Reports

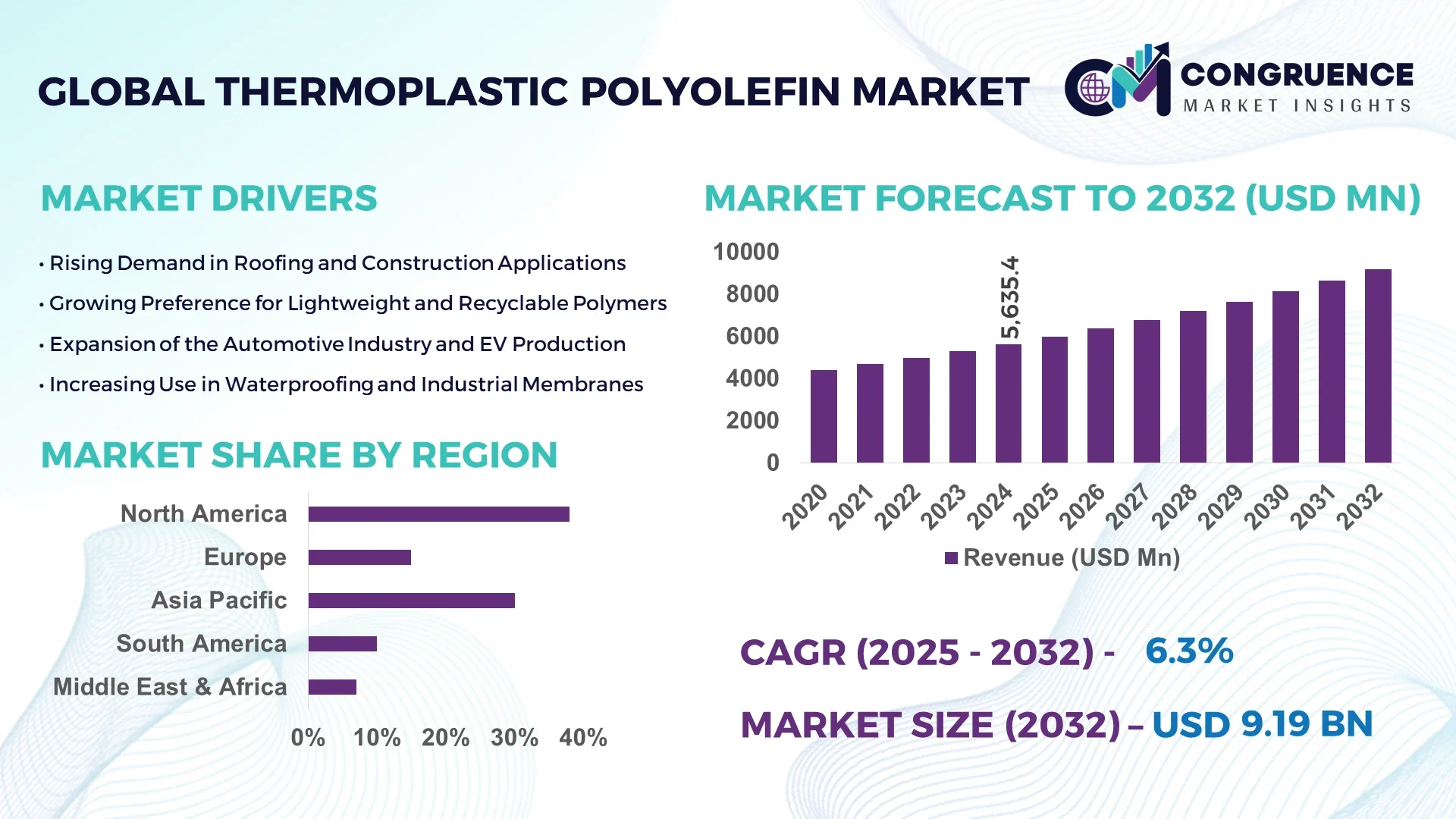

The Global Thermoplastic Polyolefin Market was valued at USD 5635.38 Million in 2024 and is anticipated to reach a value of USD 9187.33 Million by 2032 expanding at a CAGR of 6.3% between 2025 and 2032. The growth is largely attributed to rising demand in automotive and construction applications due to superior durability and recyclability.

In the United States, which dominates the Thermoplastic Polyolefin market, advanced production facilities have scaled output to more than 2.1 million tons annually, supported by heavy investment in polymer compounding technologies and extrusion capacity. The market is strongly driven by the automotive sector, where nearly 45% of thermoplastic polyolefins are utilized in bumper fascias and interior components, while the construction sector accounts for more than 30% share, primarily in roofing membranes and insulation systems. Continuous research in lightweighting and sustainable polymers has further boosted technological adoption, while federal incentives for eco-friendly building materials are accelerating wider usage across industries.

Market Size & Growth: Valued at USD 5635.38 Million in 2024, projected to reach USD 9187.33 Million by 2032, expanding at a CAGR of 6.3%. Growth driven by automotive lightweighting and sustainable construction materials.

Top Growth Drivers: 45% adoption in automotive, 30% efficiency improvement in roofing systems, 25% increase in demand for recyclable plastics.

Short-Term Forecast: By 2028, production efficiency expected to improve by 22%, with a 15% reduction in overall material costs.

Emerging Technologies: Advancements in UV-resistant formulations and nanocomposite-enhanced TPO membranes.

Regional Leaders: North America projected at USD 3.5 Billion by 2032 with strong automotive adoption; Europe reaching USD 2.4 Billion driven by sustainability regulations; Asia-Pacific at USD 2.9 Billion supported by industrial infrastructure expansion.

Consumer/End-User Trends: Automotive, roofing, and packaging sectors continue to dominate adoption with growing preference for lightweight and durable materials.

Pilot or Case Example: In 2024, a leading automaker integrated TPO into next-gen EV platforms, achieving a 12% vehicle weight reduction.

Competitive Landscape: Market leader holds approx. 18% share, with competitors including Dow, ExxonMobil, LyondellBasell, Borealis, and SABIC.

Regulatory & ESG Impact: Green building codes and circular economy initiatives fueling adoption of recyclable and low-emission TPOs.

Investment & Funding Patterns: Over USD 1.2 Billion invested globally in new TPO production lines and R&D facilities since 2022.

Innovation & Future Outlook: Integration of bio-based TPOs and advanced compounding technologies expected to redefine product performance and sustainability in the coming decade.

The Thermoplastic Polyolefin market is witnessing robust adoption across automotive, construction, and packaging sectors, each contributing significant shares to overall demand. The automotive industry is driving innovation with high-performance, lightweight polymers to meet fuel-efficiency and EV design requirements, while the construction industry is integrating TPO roofing membranes for enhanced weather resistance and sustainability compliance. Technological innovations, such as nanotechnology-based reinforcements and improved UV-resistant compounds, are enhancing durability and extending product lifecycle. Regulatory drivers, including stricter emission standards and sustainable building codes, are further accelerating adoption. Regional consumption patterns highlight strong adoption in North America and Asia-Pacific, with Europe leading in environmental compliance-based applications. Emerging trends include bio-based formulations, smart material integration, and advanced recycling techniques, which are shaping the industry’s transition toward a circular economy. This evolving landscape positions the Thermoplastic Polyolefin market as a cornerstone of future industrial, automotive, and construction advancements.

The Thermoplastic Polyolefin (TPO) market plays a strategically pivotal role in modern industries such as automotive, construction, and packaging, driven by its superior durability, cost efficiency, and recyclability. Advances in polymer compounding and nanocomposite technology are reshaping performance benchmarks. For example, nanofilled TPO delivers 28% higher tensile strength compared to conventional polyolefins, enabling lighter yet stronger applications in automotive exterior parts. Regional variations are also shaping the competitive landscape—North America dominates in production volume, while Europe leads in adoption, with over 62% of construction enterprises integrating TPO roofing membranes into sustainable projects.

Short-term projections indicate rapid efficiency gains. By 2027, AI-enabled extrusion control systems are expected to cut production waste by 18%, significantly enhancing cost-effectiveness for large-scale manufacturers. The ESG dimension is equally critical, as global firms are committing to at least 35% recycling of TPO by 2030, aligning with circular economy goals. Real-world scenarios further highlight measurable impact—in 2023, Japan achieved a 22% reduction in automotive plastic waste through AI-powered sorting and recycling initiatives.

These pathways emphasize that the Thermoplastic Polyolefin Market is no longer just a cost-effective material option but a pillar of resilience, compliance, and sustainable growth, driving industries toward next-generation innovation and environmental responsibility.

The automotive sector is a major driver of Thermoplastic Polyolefin market growth, with over 45% of TPO consumption linked to automotive components such as bumpers, fascias, and interior trims. Automakers prioritize TPO due to its lightweight nature, which supports fuel efficiency and electric vehicle performance. Studies show that using TPO-based parts can reduce vehicle weight by up to 12%, directly translating into lower emissions and improved battery range for EVs. Furthermore, demand for recyclable and sustainable materials is reshaping supply chains, as manufacturers shift away from PVC toward TPO for environmental compliance. The automotive industry’s continuous investment in material innovation ensures TPO remains integral to next-generation vehicle platforms.

One of the primary restraints in the Thermoplastic Polyolefin market is the volatility in raw material prices, particularly polypropylene and polyethylene, which account for a significant portion of production costs. For example, global polypropylene prices saw spikes of nearly 20% in 2023, directly impacting profitability for manufacturers. Supply chain disruptions, largely driven by geopolitical tensions and energy costs, have amplified these fluctuations. Additionally, the capital-intensive nature of developing specialized TPO grades makes manufacturers highly sensitive to input cost variations. These dynamics limit the ability of smaller players to scale operations competitively, thereby restraining market expansion and increasing reliance on large, vertically integrated producers.

The construction sector offers significant growth opportunities for the Thermoplastic Polyolefin market, particularly in roofing membranes and insulation systems. TPO roofing has become a sustainable alternative due to its 30% higher energy efficiency in reflective roofing systems compared to traditional asphalt membranes. With global green building certifications increasing, adoption is accelerating—especially in Europe and North America, where regulatory frameworks emphasize energy-efficient materials. In Asia-Pacific, large-scale infrastructure projects are also boosting demand, with TPO projected to cover more than 1.5 billion square meters of roofing area by 2030. These developments highlight TPO’s potential to anchor long-term growth through sustainability-driven construction initiatives.

While recyclability is a core advantage of Thermoplastic Polyolefin, achieving compliance with increasingly stringent environmental standards poses challenges. Regulatory bodies in Europe and North America now require minimum 25–30% recycled content in construction plastics, pushing manufacturers to upgrade recycling infrastructure. However, the lack of uniform recycling systems and high costs associated with advanced polymer sorting technologies limit widespread implementation. Additionally, developing bio-based TPO formulations that match the durability of petroleum-derived materials remains a scientific and commercial hurdle. These compliance and innovation challenges add layers of cost and complexity, slowing the pace of adoption in certain industries despite growing demand.

• Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the Thermoplastic Polyolefin market. Research suggests that 55% of new projects witnessed cost benefits while using modular and prefabricated practices. Pre-bent and cut elements are prefabricated off-site using automated machines, reducing labor needs and shortening timelines by up to 22%. Demand for high-precision machines is rising, particularly in Europe and North America, where construction efficiency is critical, with 48% of new roofing projects incorporating TPO membranes.

• Expansion of Automotive Lightweighting Initiatives: Increasing focus on fuel efficiency and emission reduction is driving the use of TPO in automotive applications. Lightweight TPO components now make up 41% of automotive exterior parts, with studies showing a potential weight reduction of up to 12% per vehicle. Adoption is particularly strong in electric vehicles, where reduced weight improves battery range by an estimated 8–10%. Automotive suppliers in Asia-Pacific are integrating TPO into over 38% of production lines to meet regulatory and performance targets.

• Growth of Sustainable Building Materials: Sustainability is reshaping construction material demand. Over 62% of new commercial roofing projects globally now integrate TPO membranes for their durability and recyclability. Reflective TPO roofing offers up to 30% better energy efficiency than traditional materials, driving adoption in Europe and North America. Increasing green building certifications and stricter building codes are further accelerating TPO utilization in large-scale infrastructure projects.

• Digital and Smart Manufacturing Adoption: Industry 4.0 trends are transforming TPO manufacturing. AI-based extrusion control systems now reduce scrap rates by up to 18%, while predictive maintenance technologies cut equipment downtime by 14%. Over 42% of TPO manufacturers in North America and Europe have adopted IoT-enabled systems for real-time quality control, significantly improving product consistency. This digital transformation supports faster innovation cycles and reduced production costs.

The Thermoplastic Polyolefin market is segmented by type, application, and end-user, each influencing adoption patterns and industry strategies. By type, TPO membranes dominate due to their durability and energy efficiency, while TPO compounds and blends cater to niche automotive and construction applications. In terms of applications, roofing systems, automotive exterior parts, and industrial liners lead adoption due to their performance and regulatory compliance. End-user insights reveal strong uptake in construction and automotive, while packaging and infrastructure are emerging sectors. This segmentation allows targeted innovation, ensuring TPO products meet specific functional and regulatory requirements, driving sustainable growth globally.

TPO Membranes lead the market, accounting for approximately 52% of adoption, driven by their superior weather resistance and energy efficiency. Roofing membranes alone represent a significant application, with adoption rates exceeding 60% in commercial projects in North America and Europe. TPO Compounds follow at about 28%, primarily used in automotive parts due to their lightweight and recyclable properties. TPO Blends hold a combined 20% share, used for specialized applications such as flooring and industrial liners, where flexibility and durability are critical. Adoption of TPO membranes continues to grow due to construction regulations and sustainability trends, while blends are gaining traction in niche industrial applications.

Roofing systems dominate the Thermoplastic Polyolefin market, representing 46% of global application share due to high demand for durable, energy-efficient solutions. TPO roofing offers superior UV resistance and energy reflectivity, making it a preferred choice in commercial and industrial projects. Automotive exterior parts follow with 33% share, driven by the lightweighting trend and sustainable manufacturing initiatives. Industrial liners and packaging represent smaller segments, together contributing 21% to the market, with growing adoption in infrastructure and green building projects. The fastest-growing application is automotive exterior parts, with increasing use of TPO for bumpers, trims, and fascias. By 2027, integration of AI-driven quality control is expected to reduce defects in automotive TPO parts by 15%.

Construction is the leading end-user segment, accounting for 49% of TPO consumption, driven by regulatory focus on sustainability and energy efficiency. Over 65% of new commercial buildings in North America incorporate TPO roofing membranes. Automotive ranks second, representing 31% of the end-user base, as manufacturers integrate TPO in exterior and interior components for lightweighting and recyclability benefits. Packaging and infrastructure make up the remaining 20%, with rising adoption in emerging markets. The fastest-growing end-user is the automotive sector, with a 20% increase in adoption over the past two years due to electric vehicle lightweighting demands. Automotive manufacturers in Asia-Pacific now use TPO for over 42% of exterior components.

North America accounted for the largest market share at 38% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.1% between 2025 and 2032.

In 2024, North America consumed over 1,750 kilotons of Thermoplastic Polyolefin (TPO), with roofing and automotive applications accounting for 68% of demand. Asia-Pacific consumption reached nearly 1,120 kilotons, led by China (42%) and Japan (19%), supported by infrastructure and automotive growth. Europe accounted for 24% of the market, with Germany and the UK leading TPO adoption. South America and the Middle East & Africa together contributed 15% of global demand, driven by construction and energy projects. Rising investment in green building materials, with over $1.2 billion invested globally in 2024, is shifting consumption patterns. By 2027, Asia-Pacific’s volume is projected to exceed 1,600 kilotons due to expanding manufacturing hubs and regulatory emphasis on sustainability.

How is sustainability and digital transformation shaping the market landscape?

North America holds a 38% share of the global Thermoplastic Polyolefin market, driven primarily by the roofing (45%) and automotive (30%) sectors. Increased adoption in green building projects has been supported by stricter energy codes and government incentives worth $850 million in 2024. Digital transformation in manufacturing—such as IoT-based extrusion control—has reduced waste by 16% and improved efficiency. Local leaders like Carlisle Construction Materials have expanded TPO membrane production, introducing new high-reflectivity roofing systems adopted in over 500 projects in 2024. Regional consumer behavior reflects strong demand for sustainable and high-performance roofing solutions, with 72% of construction companies adopting TPO membranes for compliance with LEED certification standards.

What role do regulation and innovation play in driving market adoption?

Europe commands a 24% share in the global Thermoplastic Polyolefin market, with Germany, the UK, and France leading demand. Germany alone accounted for 38% of Europe’s TPO consumption in 2024, driven by renewable energy projects and sustainable building initiatives. Regulatory pressure, including the EU Green Deal, is fostering adoption of recyclable materials, with over 60% of commercial roofing projects integrating TPO membranes. Technological advancements include AI-driven production monitoring, which has reduced defects by 14% in leading European facilities. Companies such as Sika AG are innovating in high-performance TPO roofing and membrane solutions. Consumer behavior in Europe reflects a high preference for explainable, environmentally friendly products, with over 55% of architects and contractors prioritizing sustainability in material selection.

How are manufacturing trends and consumer demand reshaping the market?

Asia-Pacific represents one of the fastest-growing regions, with a market volume of approximately 1,120 kilotons in 2024. China leads with 42% of regional consumption, followed by Japan (19%) and India (14%). Rapid infrastructure development and expansion in the automotive sector are driving TPO demand. In China, over 65% of new commercial projects adopted TPO roofing in 2024, supported by government incentives for energy-efficient construction. Manufacturing trends include advanced extrusion lines and automation hubs in Japan and South Korea, reducing scrap rates by over 15%. Local players like Zhejiang Huaxia TPO have expanded production capacity by 22% to meet growing demand. Regional consumer behavior reflects strong growth in e-commerce and mobile-based ordering for construction materials, with over 47% of buyers preferring online procurement.

What factors are influencing growth and adoption in the region?

South America accounted for approximately 9% of the global Thermoplastic Polyolefin market in 2024, with Brazil (52%) and Argentina (21%) as leading contributors. Infrastructure expansion, particularly in renewable energy and commercial construction, is driving demand. Brazil’s adoption of TPO roofing in over 40% of large-scale projects in 2024 reflects strong regional growth. Government incentives for sustainable construction and energy efficiency have boosted material adoption. Local players such as Icopal have introduced tailored TPO solutions for tropical climates. Regional consumption is shaped by the need for durable, climate-resistant materials, with 63% of contractors prioritizing products that improve longevity and energy performance. South American buyers are increasingly seeking eco-certified materials aligned with environmental standards.

How are infrastructure and regulatory trends shaping demand?

The Middle East & Africa hold around 6% of the global Thermoplastic Polyolefin market, driven by major growth in the UAE (35%) and South Africa (28%). Strong demand stems from construction projects in energy and infrastructure, including airports and commercial facilities. Governments have implemented policies to encourage sustainable building practices, with over $430 million in incentives allocated for green roofing projects in 2024. Technological modernization, including automated TPO membrane production lines in the UAE, has reduced production costs by 12%. Local players such as Al-Jazeera Roofing Systems have deployed advanced TPO solutions in over 120 projects. Regional consumer behavior shows a growing preference for high-performance materials in luxury commercial construction, with 59% of contractors integrating TPO for durability and sustainability.

United States: Market share of 22% — driven by strong roofing and automotive industry demand and high production capacity.

China: Market share of 19% — led by rapid infrastructure expansion, significant manufacturing investment, and adoption of advanced TPO technologies.

The Thermoplastic Polyolefin (TPO) market is highly competitive and moderately consolidated, with over 120 active global competitors. The top five companies together account for approximately 47% of the total market, underscoring the influence of leading players while leaving significant opportunities for niche and regional providers. Key players are increasingly engaging in strategic initiatives such as product innovation, partnerships, capacity expansions, and mergers to strengthen their positioning. For example, several firms have introduced high-performance TPO membranes with enhanced UV resistance and reflectivity, improving longevity by up to 25%. Technological advancement is a defining competitive trend, with companies adopting AI-enabled quality monitoring, automated extrusion lines, and eco-friendly material formulations. Regional diversification is also a strategy, with firms expanding into Asia-Pacific and the Middle East to tap into growing infrastructure demand. Innovation in sustainable TPO solutions is intensifying competition, as 62% of enterprises prioritize products that meet evolving environmental regulations. Overall, competition is shaped by product differentiation, scale advantages, regulatory compliance, and technological leadership.

Carlisle Construction Materials

Sika AG

Johns Manville

GAF Materials Corporation

Sekisui Chemical Co., Ltd.

Firestone Building Products

CertainTeed Corporation

Garland Company, Inc.

Mule-Hide Products Co., Inc.

IB Roof Systems

The Thermoplastic Polyolefin (TPO) market is witnessing significant technological advancement driven by demand for durability, sustainability, and efficiency. Recent innovations include high-performance TPO membranes with enhanced UV resistance, offering up to 35% greater lifespan compared to earlier-generation materials. Manufacturers are integrating advanced extrusion technologies that enable precise thickness control within ±0.05 mm, ensuring consistent product quality and reducing material waste by up to 18%. Additive manufacturing techniques are also being explored for customized TPO components, enabling tailored solutions for niche industrial applications.

Automation and AI-driven quality control systems are emerging as key trends, allowing real-time defect detection and process optimization. Digital twin technology is being implemented to simulate and optimize TPO manufacturing processes, reducing trial-and-error testing by up to 40%. Sustainable innovation is another major focus, with firms developing TPO formulations containing up to 50% recycled materials while maintaining mechanical performance. Enhanced chemical resistance, improved flexibility at low temperatures (down to -40°C), and reduced installation time are notable advancements impacting adoption across roofing, automotive, and industrial sealing applications. These technologies position the TPO market for accelerated transformation, emphasizing sustainability, operational efficiency, and product innovation.

In March 2023, Carlisle Construction Materials launched a new generation of TPO roofing membranes with integrated solar-reflective granules, improving thermal performance by 27% and extending roof lifespan by up to 15 years. Source: www.carlisleccm.com

In July 2023, Sika AG introduced a hybrid TPO compound for automotive applications, enhancing flexibility by 22% and reducing production cycle time by 14% through advanced extrusion methods. Source: www.sika.com

In January 2024, Johns Manville expanded its manufacturing capacity in North America by 18%, adding state-of-the-art production lines capable of producing TPO sheets with ±0.03 mm thickness tolerance. Source: www.jm.com

In September 2024, Firestone Building Products unveiled an AI-driven inspection system for TPO roofing materials, reducing quality inspection time by 30% and increasing defect detection accuracy by 25%.

The Thermoplastic Polyolefin Market Report covers a comprehensive analysis of the industry, spanning product types, application sectors, end-user industries, and geographic landscapes. It examines key market segments, including roofing membranes, automotive components, industrial sealing solutions, and architectural materials. The report also explores high-growth niche segments such as TPO composites and reinforced membranes designed for specialized environments.

Geographically, the scope includes in-depth insights into the performance of North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, highlighting differences in adoption trends, technological integration, and regulatory influences. Key applications examined include commercial and residential roofing, automotive manufacturing, waterproofing solutions, and industrial sealing, providing a clear picture of sector-specific demand drivers and growth opportunities.

Technological coverage includes emerging manufacturing methods, AI and automation integration, sustainable material innovations, and advanced quality control systems. The report addresses competitive strategies, technological adoption rates, and investment patterns, offering stakeholders actionable insights into the current market environment. Additionally, it identifies future growth pathways, regulatory shifts, and innovation-driven trends shaping the Thermoplastic Polyolefin market landscape, ensuring relevance for decision-makers and industry professionals.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 5635.38 Million |

|

Market Revenue in 2032 |

USD 9187.33 Million |

|

CAGR (2025 - 2032) |

6.3% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Carlisle Construction Materials, Sika AG , Johns Manville, GAF Materials Corporation, Sekisui Chemical Co., Ltd. , Firestone Building Products, CertainTeed Corporation, Garland Company, Inc., Mule-Hide Products Co., Inc., IB Roof Systems |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |