheter type. It will be possible for firms to put their capital into research to bring in new cardiovascular catheters and systems that can fit the required clinical applications.

Personalized Medicine: With a smaller volume but high potential for technological advancement in the field, the growing concept of personalized medicine may foster innovations in cardiovascular catheters and systems suited to specific patient metrics and diseases specific to an individual. Precision medicine broken down involves opportunities for the companies to develop diagnostics as well as treatments that are likely to be specific to the patient.

Remote Monitoring and Telehealth: The expansion of remote monitoring, tele supervision, and telehealth solutions indicates possibilities for cardiovascular catheters and systems’ connectivity with digital health platforms. In order to create catheter systems that are linked to a constitution of data that may be closely monitored and ongoing consultation with an accredited caregiver when necessary, companies that manufacture catheters must make the necessary advancements.

Cardiovascular Catheters and Systems Market Key Trends

· Increasing adoption of minimally invasive cardiovascular procedures.

· Advancements in catheter-based imaging technologies.

· Growing integration of AI and machine learning in catheter systems.

· Rising demand for drug-eluting and bioresorbable stents.

· Expansion of robotic-assisted catheterization techniques.

· Development of hybrid operating rooms for complex cardiovascular procedures.

· Increasing focus on personalized and precision medicine.

· Integration of telehealth and remote monitoring with cardiovascular systems.

· Growth in use of 3D printing for custom catheter components.

· Surge in clinical trials and research for innovative catheter technologies.

Region-wise Market Insights

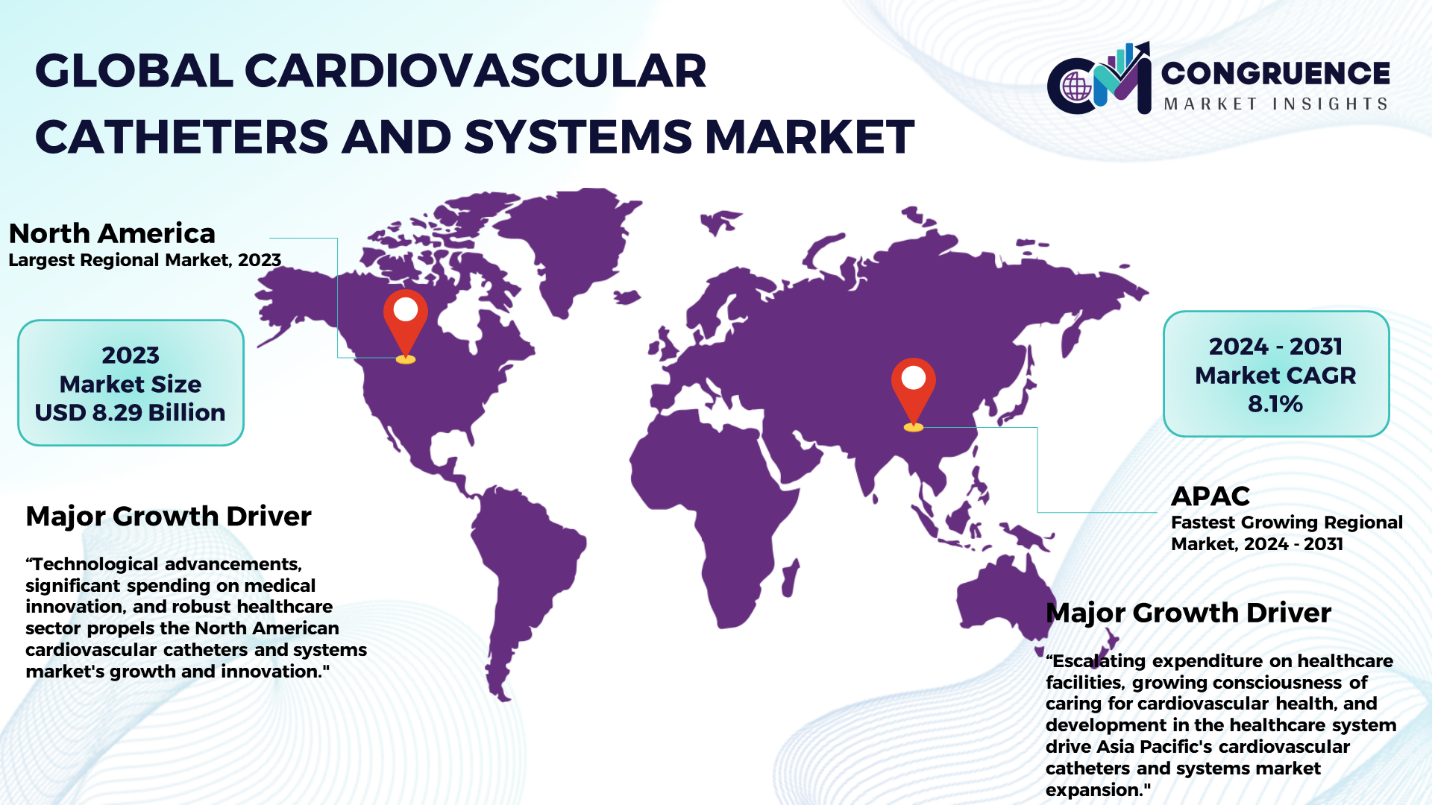

North America accounted for the largest market share at 38.5% in 2023 whereas, Asia Pacific is expected to register the fastest growth, expanding at a CAGR of 8.1% between 2024 and 2031.

Based on the geographic locations of the countries, the global cardiovascular catheters and systems market demonstrates a highly fluctuating pattern owing to the stronger or weaker healthcare facilities, economic power, or incidences of diseases. The market in North America holds the largest potential, owing to the high prevalence of CVDs, the developed healthcare sector, and significant spending on medical innovation. The United States is one of the most active markets on the technological front, with a robust healthcare sector that hosts most of the key market players. Europe is closely ranked, with countries such as Germany, France, and the UK focusing on the fewer operations and health care organizations. The Asia-Pacific region is experiencing significant growth due to the escalating expenditure on healthcare facilities, growing consciousness of caring for cardiovascular health, and development in the healthcare system. Some of the countries highlighted in the report are China, Japan, and India, for they are foreseen to have a rising demand due to the increasing prevalence of cardiovascular diseases and improvements in the standard of treatment. The Latin American market is going to be a faster-growing market, as is the Middle East and Africa, even if compared to the emerging markets. Brazil and Mexico in South America are gradually incorporating technological adoption into their operations, though not without certain economic and infrastructural barriers, while countries in the Middle East and Africa, such as the United Arab Emirates and South Africa, are also starting to incorporate these changes into their entities.

Market Competition Landscape

Major players such as Boston Scientific Corporation, Medtronic, Johnson & Johnson & Abbott Laboratories, have a larger portfolio, reputation, and insurance in the sectors including minimally invasive R & D. These leading markets will remain committed to preserving innovation in catheter solutions such as drug elution stenting, bioabsorption stenting, and robotic enabled catheterization systems with improved client efficacy and disciplined operational fulfillment. New entrants and even middle-sized companies are also not left behind in the competition, since they are presenting differentiated and specialized products which, from other ordinary products, might also cater for some specific clinical needs. Time and again, market leaders such as Cardinal Health, Terumo Corporation, and B Braun Melsungen AG have aligned them primarily according to their technological capabilities and expanded portfolios to capture a larger share of the market. This market is especially marked with smart usage of mergers and acquisitions that facilitate the firms seeking the desired technologies, expansion of geographic locations and overall enhancement of positions in this contest. Prominent players in the market include:

· Medtronic

· Boston Scientific

· Abbott Laboratories

· Johnson & Johnson

· Cardinal Health

· Terumo Corporation

· B. Braun Melsungen AG

· Philips Healthcare

· Cook Medical

· C.R. Bard (a subsidiary of Becton, Dickinson and Company)

· Biotronik

· Siemens Healthineers

· Edwards Lifesciences

· Stryker Corporation

· Merit Medical Systems

|

Report Attribute/Metric |

Details |

|

Market Revenue in 2023 |

USD 21.53 Billion |

|

Market Revenue in 2031 |

USD 37.90 Billion |

|

CAGR (2024 – 2031) |

7.4% |

|

Base Year |

2023 |

|

Forecast Period |

2024 – 2031 |

|

Historical Data |

2019 to 2023 |

|

Forecast Unit |

Value (US$ Mn) |

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Segments Covered |

· By Product Type (Angiography Catheters, Angioplasty Catheters, Diagnostic Catheters, Electrophysiology Catheters, Intravascular Ultrasound (IVUS) Catheters, Others) · By End User (Hospitals, Ambulatory Surgical Centers, Cardiac Catheterization Laboratories, Specialty Clinics) · By Application (Coronary Artery Disease, Electrophysiology, Structural Heart Disease, Peripheral Vascular Disease, Others) |

|

Geographies Covered |

North America: U.S., Canada and Mexico Europe: Germany, France, U.K., Italy, Spain, and Rest of Europe Asia Pacific: China, India, Japan, South Korea, Southeast Asia, and Rest of Asia Pacific South America: Brazil, Argentina, and Rest of Latin America Middle East & Africa: GCC Countries, South Africa, and Rest of Middle East & Africa |

|

Key Players Analyzed |

Medtronic, Boston Scientific, Abbott Laboratories, Johnson & Johnson, Cardinal Health, Terumo Corporation, B. Braun Melsungen AG, Philips Healthcare, Cook Medical, C.R. Bard (a subsidiary of Becton, Dickinson and Company), Biotronik, Siemens Healthineers, Edwards Lifesciences, Stryker Corporation, Merit Medical Systems. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |