Reports

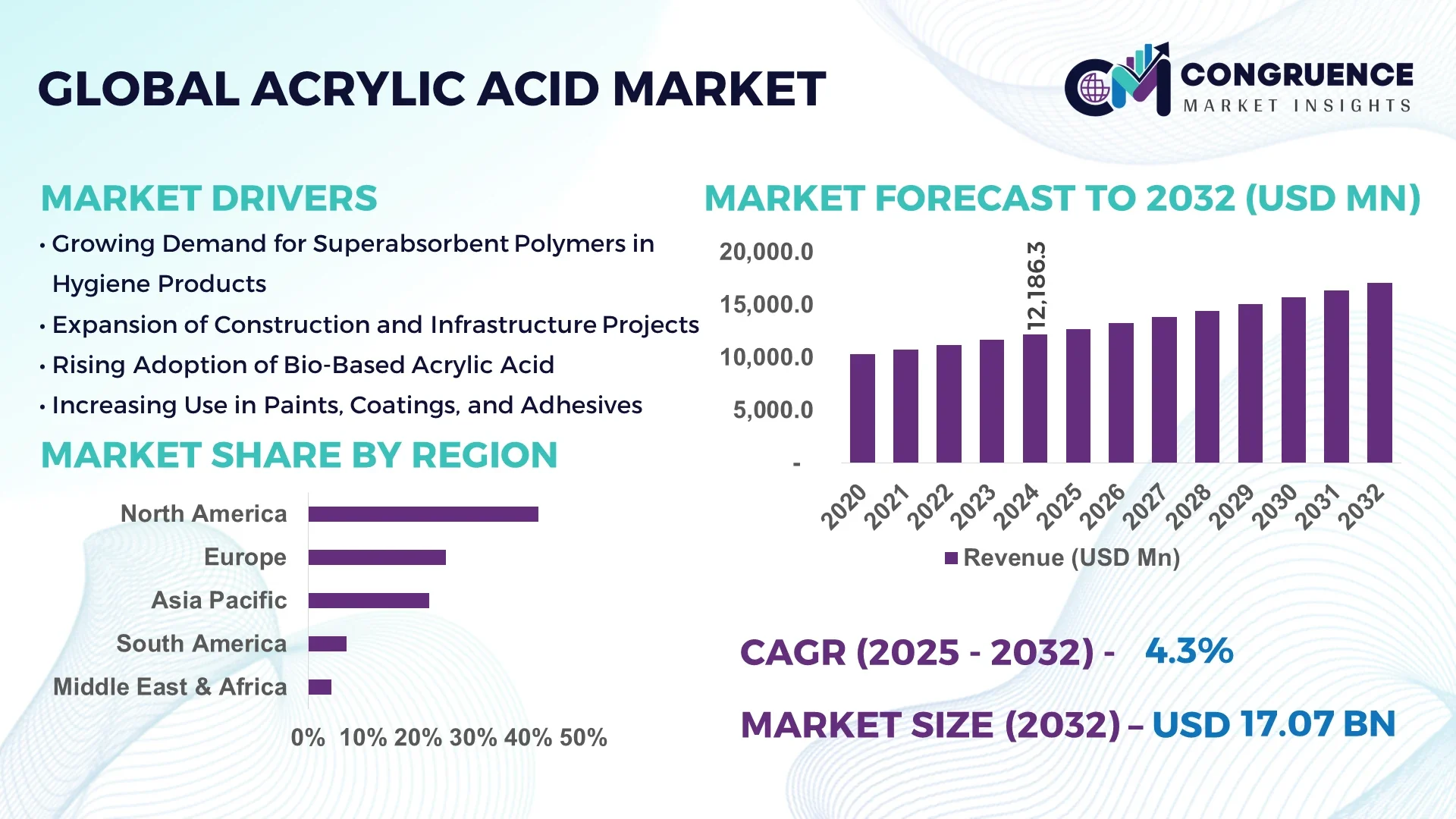

The Global Acrylic Acid Market was valued at USD 12,186.30 Million in 2024 and is anticipated to reach a value of USD 17,066.6 Million by 2032 expanding at a CAGR of 4.3% between 2025 and 2032.

Acrylic acid, a key raw material in the production of superabsorbent polymers and acrylate esters, plays a vital role across industries such as personal care, construction, and textiles. The demand for diapers, adult incontinence products, and feminine hygiene products is significantly boosting consumption of acrylic acid derivatives. In developing economies, increasing urbanization, improving sanitation infrastructure, and growing population are enhancing the market potential. Countries like China and India are emerging as major manufacturing hubs, contributing to high-volume production and regional self-sufficiency in acrylic acid. Innovations in eco-friendly bio-acrylic acid production are creating new growth avenues and are expected to reduce dependency on petroleum-based feedstocks, making the acrylic acid market more sustainable and competitive globally.

Artificial intelligence is transforming the acrylic acid market by enhancing operational efficiency, predictive maintenance, and process optimization across manufacturing units. AI-driven algorithms are being used to monitor reactor conditions and optimize reaction pathways for improved yield and safety. Machine learning models help predict demand fluctuations, optimize raw material procurement, and reduce energy consumption. Advanced data analytics supported by AI are providing insights into production bottlenecks, helping manufacturers adapt more rapidly to changes in market demand or raw material costs.

Furthermore, AI integration in supply chain management is significantly reducing downtime and logistics-related inefficiencies. For example, predictive analytics are being used to determine the optimal distribution channels for acrylic acid and its derivatives, resulting in faster delivery and reduced inventory costs. AI-powered R&D tools are also accelerating the development of new acrylic acid formulations that are safer, cheaper, and environmentally friendlier. These transformations are improving overall product quality and sustainability, giving companies a strong competitive advantage in the acrylic acid market.

In March 2024, BASF adopted AI-driven modeling to enhance the efficiency of its acrylic acid production plants, resulting in a 15% reduction in energy use per ton of product manufactured.

One of the major growth drivers for the acrylic acid market is the increasing demand for superabsorbent polymers (SAPs), primarily used in personal hygiene products. The growing population of infants and aging individuals globally is accelerating the need for diapers and adult incontinence products. For instance, over 175 billion diapers were sold globally in 2023, with SAPs being a primary component. Acrylic acid is the key precursor for SAPs, and this correlation continues to fuel demand across regions. Asia Pacific alone witnessed a sharp rise in SAP consumption due to improved living standards and hygiene awareness. Acrylic acid is also used in agricultural water retention agents and medical pads, further expanding its application base.

Stringent environmental regulations regarding emissions and exposure risks associated with acrylic acid production pose a significant restraint. Acrylic acid is known to be toxic in high concentrations, and emissions during its manufacture can contribute to air and water pollution if not properly managed. Regulatory bodies in the EU and the U.S. have imposed strict safety and disposal guidelines. This increases operational costs for companies and can deter smaller firms from entering the market. Furthermore, local community opposition to chemical plant expansions due to environmental concerns is another limiting factor for the global acrylic acid industry.

There is a growing opportunity in developing bio-based acrylic acid as industries shift towards more sustainable production. Companies like Cargill and BASF are investing heavily in renewable feedstocks such as glycerol derived from biomass. These alternatives not only reduce reliance on fossil fuels but also offer a more environmentally friendly solution that aligns with global climate goals. Bio-based acrylic acid opens the door for low-carbon, biodegradable hygiene and personal care products. The market demand for sustainable chemicals is rising rapidly, and bio-acrylics are expected to capture a sizable portion of the future demand, especially in eco-sensitive regions such as Europe and North America.

Fluctuating prices of key raw materials like propylene present a major challenge to acrylic acid manufacturers. Propylene, derived from petroleum refining, is sensitive to changes in crude oil prices and global supply chain dynamics. The recent geopolitical disruptions and energy market uncertainties have led to sharp increases in propylene prices, directly affecting the profitability of acrylic acid producers. Additionally, inconsistent supply and logistical issues further aggravate this challenge. To remain competitive, manufacturers must explore long-term supply contracts, invest in feedstock diversification, or explore alternative bio-based sources to ensure stability in production.

The acrylic acid market is witnessing significant transformations driven by evolving consumer demands and technological advancements. One of the primary trends is the increasing adoption of bio-based acrylic acid, propelled by stringent environmental regulations and a global shift towards sustainable products. Companies are investing in research and development to produce acrylic acid from renewable sources like glycerol, aiming to reduce carbon footprints and dependence on fossil fuels.

Another notable trend is the surge in demand for superabsorbent polymers (SAPs), especially in the personal care sector. The rising awareness about hygiene and the growing aging population have led to an uptick in the consumption of diapers and adult incontinence products, thereby boosting the SAP market. Additionally, the construction industry is expanding rapidly, particularly in emerging economies, leading to increased use of acrylic acid in paints, coatings, adhesives, and sealants.

Technological advancements are also playing a pivotal role. Innovations in production processes are enhancing efficiency and reducing costs, making acrylic acid more accessible for various applications. Furthermore, the integration of digital technologies and automation in manufacturing is streamlining operations and improving product quality.

In summary, the acrylic acid market is evolving with a focus on sustainability, increased demand in personal care and construction sectors, and technological innovations enhancing production and application efficiency.

The acrylic acid market is segmented based on type, application, and end-user, each playing a crucial role in the industry's dynamics. By type, the market is divided into glacial acrylic acid and crude acrylic acid, each serving distinct applications. Glacial acrylic acid is primarily used in the production of superabsorbent polymers, while crude acrylic acid is utilized in the manufacturing of acrylate esters.

In terms of application, acrylic acid finds extensive use in the production of acrylate esters, superabsorbent polymers, coatings, adhesives, and sealants. Acrylate esters are vital in the paints and coatings industry, providing properties like durability and resistance. Superabsorbent polymers are essential in personal care products, offering high absorbency.

Regarding end-users, the personal care industry is a significant consumer of acrylic acid, driven by the demand for hygiene products. The construction sector utilizes acrylic acid in various applications, including adhesives and coatings. The textile industry also employs acrylic acid derivatives for fabric treatments and finishes.

Glacial Acrylic Acid

Glacial acrylic acid is a highly purified form of acrylic acid, known for its clarity and low impurity levels. It is predominantly used in the production of superabsorbent polymers (SAPs), which are integral to personal hygiene products like diapers and sanitary napkins. The demand for glacial acrylic acid is rising in tandem with the growing awareness of hygiene and the increasing aging population. Its applications extend to the manufacturing of water treatment chemicals, textiles, and coatings, where high purity is essential.

Crude Acrylic Acid

Crude acrylic acid, containing higher levels of impurities, is primarily utilized in the production of acrylate esters. These esters are essential components in the formulation of paints, coatings, adhesives, and sealants. The construction and automotive industries are significant consumers of products derived from crude acrylic acid, owing to its cost-effectiveness and suitability for large-scale industrial applications. The versatility of crude acrylic acid makes it a staple in various manufacturing processes.

Acrylate Esters

Acrylate esters, synthesized from acrylic acid, are vital in producing paints, coatings, adhesives, and sealants. Their properties, such as flexibility, durability, and resistance to environmental factors, make them indispensable in the construction and automotive industries. The demand for acrylate esters is bolstered by the growth in infrastructure projects and the need for high-performance materials in various applications. Their role in enhancing product longevity and performance is crucial across multiple sectors.

Superabsorbent Polymers (SAPs)

Superabsorbent polymers, derived from acrylic acid, are primarily used in personal care products due to their exceptional absorbency. They are key components in diapers, adult incontinence products, and feminine hygiene items. The rising global population, increased awareness of hygiene, and the aging demographic are driving the demand for SAPs. Their ability to retain large volumes of liquid relative to their mass makes them essential in products requiring high absorbency.

Coatings

Acrylic acid-based coatings are widely used in the construction and automotive industries. They provide protective layers that enhance durability, resistance to environmental factors, and aesthetic appeal. The demand for such coatings is increasing with the growth of infrastructure projects and the automotive sector's expansion. Their application ensures longevity and performance of surfaces exposed to various conditions.

Adhesives & Sealants

Acrylic acid derivatives are crucial in formulating adhesives and sealants used across industries. Their strong bonding properties, flexibility, and resistance to environmental stressors make them suitable for construction, automotive, and packaging applications. The increasing demand for durable and efficient bonding solutions in various sectors is propelling the growth of this application segment.

Personal Care

The personal care industry is a significant consumer of acrylic acid, primarily for producing superabsorbent polymers used in hygiene products like diapers and sanitary napkins. The growing awareness of personal hygiene, coupled with an increasing aging population, is driving the demand in this sector. Innovations in product design and functionality are further enhancing the use of acrylic acid derivatives in personal care applications.

Construction

In the construction industry, acrylic acid is utilized in manufacturing adhesives, sealants, and coatings. These products are essential for ensuring structural integrity, durability, and aesthetic appeal in buildings and infrastructure projects.

Textiles

The textile industry represents a crucial end-user of acrylic acid, primarily due to its applications in superabsorbent polymers, binders, and thickeners used in fiber processing and textile coatings. Acrylic acid-based copolymers are extensively utilized in producing finishes that enhance fabric durability, water resistance, and softness.

Automotive

In the automotive industry, acrylic acid plays a pivotal role in manufacturing pressure-sensitive adhesives, sealants, and coatings used for interiors, exteriors, and under-the-hood applications. Its chemical derivatives, such as acrylate resins, contribute to lightweight, corrosion-resistant, and UV-stable parts.

Asia-Pacific accounted for the largest market share at 38% in 2024; however, North America is expected to register the fastest growth, expanding at a CAGR of 4.3% between 2025 and 2032.

The Asia-Pacific region's dominance is primarily driven by China's substantial production and consumption of acrylic acid, contributing over 50% to the regional demand. India is emerging as a significant market, with its acrylic acid demand projected to grow at a CAGR of 10.9%, reaching 408 kilotons by 2032. In North America, the presence of major manufacturers like Dow Chemicals and Arkema, coupled with a favorable business environment and easy availability of feedstock, is fueling market growth. The U.S. leads the region, with substantial investments in capacity expansions to meet the rising demand from end-use industries such as coatings, sealants, and adhesives. Europe holds a considerable market share, driven by the construction industry's expansion and the increasing demand for paints and coatings. The Middle East & Africa region is witnessing steady growth, supported by infrastructural developments and rising demand for superabsorbent polymers in hygiene products.

North America's acrylic acid market is characterized by a strong industrial base and continuous innovation. The U.S. dominates the region, with a market value projected to reach $2,425 million by 2030. The construction boom in Canada has led to increased demand for acrylic-based coatings, with building construction investments rising by 5.3% to $18.9 billion in September 2023. The U.S. textile industry, investing $20.9 billion in new plants and equipment from 2012 to 2021, contributes significantly to the demand for acrylic acid as binders and thickeners. Mexico is also witnessing growth, with a projected CAGR of 5% during 2023–2030. The region benefits from the presence of leading acrylic acid companies and a favorable business environment that encourages capacity expansions and technological advancements.

Europe's acrylic acid market is experiencing growth driven by sustainable practices and robust construction activities. The region's demand for paints and coatings is rising, particularly in the UK, Germany, and France, due to rapid construction industry expansion. BASF's initiative to double its water-soluble acrylic acid dispersant production capacity at its Dilovasi, Turkey facility, aims to support customers in the cleaning, disinfection, and chemical processing industries. The European market is also focusing on bio-based alternatives, aligning with stringent environmental regulations. These developments, coupled with technological innovations, are enhancing the region's position in the global acrylic acid market.

Asia-Pacific stands as the largest and fastest-growing acrylic acid market, accounting for over 60% of global capacity. China leads the region, with a projected market value of $1,954.4 million by 2030. India's acrylic acid demand is forecasted to grow at a CAGR of 10.9%, reaching 408 kilotons by 2032, driven by new capacity additions and increasing consumption in personal care and construction sectors. Japan and South Korea also contribute significantly, with Japan accounting for over 14% and South Korea for 12% of the regional production capacity. The region's growth is further supported by rising living standards, increased purchasing power, and infrastructural developments.

The Middle East & Africa acrylic acid market is witnessing steady growth, supported by infrastructural developments and rising demand for superabsorbent polymers in hygiene products. The region's focus on improving living standards and increasing awareness of personal hygiene is driving the consumption of acrylic acid-based products. Countries are investing in construction and industrial projects, which, in turn, boost the demand for paints, coatings, adhesives, and sealants. The market is also exploring opportunities in water treatment and textiles, leveraging acrylic acid's properties to meet the region's specific needs. These factors collectively contribute to the region's growing presence in the global acrylic acid market.

The global acrylic acid market is characterized by intense competition among key players striving to enhance their market presence through strategic initiatives. Major companies such as BASF SE, Arkema S.A., Dow Chemical Company, LG Chem Ltd., and Nippon Shokubai Co., Ltd. dominate the market, leveraging their extensive product portfolios and global distribution networks. These companies are focusing on expanding their production capacities to meet the growing demand for acrylic acid derivatives, particularly in the Asia-Pacific region. For instance, BASF SE announced the expansion of its acrylic acid production facility in Ludwigshafen, Germany, to cater to the rising demand for hygiene products. Similarly, Nippon Shokubai Co., Ltd. invested in new production lines to increase its manufacturing capacity in Southeast Asia. The market also witnesses participation from regional players like Shanghai Huayi Acrylic Acid Co., Ltd. and Zhejiang Satellite Petrochemical Co., Ltd., who are enhancing their competitiveness through technological advancements and strategic collaborations. The competitive landscape is further influenced by the increasing emphasis on sustainable and bio-based acrylic acid production, prompting companies to invest in research and development activities to innovate eco-friendly solutions. Overall, the market's competitive dynamics are shaped by capacity expansions, technological innovations, and strategic partnerships aimed at meeting the evolving consumer demands and regulatory requirements.

BASF SE

Arkema S.A.

Dow Chemical Company

LG Chem Ltd.

Nippon Shokubai Co., Ltd.

Mitsubishi Chemical Holdings Corporation

Sasol Limited

Formosa Plastics Corporation

Wanhua Chemical Group Co., Ltd.

Shanghai Huayi Acrylic Acid Co., Ltd.

Zhejiang Satellite Petrochemical Co., Ltd.

Shandong Kaitai Petrochemical Co., Ltd.

Jiangsu Sanmu Group Co., Ltd.

Indian Oil Corporation Ltd.

Reliance Industries Limited

Saudi Acrylic Acid Company

American Acryl L.P.

Momentive Specialty Chemicals Inc.

Sumitomo Chemical Co., Ltd.

Technological advancements play a pivotal role in shaping the acrylic acid market, with companies investing in innovative processes to enhance production efficiency and sustainability. The adoption of bio-based acrylic acid production methods is gaining traction, driven by environmental concerns and regulatory pressures. Companies like BASF SE and Arkema S.A. are exploring the use of renewable feedstocks, such as glycerin, to produce bio-based acrylic acid, thereby reducing carbon emissions and dependency on fossil fuels. Additionally, advancements in catalyst technologies are enabling more efficient conversion of propylene to acrylic acid, minimizing by-product formation and energy consumption. The integration of Industry 4.0 technologies, including the Internet of Things (IoT) and Artificial Intelligence (AI), is revolutionizing production processes. For instance, Dow Chemical Company utilizes digital twin technology and predictive maintenance to optimize plant operations and reduce downtime. Furthermore, the development of advanced process control systems facilitates real-time monitoring and adjustment of production parameters, ensuring consistent product quality and operational efficiency. These technological innovations not only enhance the competitiveness of market players but also align with the global shift towards sustainable and environmentally friendly manufacturing practices.

In May 2023, Nippon Shokubai Co., Ltd. inaugurated a new acrylic acid facility in Cilegon, Indonesia, with a production capacity of 100,000 metric tons per year, aiming to meet the growing demand in Southeast Asia.

In March 2023, BASF SE commenced the construction of a new production complex at its Verbund site in Zhanjiang, China, which will include facilities for glacial acrylic acid, butyl acrylate, and 2-ethylhexyl acrylate.

In April 2023, Arkema S.A. launched the Incellion™ range of sustainable, waterborne acrylic solutions designed for high-capacity anodes, cathode primers, and ceramic-coated separators, reinforcing its commitment to innovation in the energy storage industry.

In May 2024, PT. Nippon Shokubai Indonesia received ISCC PLUS certification for its acrylic acid, acrylates, and superabsorbent polymers, and commenced production and sales of these certified products.

In November 2022, Arkema S.A. announced the certification of a range of bio-attributed acrylic monomers using the mass balance methodology, enabling the offering of certified bio-attributed specialty acrylic additives and resins for various applications.

The Acrylic Acid Market Report provides a comprehensive analysis of the global market dynamics, encompassing various segments such as derivatives, applications, end-use industries, and regional markets. It offers insights into market trends, growth drivers, challenges, and opportunities, enabling stakeholders to make informed decisions. The report covers key derivatives, including acrylic esters and polymers, and examines their applications across industries like paints and coatings, textiles, adhesives, and hygiene products. It also delves into the impact of technological advancements, such as the development of bio-based acrylic acid and the integration of Industry 4.0 technologies, on market growth. Furthermore, the report analyzes the competitive landscape, profiling major players and their strategic initiatives, including capacity expansions, mergers and acquisitions, and product innovations. Regional analysis highlights the market performance in North America, Europe, Asia-Pacific, and other regions, considering factors like industrial growth, regulatory frameworks, and consumer demand. The report serves as a valuable resource for manufacturers, investors, policymakers, and other stakeholders seeking to understand the current market scenario and future prospects of the acrylic acid industry.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 12,186.30 Million |

|

Market Revenue in 2032 |

USD 17,066.6 Million |

|

CAGR (2025 - 2032) |

4.3% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

BASF SE, Arkema S.A., Dow Chemical Company, LG Chem Ltd., Nippon Shokubai Co., Ltd., Mitsubishi Chemical Holdings Corporation, Sasol Limited, Formosa Plastics Corporation, Wanhua Chemical Group Co., Ltd., Shanghai Huayi Acrylic Acid Co., Ltd., Zhejiang Satellite Petrochemical Co., Ltd., Shandong Kaitai Petrochemical Co., Ltd., Jiangsu Sanmu Group Co., Ltd., Indian Oil Corporation Ltd., Reliance Industries Limited, Saudi Acrylic Acid Company, American Acryl L.P., Momentive Specialty Chemicals Inc., Sumitomo Chemical Co., Ltd. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |