Reports

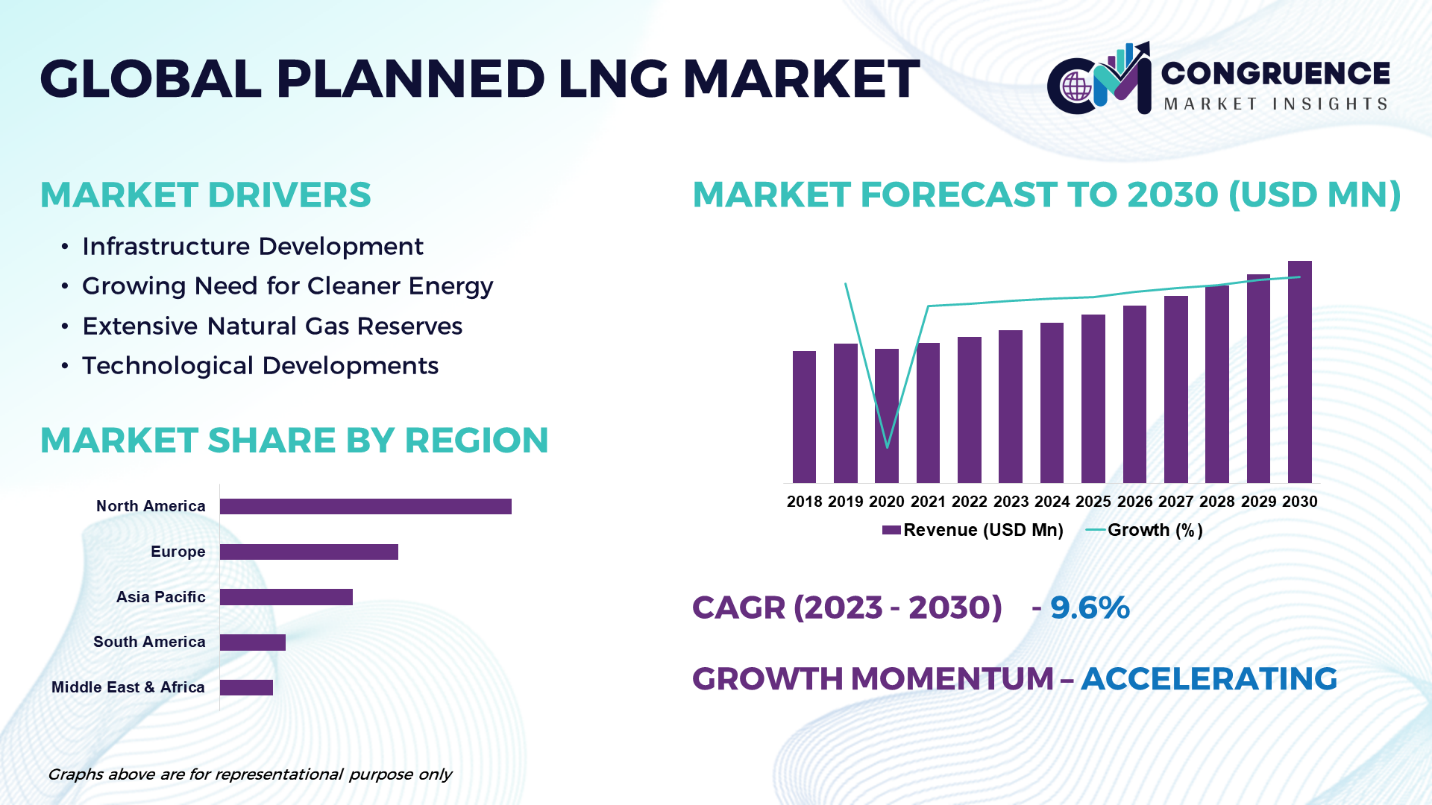

The Global Planned LNG Market is expected to expand at a CAGR of 9.6% between 2023 and 2030. The planned LNG (liquefied natural gas) market is a specialist area of the global energy industry that focuses on the planning, building, and management of new liquefaction projects with the goal of generating LNG for commercial use. LNG is the term for natural gas that has been compressed to extremely low temperatures and transformed into a liquid state for easier transportation and storage. Since, the projected LNG market offers a flexible and energy-efficient means of transporting and trading this key energy source internationally, it is crucial to meeting the world's expanding demand for natural gas. The planned LNG market essentially addresses the requirement of efficiently using natural gas resources by converting them into LNG, which permits long-distance transportation and storage. Liquification facilities, a significant player in the market, chill natural gas to a temperature of approximately -162 degrees Celsius (-260 degrees Fahrenheit), significantly reducing its volume and increasing its suitability for transportation in specialized LNG carriers. The market encompasses a wide range of projects, from expansive facilities with an emphasis on exports to smaller, modular facilities designed for regional distribution and consumption.

Planned LNG Market Major Driving Forces

Infrastructure Development: The construction of LNG infrastructure, including as liquefaction facilities, LNG carriers, and regasification terminals, is making it easier to transport and consume LNG throughout the world. Thanks to this infrastructural development, countries may now import and export LNG, which facilitates access to new energy sources and portfolio diversification.

Growing Need for Cleaner Energy: As a cleaner-burning fuel than coal and oil, LNG is in high demand as the world moves toward greener energy sources to combat climate change and cut carbon emissions. LNG is a dependable and adaptable solution to fulfill expanding energy needs while lessening environmental effect, particularly as governments and companies work to decarbonize their energy mix.

Extensive Natural Gas Reserves: In order to monetize these resources for both domestic and international use, investment in LNG infrastructure is being spurred by the discovery and development of extensive natural gas reserves, mainly in areas such as Australia, the Middle East, and North America. Naturally occurring gas feedstock is plentiful and reasonably priced, giving LNG project development a competitive edge.

Technological Developments: Advances in LNG liquefaction, transportation, and regasification technologies are reducing the entry barriers for the construction of LNG projects, allowing for faster project execution and more flexibility in the planning and execution of projects. The efficiency, safety, and dependability of LNG operations are improved by innovations such increased cargo containment systems, modular liquefaction units, and floating LNG terminals.

Planned LNG Market Key Opportunities

Eco-Friendly and Sustainable solutions: The growing popularity of eco-friendly products offers the anticipated LNG industry a chance to create and advance sustainable solutions. Producers who supply planned LNG with ethical sourcing and production can profit from this trend.

Technological Innovations: Technology developments are causing a steady shift in the planned LNG industry by creating opportunities for more efficient, sustainable, and cost-effective operations. Technological advancements in liquefaction are reducing energy consumption and greenhouse gas emissions while improving LNG production efficiency.

Growing Air Pollution: Vehicles powered by gasoline and diesel are among the main contributors to the rising levels of air pollution, particularly in large cities. It is also to blame for global warming and climate change. Authorities and governments are now looking for more environmentally friendly options, and LNG offers this opportunity.

Planned LNG Market Key Trends

· Increasing interest in LNG as a greener fuel for industrial and power production uses compared to coal and oil.

· Growth in emerging markets and LNG trading routes is propelling infrastructure investment in LNG.

· Technological developments that increase efficiency and reduce costs in LNG liquefaction and regasification.

· Investing more in floating LNG terminals will allow access to distant markets and offshore gas deposits.

· Growth in short-term and spot LNG trading has increased market flexibility and liquidity.

· Move toward LNG projects with a smaller size in order to cater to specialized markets and decentralized energy systems.

· Adoption of LNG as a marine fuel in order to abide by the shipping industry's more stringent emission rules.

· Infrastructure for LNG bunkering is expanding to facilitate the construction of ships that run on LNG.

· Combining LNG infrastructure with renewable energy sources can lower carbon emissions and improve sustainability.

· In reaction to market volatility and geopolitical concerns, emphasize supply chain resilience and risk management.

Market Competition Landscape

The presence of both domestic and foreign competitors defines the competitive landscape of the LNG market that is envisioned. Due to mergers and acquisitions, wherein larger corporations have purchased smaller enterprises in order to enhance their market position and increase their skills, the planned LNG sector has concentrated. Notable businesses with a broad range of goods and services and a global presence have arisen as a result of this trend. Businesses in the projected LNG market are adopting innovative technology at a rapid pace to enhance project efficiency, safety, and environmental sustainability. Companies with a broad geographic reach can access a wider range of markets and opportunities more effectively. By leveraging their local or global presence, they can expand their project portfolio and gain a larger market share. Local and regional pipeline contractors have an advantage over rivals in their specialized marketplaces as they are acquainted with local regulations, cultural peculiarities, and project-specific requirements. Prominent players in the market include:

· Royal Dutch Shell

· Chevron Corporation

· Exxon Mobil Corporation

· Qatar Petroleum

· TotalEnergies

· BP plc

· Gazprom

· Petronas

· Woodside Petroleum

· Santos Ltd.

· Cheniere Energy, Inc.

· Eni S.p.A.

· Novatek

· Equinor ASA

· ConocoPhillips

|

Report Attribute/Metric |

Details |

|

Base Year |

2022 |

|

Forecast Period |

2023 – 2030 |

|

Historical Data |

2018 to 2022 |

|

Forecast Unit |

Value (US$ Mn) |

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Segments Covered |

· By Project Type (Liquefaction Terminals, Regasification Terminals, Floating LNG Facilities) · By Application (Power Generation, Industrial Use, Transportation, Residential) · By End User (Utilities, Industrial, Commercial, Residential) |

|

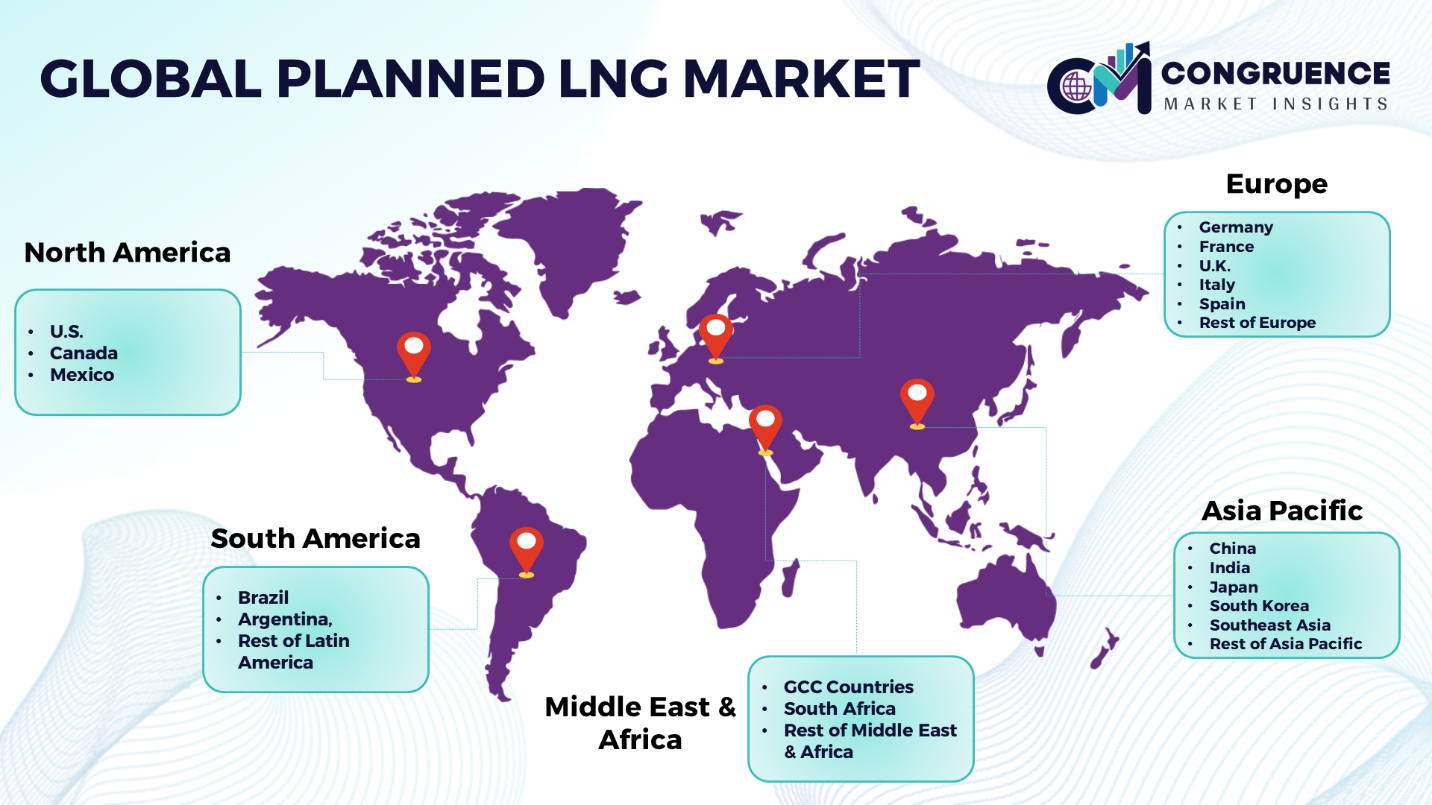

Geographies Covered |

North America: U.S., Canada and Mexico Europe: Germany, France, U.K., Italy, Spain, and Rest of Europe Asia Pacific: China, India, Japan, South Korea, Southeast Asia, and Rest of Asia Pacific South America: Brazil, Argentina, and Rest of Latin America Middle East & Africa: GCC Countries, South Africa, and Rest of Middle East & Africa |

|

Key Players Analyzed |

Royal Dutch Shell, Chevron Corporation, Exxon Mobil Corporation, Qatar Petroleum, TotalEnergies, BP plc, Gazprom, Petronas, Woodside Petroleum, Santos Ltd., Cheniere Energy, Inc., Eni S.p.A., Novatek, Equinor ASA, ConocoPhillips |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |