Reports

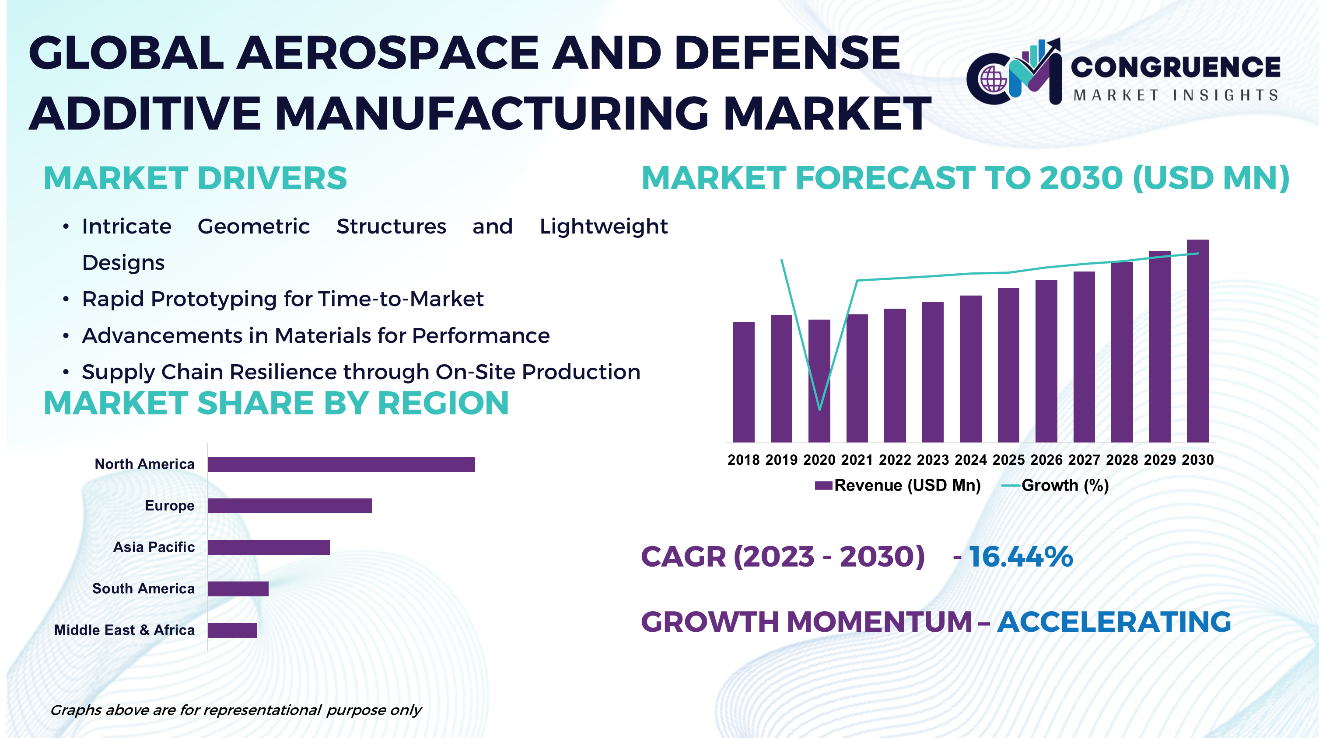

The Aerospace and Defense Additive Manufacturing sector has significantly impacted aerospace and defense industries through additive manufacturing, commonly known as 3D printing. This dynamic field utilizes a layer-by-layer approach for intricate component creation, providing unmatched design flexibility and rapid prototyping capabilities. Crucial technological advancements within this market include progress in materials, processes, and scalability, incorporating high-performance alloys, composite materials, and innovative printing techniques to enhance part strength, durability, and intricacy. The industry landscape underscores a robust sector increasingly relying on additive manufacturing for critical applications. Aerospace and defense organizations embrace this technology for lightweight component production, supply chain optimization, and reduced lead times. Key contributors to innovation drive the market, emphasizing the industry's evolution towards the direct production of end-use components, representing the transformative impact of aerospace and defense additive manufacturing on manufacturing processes. The Global Aerospace and Defense Additive Manufacturing Market is expected to expand at a CAGR of 16.44% between 2023 and 2030.

Aerospace and Defense Additive Manufacturing Market Major Driving Forces

Intricate Geometric Structures and Lightweight Designs: Additive manufacturing facilitates the development of aerospace components with intricate geometric structures and lightweight designs, enhancing efficiency and structural integrity.

Rapid Prototyping for Time-to-Market: Additive manufacturing accelerates product development with rapid prototyping, enabling faster design iterations and reducing time-to-market for new aerospace and defense products.

Advancements in Materials for Performance: Ongoing advancements in materials, such as high-performance alloys and composites, bolster the strength, durability, and overall performance of aerospace components.

Supply Chain Resilience through On-Site Production: The technology's capability to produce components on-site or in proximity enhances supply chain resilience, reducing dependence on centralized manufacturing facilities.

Aerospace and Defense Additive Manufacturing Market Key Opportunities

Scaling Production: The market can capitalize on opportunities to scale up additive manufacturing production capabilities, meeting the increasing demand for lightweight, complex components in the aerospace and defense industries.

Supply Chain Optimization: Opportunities exist for integrating additive manufacturing into supply chain strategies, reducing lead times, and optimizing the production and distribution of critical aerospace components.

In-Flight Repairs and Maintenance: Additive manufacturing offers opportunities for on-demand, in-flight repairs and maintenance of aerospace components, enhancing operational flexibility and reducing downtime.

Aerospace and Defense Additive Manufacturing Market Key Trends

· Growing trend in adopting metal additive manufacturing for critical aerospace components, driven by advancements in metal 3D printing technologies.

· Industry shift towards large-scale additive manufacturing for aerospace components, aiming to leverage additive manufacturing benefits while addressing size and scalability challenges.

· Increasing adoption of hybrid manufacturing, combining additive and subtractive processes, optimizing material usage and enhancing overall component performance.

· Continuous development of high-performance materials, including advanced alloys and composites, enhancing strength, durability, and functionality of aerospace components.

· Utilization of additive manufacturing for in-service maintenance and repairs, enabling on-demand production of replacement parts, reducing downtime, and improving operational efficiency.

· Trend towards standardized certification processes as additive manufacturing becomes prevalent in aerospace and defense, ensuring compliance with safety and quality standards.

· Increasing role of AI and ML in optimizing additive manufacturing processes, contributing to improved design, process control, and quality assurance for aerospace components.

Market Competition Landscape

In the Aerospace and Defense Additive Manufacturing Market, intense competition prevails, marked by a focus on innovation and technological progress. Market contenders vie for leadership, emphasizing scalable production, optimal material usage, and sustainable practices. The industry landscape reflects a trend towards large-scale manufacturing and the integration of hybrid processes, combining additive and subtractive methods. The competitive dynamics are further defined by a strong emphasis on high-performance materials and environmental consciousness. Collaborations among industry participants and the incorporation of artificial intelligence contribute to shaping a competitive arena poised for continuous evolution and advancements in aerospace and defense additive manufacturing.

Key players in the global Aerospace and Defense Additive Manufacturing market implement various organic and inorganic strategies to strengthen and improve their market positioning. Prominent players in the market include:

· Sintavia, LLC

· ENVISIONTEC US LLC

· 3D Systems, Inc.

· EOS

· ExOne

· GE Additive

· Höganäs AB

· Optomec, Inc.

· Prodways

· Renishaw plc.

· SLM Solutions

· Stratasys Ltd.

· UltiMaker

|

Report Attribute/Metric |

Details |

|

Base Year |

2022 |

|

Forecast Period |

2023 – 2030 |

|

Historical Data |

2018 to 2022 |

|

Forecast Unit |

Value (US$ Mn) |

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Segments Covered |

· By Material Type (Polymer, Metal Alloys, and Ceramics) · By Technology (Powder Bed Fusion (PBF), Direct Energy Deposition (DED), and Material Extrusion) · By End Use (Commercial Aircraft, Military Aircraft, and Spacecraft) · By Sales Channel (Independent Small Stores, Specialty Stores, Online Retailing, and Others) |

|

Geographies Covered |

North America: U.S., Canada and Mexico Europe: Germany, France, U.K., Italy, Spain, and Rest of Europe Asia Pacific: China, India, Japan, South Korea, Southeast Asia, and Rest of Asia Pacific South America: Brazil, Argentina, and Rest of Latin America Middle East & Africa: GCC Countries, South Africa, and Rest of Middle East & Africa |

|

Key Players Analyzed |

Sintavia, LLC, ENVISIONTEC US LLC, 3D Systems, Inc., EOS, ExOne, GE Additive, Höganäs AB, Optomec, Inc., Prodways, Renishaw plc., SLM Solutions, Stratasys Ltd., and UltiMaker |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |