Reports

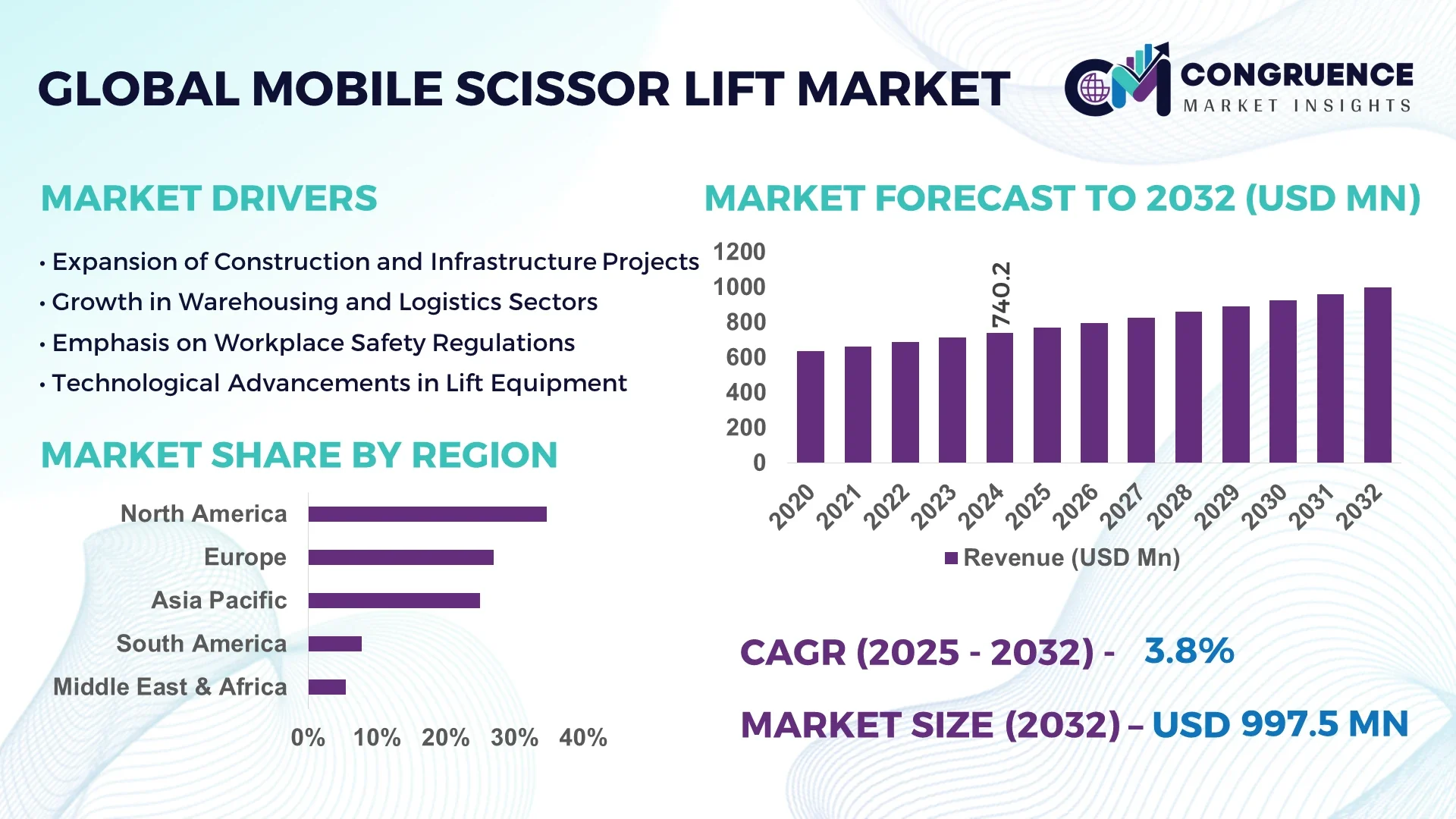

The Global Mobile Scissor Lift Market was valued at USD 740.2 Million in 2024 and is anticipated to reach a value of USD 997.53 Million by 2032 expanding at a CAGR of 3.8% between 2025 and 2032.

The mobile scissor lift market is experiencing steady demand across global industrial zones, primarily driven by its efficiency in vertical lifting solutions across construction, logistics, aviation maintenance, and warehousing. The mobile scissor lift market benefits from rapid infrastructure development in emerging markets and rising automation in developed economies. Increasing government investments in smart city projects and industrial safety compliance standards have further propelled the adoption of mobile scissor lifts. Manufacturers in the mobile scissor lift market are introducing electric-powered and hybrid models to meet growing sustainability standards. Integration of advanced control systems, reduced maintenance, and compact design are encouraging adoption of mobile scissor lifts in both indoor and outdoor operations. The mobile scissor lift market is expanding across North America, Asia-Pacific, Europe, and the Middle East, where mobile scissor lift solutions are prioritized for efficient aerial work platform (AWP) requirements.

AI is transforming the mobile scissor lift market by enhancing safety, efficiency, and operational intelligence. In the mobile scissor lift market, AI-enabled sensors and machine vision technologies are being integrated to monitor weight capacity, platform stability, obstacle detection, and real-time diagnostics. Mobile scissor lifts equipped with AI now offer predictive maintenance features, reducing downtime by up to 30%, ensuring continued operation on industrial sites. AI is optimizing fleet management in the mobile scissor lift market through real-time GPS tracking, usage data analytics, and automated job assignment, helping rental service providers cut operational costs by nearly 20%.

AI-enhanced remote monitoring platforms are increasingly being adopted in the mobile scissor lift market to improve productivity in warehouse and construction settings, allowing operators to make quicker, safer decisions. Integration of AI-powered software is also enabling voice-controlled and semi-autonomous scissor lifts, boosting operator safety. AI applications in the mobile scissor lift market have helped reduce human error-related accidents by 25%, according to industry studies. Furthermore, mobile scissor lift market players are collaborating with AI developers to create adaptive lift controls based on environmental inputs such as terrain, load shifts, and wind conditions. AI is not only optimizing lift deployment but also ensuring compliance with OSHA and ISO safety standards in the mobile scissor lift market.

"In 2024, a major mobile scissor lift manufacturer introduced AI-based predictive maintenance technology. This development allows the lift to autonomously monitor its components and predict necessary maintenance actions, significantly reducing downtime and operational disruptions."

The dynamics of the mobile scissor lift market are influenced by several factors, including technological innovations, rising demand for equipment in construction and warehousing, and the ongoing focus on safety and operational efficiency. With more industries embracing automation and mechanisation, the demand for scissor lifts with advanced features such as AI, predictive analytics, and autonomous functions is growing. These innovations have expanded the scope of mobile scissor lifts beyond traditional industries, including entertainment, retail, and logistics. Additionally, regulatory standards that emphasise safety and operational efficiency have further driven the adoption of these lifts. As construction activities increase globally, particularly in urban areas, the demand for efficient vertical transportation solutions continues to rise. These factors collectively contribute to a favourable market environment for the growth of mobile scissor lifts.

Expansion in construction and infrastructure sectors

The mobile scissor lift market is significantly driven by increasing construction activities and infrastructure projects worldwide. As of 2023, the global construction industry was valued at over USD 10 trillion, with a significant portion of spending allocated to vertical construction projects requiring elevation platforms. In China alone, nearly 25,000 construction sites actively use mobile scissor lifts for multi-level access. In the mobile scissor lift market, the rise of prefabricated and modular construction methods has boosted the requirement for compact, mobile, and safe vertical lifting platforms. The demand for urban redevelopment and smart buildings in the U.S., India, and Germany has further intensified the need for mobile scissor lifts in both commercial and residential projects. Mobile scissor lift sales have surged in logistics parks, retail complexes, and airport expansions, supporting the growing mobile scissor lift market.

High maintenance and battery replacement costs

One major restraint in the mobile scissor lift market is the recurring maintenance expenses and high battery replacement costs. Electric-powered scissor lifts, which constitute over 60% of the mobile scissor lift market, require battery replacements every 2-3 years at an average cost of USD 1,000–1,500 per unit. Hydraulic components also require frequent servicing due to fluid leaks and wear-and-tear issues, increasing operational costs for end users. In rental markets, fleet operators face rising challenges in managing maintenance schedules, leading to increased equipment downtime. The lack of standardized repair services in emerging economies also hampers equipment longevity. Furthermore, users in regions with fluctuating power supplies or extreme weather conditions experience shortened battery life, contributing to reduced customer satisfaction in the mobile scissor lift market.

Electrification and eco-friendly innovations

The mobile scissor lift market is witnessing a surge in opportunities due to the electrification trend and growing focus on zero-emission machinery. Electric and hybrid scissor lifts are gaining traction as companies align operations with ESG goals and emissions regulations. As of 2023, more than 45% of new mobile scissor lift models introduced in Europe and North America featured lithium-ion batteries and noise-reduction systems. Urban environments with noise restrictions are increasingly adopting electric mobile scissor lifts for indoor applications such as mall maintenance, HVAC servicing, and data center installations. Government incentives for adopting electric industrial machinery have further opened opportunities in the mobile scissor lift market, especially across Scandinavian and Western European countries. Manufacturers are investing in green tech R&D, producing lightweight yet durable lift frames using recycled alloys and composites, fostering eco-conscious growth in the mobile scissor lift market.

A pressing challenge in the mobile scissor lift market is the shortage of certified operators and comprehensive training programs. In the U.S., nearly 28% of mobile scissor lift accidents in 2022 were linked to operator error due to lack of training. While advanced models include smart controls and safety automation, a significant portion of workers in emerging economies operate lifts with minimal instruction. Inconsistent training certifications across global regions create safety compliance issues, limiting cross-border equipment leasing. Additionally, language barriers and literacy levels restrict the effectiveness of existing digital training modules. Small and medium enterprises (SMEs) in developing countries often forgo certified training to save costs, resulting in higher injury risks and equipment damage. This training gap restricts adoption and threatens long-term growth of the mobile scissor lift market.

The mobile scissor lift market is undergoing a transformative phase, shaped by trends focused on safety, digitization, automation, and sustainability. One of the most dominant trends in the mobile scissor lift market is the rising demand for compact electric models designed for tight indoor environments, especially in retail, hospitality, and warehouse automation sectors. By 2024, over 55% of newly launched mobile scissor lift units in Europe were electric-powered, prioritizing zero emissions and lower noise levels. The integration of telematics is another major trend, with more than 60% of fleet owners using IoT-based diagnostics for real-time data tracking, fault detection, and predictive maintenance. Manufacturers are focusing on designing foldable, lightweight mobile scissor lift units to enable easy transportation and deployment in remote construction sites.

Another growing trend is the adoption of smart safety systems like auto-braking, load sensing, anti-crush bars, and tilt sensors. In Asia-Pacific, mobile scissor lift adoption in warehousing has grown significantly, fueled by the exponential rise of e-commerce and logistics firms requiring efficient vertical access solutions. The rental model continues to dominate the mobile scissor lift market, with more than 65% of end users preferring short-term equipment leasing over capital purchase. Moreover, digital platforms offering equipment booking and remote usage analytics are emerging as critical enablers of mobile scissor lift market expansion. These trends collectively signify a forward-moving, technologically enhanced mobile scissor lift market designed to meet dynamic global industrial demands.

The mobile scissor lift market is segmented by type, application, and end-user insights, offering comprehensive insights into demand patterns and operational preferences across various industries. Types of mobile scissor lifts cater to specific work environments, including electric, hydraulic, pneumatic, rough terrain, and vertical scissor lifts. Applications vary widely from construction to warehousing, each demanding unique lift capabilities and specifications. End-user insights reveal how different sectors like construction companies and logistics providers are utilizing these lifts to enhance productivity, safety, and operational efficiency. This segmentation provides a detailed understanding of how diverse market demands are shaping product development and strategic deployment within the mobile scissor lift market.

Electric Scissor Lifts: Electric scissor lifts are increasingly popular due to their quiet operation, low emissions, and suitability for indoor use. These lifts are battery-powered and require less maintenance compared to traditional models. In 2024, electric scissor lifts accounted for over 30% of the global mobile scissor lift market share. They are widely used in indoor construction projects, maintenance tasks, and warehousing operations due to their compact design and environmental friendliness. As environmental regulations tighten, especially in urban areas, the demand for electric scissor lifts continues to rise. Additionally, innovations in lithium-ion batteries are improving the performance and runtime of these lifts.

Hydraulic Scissor Lifts: Hydraulic scissor lifts are known for their robust lifting capabilities and durability. These lifts operate using hydraulic fluid pressure, making them ideal for heavy-duty applications such as construction and industrial maintenance. In 2024, hydraulic scissor lifts remained the most used type in developing regions due to their lower initial costs and mechanical simplicity. Despite slower operation speeds and potential for fluid leakage, their reliability in lifting heavy materials makes them indispensable in harsh working environments. Many rental companies continue to invest in hydraulic models due to their broad usability and long service life.

Pneumatic Scissor Lifts: Pneumatic scissor lifts use air pressure instead of hydraulic fluids, making them an environmentally safe alternative. These lifts are especially suitable for industries where cleanliness and zero fluid contamination are critical, such as food processing and electronics manufacturing. Although their market share remains niche, pneumatic scissor lifts are gaining attention for their eco-friendly operation. In 2024, their demand saw modest growth in cleanroom applications and laboratories. Their simple mechanics and reduced maintenance requirements further support their adoption in environments that prioritize hygiene and safety.

Rough Terrain Scissor Lifts: Rough terrain scissor lifts are specifically designed for outdoor use in uneven and rugged environments. These lifts are equipped with four-wheel drive, reinforced tires, and high weight capacities to handle construction, mining, and oil & gas projects. In 2024, rough terrain models represented a significant portion of mobile scissor lift sales in North America and the Middle East. Their strong performance in adverse conditions, combined with growing infrastructure projects worldwide, drives their continued market expansion. These lifts are crucial in locations where standard models cannot safely or efficiently operate.

Vertical Scissor Lifts: Vertical scissor lifts are optimized for narrow spaces and vertical operations, typically used in indoor maintenance and retail environments. These lifts are designed to provide access to ceilings, signage, and lighting in tight locations. In 2024, vertical lifts experienced increasing adoption in commercial buildings and hospitals where maneuverability and safety in restricted areas are essential. Their small footprint, ease of use, and compliance with strict safety regulations make them an attractive option for building maintenance professionals and facility managers.

Construction: Mobile scissor lifts are integral to the construction sector for vertical access during installation, painting, cladding, and electrical work. These lifts are preferred over traditional ladders and scaffolding due to their safety and efficiency. In 2024, over 40% of the mobile scissor lift market demand came from construction applications globally. Their ability to elevate workers and materials at variable heights, combined with their stability, makes them indispensable for both residential and commercial projects. Increased infrastructure spending worldwide continues to drive their adoption in this sector.

Maintenance and Repair: Maintenance and repair tasks in commercial, industrial, and institutional facilities require reliable vertical access tools. Mobile scissor lifts offer a safe and efficient solution for tasks such as HVAC servicing, electrical work, and facility inspections. In 2024, maintenance and repair applications held a notable share in developed economies due to the aging infrastructure and increasing facility maintenance budgets. These lifts allow technicians to reach high ceilings and roof spaces with stability and precision, improving task completion times and reducing workplace accidents.

Warehousing and Inventory Management: In warehousing and logistics environments, mobile scissor lifts are used for stocking, inventory checks, and shelf maintenance. These lifts enhance efficiency by enabling quick and safe access to high-storage areas. With the growth of e-commerce and global supply chains, warehouses are scaling vertically, increasing demand for vertical access equipment. In 2024, warehousing applications contributed significantly to market demand in North America, Europe, and Asia-Pacific. The need for fast, safe, and ergonomic access in high-density storage facilities is a major driver in this segment.

Event Setup and Staging: Event management companies utilize mobile scissor lifts for stage setup, lighting rigging, and sound equipment installation. These lifts provide safe elevation for technicians working at height during concerts, exhibitions, and corporate events. In 2024, mobile scissor lifts saw increased demand in the entertainment sector due to the resurgence of live events post-pandemic. Their compact size, ease of transport, and ability to quickly raise heavy equipment make them a vital tool for event organizers worldwide.

Industrial and Manufacturing: Manufacturing plants and industrial facilities rely on mobile scissor lifts for equipment installation, routine maintenance, and overhead repairs. These environments often require robust lifting equipment that can operate in confined spaces. In 2024, mobile scissor lifts were commonly used in automotive, electronics, and heavy machinery manufacturing plants. The need for reducing downtime and ensuring employee safety during elevated operations continues to drive demand in this application segment. Their versatility and load-bearing capabilities make them suitable for a wide range of industrial tasks.

Construction Companies: Construction companies are the largest end-users of mobile scissor lifts due to their constant need for height-access equipment on project sites. These companies prioritize equipment that enhances safety, reduces manual labor, and increases work efficiency. In 2024, construction firms accounted for the majority of scissor lift rentals and purchases globally. The trend of adopting automated and AI-integrated equipment in modern construction sites has further boosted demand. Additionally, government investments in public infrastructure projects worldwide are driving adoption among small and large construction enterprises alike.

Logistics and Warehousing Providers: Logistics and warehousing providers are increasingly adopting mobile scissor lifts to support vertical storage systems and streamline inventory operations. These organizations require lifts that are energy-efficient, maneuverable, and capable of operating in narrow aisles. In 2024, the rise in demand for last-mile delivery services and global e-commerce led to a spike in mobile scissor lift usage across logistics centers and distribution hubs. Providers seek lifts with advanced safety features, real-time tracking, and low maintenance requirements, making modern scissor lifts an essential part of their warehouse automation strategy.

North America accounted for the largest market share at 34.7% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.9% between 2025 and 2032.

North America's dominance is attributed to high demand from construction, warehousing, and manufacturing sectors, along with strong safety regulations and a mature rental ecosystem. In contrast, Asia-Pacific’s rapid urbanization, infrastructure projects in India, China, and Southeast Asia, and a surge in e-commerce warehousing are propelling fast market expansion. Europe follows with a 27.1% share, driven by automation in industrial processes and green equipment adoption. Meanwhile, the Middle East & Africa region is emerging due to smart city initiatives and increasing construction investments in the UAE and Saudi Arabia. Latin America also presents moderate growth opportunities led by Brazil and Mexico’s commercial infrastructure development. Regionally, market dynamics vary considerably, with developed markets leaning towards electrification and developing markets focusing on equipment affordability and durability.

Robust Infrastructure Push in North America Fuels Market Demand

In 2024, North America captured the largest share in the global mobile scissor lift market at 34.7%, driven by significant investments in construction, commercial real estate, and industrial facility upgrades. The United States dominates the regional demand due to its robust construction pipeline, extensive warehouse networks, and established rental fleet operators. Over 70% of scissor lift sales in North America are through rental companies, reflecting high equipment turnover and demand flexibility. Additionally, strict OSHA (Occupational Safety and Health Administration) regulations have led to widespread adoption of scissor lifts over traditional ladders for elevated work. Canada is also seeing increased demand, especially in infrastructure renovations and logistics expansion. The growing shift toward electric and hybrid scissor lifts due to environmental considerations further enhances growth prospects. North America's preference for advanced safety features and automation-integrated platforms distinguishes it as a technologically mature market in this segment.

Green Equipment Adoption Drives European Market Penetration

Europe maintained a 27.1% share of the mobile scissor lift market in 2024, reflecting consistent demand from construction, maintenance, and warehousing operations across countries such as Germany, the UK, France, and Italy. The European market is characterized by strong regulatory frameworks emphasizing worker safety and environmental sustainability. Germany leads in unit sales due to its robust manufacturing sector and ongoing infrastructure modernization. The adoption of electric scissor lifts is notably high in Europe, supported by policies restricting diesel-powered machinery in urban zones. The UK and France have also seen increasing deployment of scissor lifts in retail and airport maintenance. Manufacturers are responding by introducing low-noise, zero-emission lifts to meet strict EU emission standards. Furthermore, the growing trend of leasing and equipment-as-a-service models is fueling wider adoption, especially among small-to-mid-size enterprises looking for cost-effective solutions without long-term ownership.

Asia-Pacific Emerges as Fastest Growing Market with Urbanization and Logistics Surge

The Asia-Pacific region is witnessing rapid acceleration in mobile scissor lift adoption, led by infrastructural expansion, e-commerce logistics, and industrial automation. In 2024, the region held a 22.3% market share, with China, India, Japan, and Southeast Asia driving growth. China's Belt and Road Initiative and smart city projects have significantly boosted construction equipment demand. India is experiencing a surge in logistics warehousing due to increased foreign investment in retail and e-commerce sectors, prompting the use of mobile scissor lifts for vertical storage management. Japan and South Korea emphasize compact and electric models suited for urban infrastructure maintenance. The increase in labor safety regulations across ASEAN countries is also promoting scissor lift usage in factory setups. As manufacturers expand regional production hubs and supply chains decentralize, Asia-Pacific is poised to outpace other regions in new unit sales. Government incentives for electric industrial vehicles further encourage the transition to cleaner lift technologies.

Infrastructure Projects and Mega-Events Spur Middle East & Africa Market Activity

The Middle East & Africa mobile scissor lift market is gaining momentum, particularly in Gulf Cooperation Council (GCC) countries. In 2024, the region contributed a 10.4% share to the global market, led by construction mega-projects in Saudi Arabia (NEOM), the UAE (Expo legacy developments), and Qatar. Governments are investing heavily in commercial infrastructure, tourism, and smart cities, creating robust demand for vertical access equipment. The adoption of mobile scissor lifts in these regions is driven by labor safety requirements and the need for efficient material handling on-site. South Africa and Nigeria are also seeing incremental growth in warehousing and telecom infrastructure, where scissor lifts are used for equipment installation. Rental penetration remains moderate, but the region is witnessing increased imports of rough terrain and electric scissor lifts, tailored to the varying site conditions and power availability across urban and remote project locations.

The global mobile scissor lift market is highly competitive, with established manufacturers and regional players striving for technological advancement, geographic expansion, and service enhancement. Companies are focusing on product innovation, such as incorporating IoT-enabled monitoring systems, self-diagnostics, and electric or hybrid drive systems to meet changing customer demands. As of 2024, rental channels accounted for over 65% of global scissor lift transactions, prompting OEMs to partner closely with rental companies to ensure faster deployment and after-sales support. North America and Europe remain saturated with well-known brands competing on durability and operator safety features, while emerging markets offer potential through affordable product lines and local manufacturing. Joint ventures, facility expansions, and M&A activities have intensified as manufacturers seek stronger distribution networks and after-market service coverage. Competition is also marked by the integration of automation and remote-controlled platforms designed for smart warehouses and construction monitoring. Key players are now integrating safety interlocks, fall detection systems, and energy-efficient powertrains to remain competitive.

JLG Industries, Inc.

Haulotte Group

Skyjack (a Linamar Company)

MEC Aerial Work Platforms

Aichi Corporation

Sinoboom Intelligent Equipment Co., Ltd.

Zhejiang Dingli Machinery Co., Ltd.

Holland Lift International B.V.

Snorkel International

Palazzani Industrie S.p.A.

ELS Lift

Manitou Group

The mobile scissor lift market is rapidly evolving due to emerging technologies focused on improving safety, energy efficiency, and operational performance. Mobile scissor lift manufacturers are investing heavily in smart features and electric-driven mechanisms to gain a competitive edge. Mobile scissor lift technology has seen increasing demand for electric scissor lifts, especially in urban and indoor applications where zero emissions and silent operation are essential. In 2023, electric scissor lifts held more than 68% of the global scissor lift market share, indicating a rising preference for sustainable alternatives over diesel or gas-powered machines.

Integration of telematics and IoT sensors into mobile scissor lifts enables fleet operators to track usage, monitor maintenance schedules, and optimize deployment. Predictive maintenance and automated diagnostics are reducing downtime by up to 25%, significantly improving productivity. Safety enhancements like tilt alarms, overload detection, and proximity sensors are now standard in premium models. Furthermore, hybrid scissor lifts are gaining popularity due to their dual power source capability, offering flexibility in mixed-use environments. In terms of materials, companies like LAPP are introducing bio-based cables to reduce environmental impact. Overall, mobile scissor lift technology continues to move toward automation, sustainability, and intelligence-driven systems.

In June 2024, LAPP introduced the ETHERLINE® FD bioP Cat.5e, its first bio-based Ethernet cable produced in series. This sustainable variant features a bio-based outer sheath composed of 43% renewable raw materials, reducing the carbon footprint by 24% compared to traditional fossil-based TPU sheaths.

In February 2024, JLG launched the ES4046 Electric Scissor Lift, designed with a zero turning radius and 50% more duty cycle than earlier models. This innovation allows better maneuverability in confined spaces and extends operational hours on a single charge.

In November 2023, Genie upgraded its slab scissor lift range with new lithium-ion battery packs, delivering 25% longer operational uptime and reduced energy costs. The battery system was optimized for high-cycle usage in rental operations.

In July 2023, Haulotte announced its new OPTIMUM 8 electric scissor lift with an auto-diagnostics interface that reduces service time by up to 30%. The model also integrates advanced proportional controls for smoother operator experience.

In March 2023, Skyjack enhanced its telematics capabilities with ELEVATE Live, a feature allowing real-time machine data to be accessed directly via QR codes. This move improved fleet transparency and customer support for rental companies.

The scope of the Mobile Scissor Lift Market Report covers a comprehensive evaluation of the industry’s current conditions and future projections across the globe. The report examines critical factors influencing market growth such as type differentiation (electric, hydraulic, pneumatic), rising demand in warehousing and construction, and end-user behavior across industries. It includes detailed segmentation analysis by type, application, and end-user insights, offering a complete overview of how different sectors are contributing to the market dynamics.

The Mobile Scissor Lift Market Report further explores regional demand, identifying North America as the dominant contributor in 2024 and projecting Asia-Pacific to exhibit the highest growth between 2025 and 2032. It provides in-depth coverage of ongoing technological innovations, including battery advancements, AI integration, telematics, and eco-friendly components, that are reshaping the competitive landscape.

The report outlines key players in the mobile scissor lift market, their product portfolios, strategic partnerships, acquisitions, and expansion initiatives. It addresses market drivers, restraints, opportunities, and challenges, offering a 360-degree view of the competitive dynamics and demand-supply trends. This makes the report a strategic tool for investors, manufacturers, policymakers, and stakeholders aiming to capitalize on the future of the mobile scissor lift market.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 740.2 Million |

|

Market Revenue in 2032 |

USD 997.53 Million |

|

CAGR (2025 - 2032) |

3.8% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

JLG Industries, Inc., Haulotte Group, Skyjack (a Linamar Company), MEC Aerial Work Platforms, Aichi Corporation, Sinoboom Intelligent Equipment Co., Ltd., Zhejiang Dingli Machinery Co., Ltd., Holland Lift International B.V., Snorkel International, Palazzani Industrie S.p.A., ELS Lift, Manitou Group 4o |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |